August market update

August market update

7 Sep 2021

An exceptional month for NZ with the global markets continuing their record-breaking winning streak

August market update

Once again, we’re in lockdown. The fears of the covid delta variant reaching our shores have now become reality. Generally, you would expect a link between lockdown restrictions and your KiwiSaver but we have seen no links at all – despite the lockdown and increasing global concern on the Delta variant, markets, and therefore your KiwiSaver balances continue to march higher.

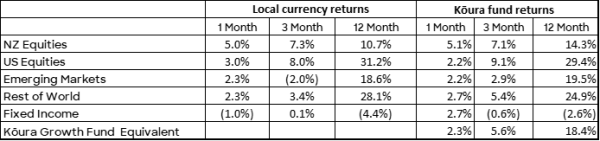

NZ markets have been one of the strongest global performers over the month, bucking our recent trend of poor performance. The key drivers this month have been very strong results from several large companies and the prospect of takeover activity of a few companies.

Internationally, markets continued their unabated march higher with companies around the world reporting strong earnings, increased certainty on reopening, and reducing uncertainty around potential interest rate hikes. Key markets have now delivered 7 consecutive months of positive returns.

Key news events during the month were:

- Against all expectations, the RBNZ (Reserve Bank of New Zealand) held the OCR (official cash rate) steady due to the potential impact of announcing rates on the same day as Level 4 lockdown

- The US Fed chair Jerome Powell’s annual Jackson Hole speech provided more comfort to investors on the pace of interest rate normalisation

- A number of European markets outlined their plans for reopening and getting back to a normal post-covid world allowing investors to fully price in the recovery

- The Chinese Premier Xi Jing Ping set out his agenda for more inclusive prosperity, giving confidence that regulatory intervention which has plagued the market this year might be close to an end

Kōura fund updates

[1] Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4% Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%

Why has NZ's new lockdown not hit your KiwiSaver?

Before we dive into the full market update, we thought it would be useful to answer the most common question we are getting at the moment.

Back in March 2020 as we went into lockdown our KiwiSaver balances were tumbling and for some, it felt as though the world was ending. This time is very different, and KiwiSaver balances continue to grow for a few reasons:

- Investors and markets believe they now understand Coronavirus and its potential impacts. With vaccine rollouts largely underway and a number of countries' rollouts reaching an end, people can now see a clear path back to normality. Most investors are hoping that by mid-2022, Covid restrictions will be long gone, and we will have learned to live with the virus

- Your KiwiSaver should be well-diversified and should therefore only have limited exposure to the New Zealand market (most KiwiSaver funds would be below 25% exposed to New Zealand). Internationally, the delta variant has been around for a while, and whilst it has had an impact on economic growth it is not expected to be a significant long-term impact that will drive company earnings or valuations

- The New Zealand market believes this current lockdown will be a short-term blip and does not believe that this lockdown will have a material impact on the state or strength of the economy. Instead, strong company results and outlooks have driven the market, rather than Covid related fears.

It really comes down to the fact investors now understand Covid and can see a clear path out and back to normality.

New Zealand

Despite covid restrictions impacting NZ for the second half of August, the NZX delivered a market-leading return of 5% for the month of August.

The RBNZ (Reserve Bank of NZ) was widely expected to raise interest rates to address the clear inflation pressures in the economy, however, the day they were expected to announce the interest rate rises the country was plunged into Level 4 lockdown. In a later interview with Bloomberg, a Deputy Governor explained that they did not want to announce interest rate hikes on the same day as Covid lockdowns due to “communication difficulties”.

We struggle to understand why Covid would have created communication difficulties, but we are not economists. At least this very frank admission saw the foreign exchange and fixed income markets quickly reprice the possibility of sharp interest rate rises leading into Christmas. There’s a link to the article here if you’re interested.

Another key driver of returns in the month was the announcement of very strong results from a number of large companies. Company results are coming in ahead of expectation, reflecting the strength of the domestic economy.

