8 tips for first home buyers using their KiwiSaver

8 tips for first home buyers using their KiwiSaver

28 Apr 2021

8 tips for first home buyers using their KiwiSaver

Everything you need to know about using your KiwiSaver for your first house deposit

You're planning on saving for your first home, and your KiwiSaver will make up part of your deposit - but how does it all work? It can seem like information overload when you first start looking into using your KiwiSaver as a house deposit. We're making it easy for you and covering everything you need to know, all here in one place.

What type of fund should I be in?

Before you start making plans to take out your KiwiSaver for your house deposit (more on how to do that soon), first let's talk about what KiwiSaver fund you should be in. Do you know what funds currently make up your KiwiSaver portfolio? If not, no worries, now is the perfect time to get informed and make some decisions that will put you in the best stead for that house deposit.

But first, what are KiwiSaver funds?

Your KiwiSaver is an investment, not a savings account - and you can choose what funds you invest in. A fund holds a mix of investments, and depending on what the investments are (e.g. shares, property, bonds) the fund will be more or less risky when it comes to volatility and movement in the markets. There are hundreds of different KiwiSaver funds, and what fund/s you choose will depend on your KiwiSaver scheme provider. Most providers offer Defensive (lowest risk), Conservative (low risk), Balanced (riskier), Growth (higher risk) and Aggressive (riskiest) funds. The riskier the fund, the higher the potential there is for you to have higher returns, but you're KiwiSaver balance will fluctuate up and down along the way.

So what fund is right for me?

Everyone has a different risk appetite (the level of risk they're comfortable with). How much risk you're willing to take on often depends on how much you're relying on your KiwiSaver for your deposit. Both of these things should be factored in when you're deciding what KiwiSaver fund/s to be in.

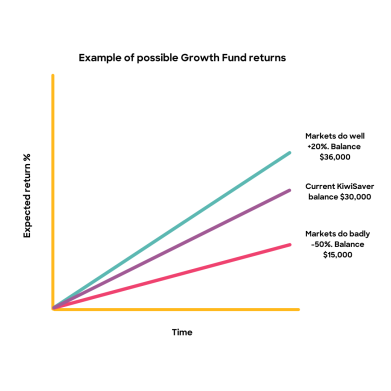

If you're planning on using your KiwiSaver within the next 1-2 years, then you need to ask yourself if you're willing to take the risk of losing a large portion of your KiwiSaver to potentially have higher returns and ultimately a bigger deposit. For example, you're current KiwiSaver balance is $30,000 and sitting in a growth fund. The market performs badly so your balance falls to $15,000. Alternatively, if the market performs well, your $30,000 could turn into $36,000. In this scenario, is the possibility of an extra $6,000 worth the risk of losing $15,000?

If losing 50% of your KiwiSaver in the short term means that you won't have the deposit you need for your house, then you might consider moving into a less risky conservative fund. In a conservative fund you may still see a dip in your KiwiSaver if the market underperforms, yet that $15,000 drop is more likely to be $2,000 instead, meaning that you're in a better financial position to buy your first property.

Depending on your KiwiSaver scheme provider, you can usually choose the percentage of your KiwiSaver account that is invested in a growth fund (higher risk) and how much of it is in a conservative fund (lower risk), meaning it doesn't have to be all or nothing when it comes to risk and returns. However, if you're unsure, then in general the closer you get to making the purchase, the safer it is move more and more of your KiwiSaver balance into a conservative or cash fund.

If you're planning on buying within the next few months, you won't want your KiwiSaver balance to dip at all. That means you should move 100% of your KiwiSaver balance into a cash fund so that it's waiting for you to withdraw it. While your KiwiSaver is in a cash fund, think of it almost like a savings account that will continue to have the money from your employee and employer contributions added to it. It will be ready and waiting for when the time comes to use it.

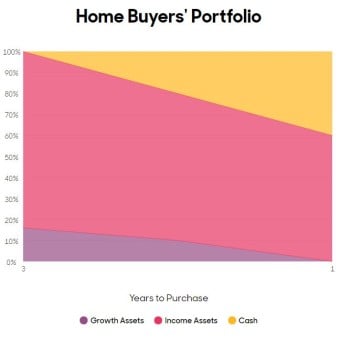

Example of a Kōura first home buyer's KiwiSaver portfolio

Do I qualify to use my KiwiSaver for my first home?

