August market wrap: Japanese Carry Trade Unwinds, NZ Rate Cuts, and Global Market Volatility

Table of Contents

August market wrap: Japanese Carry Trade Unwinds, NZ Rate Cuts, and Global Market Volatility

11 Sep 2024

After a shaky start, global share markets managed to shake off their nerves and returned to trend, delivering a positive return for August, an amazing feat given they were down 8% after the first week! Investors are clearly on edge with increasing unease about the lofty valuations and the increasingly uncertain economic environment. With markets up almost 20% since the start of the year and valuations at all time highs it is easy to see why investors are on edge.

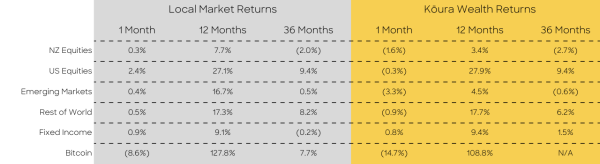

Source: Factset: Kōura returns are pre-tax and post-fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ. Local market returns use the relevant markets indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin.

The unwind of the Japanese carry trade

At times, finance professionals can move like a herd, they follow trends that appear to be too good to be true and more often than not forget about the risk management implications on the way through. This time it was the Japanese carry trade. According to Deutsche Bank, the herd managed to put US$20 trillion into this trade, a huge bet!

Japan has been battling deflation for the better part of the last 30 years and as a result has had ultra low interest rates. Even over the past few years of high global inflation, inflation remained low and it was not clear whether it would breach the 3% target of the Bank of Japan, or that the Bank of Japan would be willing to raise interest rates even if it breached the 3% target. Investors effectively interpreted this as Japan would have 0% interest rates permanently. This is why the Japanese Yen has continued to fall in value over the past 2 years.

To take advantage of this, Investors saw this as an opportunity to take out low interest loans in Japan and invest the funds in higher returning off shore markets such as USA or even Mexico. A great strategy so long as interest rates remained low in Japan and the Japanese Yen continued to weaken.

This all changed in July when it became clear the US Fed would lower interest rates and the Bank of Japan announced it would look at raising interest rates to deal with inflation (that has recently crept above the 3% target). Foreign Exchange markets reacted exactly as they should have and we saw a rapid 15% strengthening of the Japanese Yen against the USD - bad news for anyone that had borrowed in Yen and used that to invest in offshore assets (effectively the loans are now worth more than the underlying assets that have been purchased). Investors needed to quickly sell assets to unwind their positions as the losses meant that they had breached risk or leverage ratios.

Markets (particularly the S&P500) reacted strongly to this and were down c.7% over the first few days of the month with investors fretting that this was the start of the end of the massive bull cycle. This reaction was extreme and appears more likely related to the summer holidays and light trading volumes rather than anything material. A week after this correction, markets had fully recovered to where they had started.

This mini crisis demonstrated how nervous markets are at the moment. Many investors jumped on any reason to be negative and shows the importance of not reacting to short term news cycles, particularly in the current environment.

Interest rate cuts here in New Zealand – good or bad news.

In New Zealand we finally received relief from Adrian Orr and the Reserve bank of New Zealand with the Official Cash Rate being cut by 0.25%.

This was a marked change from May when the RBNZ said that they had considered raising interest rates as they were still concerned with inflation. Many economists have lambasted the RBNZ calling it a backflip though, the alternative perspective is that the NZ economy has slowed significantly faster than anyone had ever anticipated.

Anecdotally, many businesses are struggling which makes sense considering the external factors that are going on; fixed rates have rolled over with the most mortgage holders paying the higher interest rates, most Government projects have been stopped awaiting outcomes of various reviews, the housing market is at 2008 Global Financial Crisis levels levels, and immigration has materially slowed. All the things that have driven our economy for the past 10 – 15 years are no longer existent, so we should not be surprised that things have stopped.

Banks have started reducing their mortgage rates, though have a lot further to come if they are to come close to matching the sharp downward movements in wholesale interest rates. Wholesale interest rates have now fallen by over 1.5% since their peaks which shows how far we have to go on retail mortgage rates.

Whilst good news for mortgage holders, it is very scary for many New Zealanders who are now fearful of their jobs and still facing higher cost of living.

The US economy is on a bit of a knife edge

Toward the end of the month, US Federal Reserve Governor Jerome Powell confirmed that we are likely to see a fall in the US interest rates in September.

Over the past few months, we have seen worsening job openings data, manufacturing data and the unemployment rate continues to tick up. Investors are unsure of whether this is good news or bad news. On one hand the softening economic data increases the chances of interest rates coming down faster, though on the other it might indicate the much talked about soft landing is not quite as easy as expected and maybe the higher interest rates have tipped the US market into recession.

Potentially we are only now seeing the long and variable impacts that higher interest rates can have on the economy.

Nvidia has come off its highs

Nvidia, the success story of 2024 has fallen 15.2% from its all time highs, though still remains 102% year to date and a meteoric 691% return over the past 2 years. Investors are increasingly concerned that Nvidia will not be able to maintain its meteoric growth. Its recent boom has propelled it to the third largest listed company in the US and was briefly one of only 3 companies to have been valued at over US$3 trillion.

Nvidia appears to be yet another example of retail exuberance (remember Tesla?) and shows why you need to manage your risk as an investor.

Bitcoin remains flat, despite having the potential for significant growth

Bitcoin ended August down at US $59,000 despite continued positivity in the sector. Crypto enthusiasts are scratching their heads wondering why Bitcoin is not going stronger:

- the ETF’s have proven to be a big success in the US and have now been followed by the successful launch of Ether ETF’s

- Donald Trump and Kamala Harris have both indicated policies that will support the crypto industry into the medium term

Unfortunately, Bitcoin can’t quite get out of its current trend of US $55 – 65k which is largely due to the economic uncertainty. Despite fighting the allegation, crypto remains a barometer for risk (when investors are brave crypto soars, and when investors / economists are nervous crypto does not fare well) and with the high levels of uncertainty at the moment, it is hard to see it breaking out of its current range.