Compounding this, we saw a takeover offer launched for Z Energy (not a Kōura holding because of its fossil fuel exposure) and the potential of a takeover of A2 Milk from Nestle. Unfortunately, the Nestle rumours were not enough to protect A2 from further bad news as it released a deteriorating outlook related to difficulties in China. It has now fallen 73% from its July highs. A great lesson on why diversification is so important.

US

The S&P 500 recorded its seventh month of gains ending the month 3% higher. Investors continue to swing between the key themes of:

- Wondering when will the fed start to taper its bond purchases (which will result in interest rates rising);

- Questioning whether the US economy has reached peak growth – was the last quarter as good as it will ever get?; and

- Whether the delta variant will push back reopening and create another 12 months of disturbances

Jerome Powell (US Fed Chair) helped the markets answer the first question during his annual Jackson Hole summit signalling that federal rate hikes (same as our Official Cash Rate) are still a long way away and tapering was to be treated separately to interest rate hikes.

Understanding where interest rates are going is the main driver and with clarity on the interest rate settings, markets seemed to forget about concerns from a slowing economy.

Economic concerns were reinforced at the end of the month when labour surveys showed that significantly fewer jobs were created over the past month than forecast. Though markets ignored this important point and chose to see this as another indicator that interest rates may stay low for longer.

Europe & Japan

European vaccination rates on the rise

Both the FTSE100 and Pan European Stoxx 600 index were up over 2% month on month in August, marking the seventh consecutive month of gains. This is despite August typically being a quiet month for trading due to the summer holidays. However, there were signs of slowing at month-end.

All over Europe inflation reports are showing the highest consumer prices in a number of years. Preliminary Eurozone inflation is expected to have reached 3% in August which is well above market expectations. This is driven by a steady recovery in domestic demand and a low base (comparison) year caused by the Covid pandemic.

UK business confidence is at a four-year high, but difficulty in recruiting new staff is still an issue, demonstrating that the economy is operating close to capacity.

Vaccination rates are on the rise and 70% of adults have been fully vaccinated. This has allowed countries such as the UK, Denmark, and Portugal (some of the worst-hit during the pandemic) to set clear reopening schedules and timelines. We expect most of Europe to drop Covid restrictions in the next few weeks.

Japan ends the month strong

Shares in Japan rallied after catching the tailwind of strong Wall Street performance and the conclusion of a highly successful Olympics. This was all despite the fifth wave of record Covid numbers and Tokyo and Osaka being in a state of emergency.

The Bank of Japan announced it will support the fight against climate change by providing zero-interest loans to commercial financial institutions that plan to invest and take out loans in the area.

GDP returned to modest growth in Q2 2021, rising +0.3% quarter-on-quarter (1.3% on an annualized basis). While performance was up, it was still hampered by ongoing restrictions due to Covid.

The supply chain crisis caused by Covid continues to impact Japan’s manufacturing base, with Toyota announcing it would cut the output of its cars in September by 40% compared to previous production plans. The stock closed 2.17% down in August.

Emerging Markets

Emerging markets were up 2.3%, with the Chinese markets making a recovery following its July regulatory announcements, despite the tightening of restrictions as delta cases spike. Vaccination rates continue at a pace that is slower than preferred, with China having vaccinated 55% of the population over August.

Chinese President Xi Jinping continued his campaign of “common prosperity” in a bid to return the country to Communist Party values. After already targeting the data-rich tech sector, the focus is now on reigning in the excess of civil society, including fandom, academic cram schools, and video gaming. After the excessive growth of some Chinese companies that are now bigger than State-owned enterprises, the state seems to want to further close the wealth gap by shaping citizens' daily life. This month has seen limits on gaming for minors, warnings about business drinking, increasing tax evasion investigations, and efforts to erase “celebrity” influences. The question for investors is how far will this go? And how long will it go on for? Will the government privatize public companies to redistribute wealth?

China billionaires are taking it seriously. Tencent Holdings (up 0.43%) and Alibaba (down 12.43%) both pledged funds for social responsibility programs, and Pinduoduo (up 9.18%) has set aside future profits for agricultural programs.