If you meet the below eligibility criteria then it's likely you'll be able to use your KiwiSaver to purchase your first home:

- You have to have been a member of KiwiSaver for at least three years or in a complying superannuation fund for three years

- You must intend to live in your property or on the land that you're buying. That means it can't go towards an investment property that you won't be residing in), and it must be in New Zealand

- You must be buying your first home or land, or qualify for a second chance home buyer withdrawal. If you have previously owned a home but your financial position is now similar to that of a first home buyer, then you may be eligible. Find out more whether you qualify for a second chance home buyer withdrawal over on the kāinga ora website

What happens if I’m buying with my partner and they already have a house, do I still qualify?

No worries, it just means that you'll be able to withdraw your KiwiSaver but your partner won't be able to withdraw theirs.

How do I withdraw my KiwiSaver, is it hard to get it out?

Good news, it's not hard at all! Your first home withdrawal is a really simple process, usually it entails contacting your KiwiSaver provider, filling out a form, and having your lawyer oversee the process. If you don't already have a lawyer, you'll want to find one for the process of buying your first home anyway, so this is just one extra thing they will help with.

At Kōura, once we have your filled out form, you'll have your KiwiSaver balance with you in 5-15 working days. Just be sure to factor in the 10-15 day period in when you're working through your Sale and Purchase Agreement.

How much can I take out?

If you're eligible to use your KiwiSaver to get on the property ladder, then your KiwiSaver withdrawal can be everything in your account except $1,000. So if you're current balance is $30,000, you'll be able to take out and use $29,000. With that said, you can choose to leave more than $1,000 in your KiwiSaver and take out less. Just remember that you can't change your mind and take more out later, the next time you'll be able to make a withdrawal is for retirement (or if you have extreme circumstances).

Am I eligible for a first home grant?

It's worth checking if you meet the eligibility criteria for a first home buyers grant. If you meet the criteria than you could have up to $10,000 extra to go towards your first home. Eligibility is based on whether you're buying as an individual or with others, how much you earn, how long you've been contributing to your KiwiSaver, and whether you're buy an existing home or a new build. Find out if you qualify for the KiwiSaver Homestart Grant here.

What should I be doing with my non-KiwiSaver savings?

If you have other money invested elsewhere that you're planning on using for your first home deposit (e.g. through platforms like Sharesies or Hatch), then the same risk rules as your KiwiSaver apply. You'll likely want to cash out of your investments so that you have the money ready, rather than leaving it invested and risk losing a large portion of it if the markets take a dive.

Should I wait to sort my KiwiSaver out until after I’ve bought my first home?

No way! The sooner you get your KiwiSaver fund selection right and suited to your current goals the better. Unless you're buying a house within the next month, then there's still time to change funds or even KiwiSaver providers. Sorting it out now means less surprises for you down the line, and while it can seem daunting at first, changing funds or providers is usually a quick and easy process. Plus, with all of the new responsibilities that come with owning your own home for the first time, why not sort it now instead of when you have your hands full.

What should I look for in a KiwiSaver provider?

- Low fees - the more you save on fees, the more money there is in your KiwiSaver. And because KiwiSaver fees will be one of the biggest expenses you’ll pay in your lifetime, it really pays to do your research when it comes to providers. kōura’s KiwiSaver fees are half the industry average at a very low 0.63%

- Personalised advice - personalised advice from your scheme provider means that you can rest easy knowing your KiwiSaver is working for you. However, personal advice often means higher fees. To avoid the high fees and still receive advice, find a provider with a personalised digital advice tool (like Kōura) who will ensure your KiwiSaver is performing and in-line with your goals

- Sustainable and ethical investing (ESG) - if ethical investing is a priority for you, then definitely opt for a provider who is transparent about the types of things they invest in. Kōura proudly has a best in class sustainable and ethical portfolio, so we only invest in things we can be proud of

About Kōura

At Kōura, we recognise how hard it is to save for the things you want (especially your first home). We make it easy for you to make the right decisions about your KiwiSaver. Build your own personlised KiwiSaver portfolio using the Kōura personal advice tool below.

[hubspot type=cta portal=5033855 id=dfd6e00f-28a3-40bc-a3d9-fe025bfa70f8]