April market update

April market update

5 May 2021

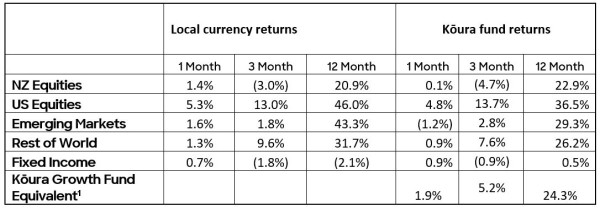

Global markets rose by over 4% this month, with the returns spread across all regions. The three big themes driving the markets were calming interest rate expectations, the concern around inflation, and the global economy starting to reopen now that more Covid-19 vaccines are rolled out.

Quick fire summary

April saw the strongest month since November with global markets rising by over 4% in the month. The returns were spread across all regions, though the USA appears to be going from strength to strength and delivered the strongest returns – the S&P500 generated a return of 5.3% in the month. The USA’s economic growth forecasts continue to be upgraded which, combined with ongoing stimulus and confidence on interest rates continues to push markets to new highs.

The three big themes that have driven markets this month are:

- Interest rates - after a record rise in long term interest rates in March, interest rates seem to have calmed down slightly in April as investors have better understood how the Federal Reserve will respond to inflation. A calming of interest rate expectations has seen a recovery in the tech stocks

- Inflation is the biggest concern for investors at the moment - If inflation rises, central banks will be required to push up interest rates. Higher interest rates will increase the return requirements on shares which is likely to push them down

- Global economic reopening – with vaccine programs accelerating through the developed world and fiscal stimulus remaining in place, economists and investors are preparing themselves for one of the strongest periods of economic growth in history

[1] Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4% Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%

Explaining the US market returns

The S&P500 return of 5.3% in the month was largely driven by the outperformance of the big tech stocks. The small cap (and main street orientated) Russell 2000 was up only 2% in the month versus the Nasdaq which was up 5.2%. Apple, Amazon and Google all delivered spectacular results in the last week of the month. Apple’s iPhone sales were up 50% on the prior period, which is truly incredible. The big question for these companies is how much of this growth is sustainable and how much of it is Covid inspired?

Over the past few months, inflation (the rate at which every day prices rise) came to the fore and seems to be swinging markets on a daily basis. If inflation does rise, then central banks may be required to raise interest rates which could cause share markets to fall.

The current elevated levels of inflation are driven by:

- The massive amounts of disposable income people have to spend at the moment - driven by stimulus cheques, the inability to go out and spend money while stuck in lockdown, and very low interest rates

- Very strong global growth - the expectation of record global growth for 2021 has driven the prices up for all commodities, from food to iron ore to copper. Commodities are now trading at their highest prices since 2013

- Difficulties in the logistics world – this is pushing up underlying costs and making it harder for companies to rely on global supply chains

- A rebound from a complete economic lockdown - which occurred in the second quarter of 2020.

Expect to hear lots more about inflation over the coming months

Biden’s tax and infrastructure packages

Another material piece of news in April were the Biden tax and infrastructure packages. At its core, Joe Biden wants to spend $3trillion to upgrade infrastructure, improve broadband and education access and accelerate the transition to a green economy. To fund this very significant change, Joe Biden has proposed plans to reverse some of the Trump tax proposals and increase the rate of capital gains tax to bring it into line with income taxes up to 39.6% for those earnings over $1 million. A 39.6% capital gains tax really puts into perspective how lucky we are in New Zealand to have no capital gains tax at all.

Markets did not really react to the tax proposals, however investors are trying to balance out the conflicting influences of higher spending versus higher taxes. They’ll also be looking to see what survives as the package works its way through the very difficult and contorted US legislative system.

Other overseas markets

Outside of the US the other standout global market was Taiwan, growing 7% in the month taking its 12 month return to 66%. One reason for the growth is that Taiwan hosts some of the largest semi-conductor companies who are seen as some of the biggest beneficiaries of the increased consumer spending. The remaining

Emerging Markets delivered a muted return of 1.2%. Strong economic growth across all countries and upgrades of GDP forecasts were offset by a strengthening US dollar and a Chinese crackdown on some of the Fintech companies in China and Hong Kong.

Europe is still struggling to move into a consistent recovery through the lockdowns, and Eurozone GDP shrunk in the quarter which was against expectations. This was driven by new lockdowns that were introduced in Germany, France and Spain. Despite this, the Eurostoxx index (a selection of European large cap stocks) still returned a respectable 2.3%.

For the first time in a long time the UK based FTSE 100 outperformed the rest of Europe. The UK has done a great job on vaccinations with over 50% of the population having received a first jab, and almost 25% having received their two required shots. The UK is expecting to have most restrictions lifted by mid-June and will even open the country to vaccinated travelers – making this timeline significantly ahead of most European markets. Still, the UK has been hit harder by a combination of Covid and Brexit, with GDP falling close to 10%, significantly further than other European markets. As a result, the FTSE 100 is still at breakeven level over the past 2 years versus a 20% positive return on European and US stocks over the same period.

NZ markets

Here in New Zealand, it was a relatively quiet month with the NZX 50 gaining 1%. Surprisingly, news of the travel bubble did nothing to travel stocks such as Sky City, Air NZ, Auckland Airport and Serko, suggesting that this news had clearly already been priced in. Retail and consumer focused stocks such as Kathmandu, NZ King Salmon and Comvita all performed well as the strong economic growth is likely to continue to drive strong profit growth for these companies.

Unfortunately, the two large dairy companies A2 Milk and Synlait continue to decline. A2 milk hit a new low of $7.65 in the month, a far cry from the previous high of $21.74 reached in September 2020. Investors continue to worry about whether A2 will be able to deliver on its expectation of winning in the Chinese infant formula market, which is highly competitive and increasingly regulated market.