A core-satellite investment strategy; what is it and should you follow it?

A core-satellite investment strategy; what is it and should you follow it?

17 Dec 2021

core-satellite investment strategy; what is it and should you follow it?

So you understand the fundamentals around investing, like your investment horizon and risk appetite, maybe you’ve also dabbled in investing a fair bit too. But now you want to start taking your investments more seriously and are looking for your next move. If you’re wondering what different investing strategies are out there and what one is best for you – then this is the article for you!

The average everyday investor has somewhat of a buffet selection when it comes to investing platforms these days, but what good are they if you don’t have a good investment strategy in mind?

An investment strategy is more likely to enable you to achieve consistent returns in the long run and do it all while staying within the risk levels you’re comfortable with. Our article takes a look at the ‘core-satellite investment strategy’, what it’s made up of and how you might build your portfolio around it!

What is a core – satellite investing strategy?

At a glance, a core-satellite investment strategy is the method of building a portfolio that focuses on having a ‘core’ group of investments that are well diversified, long term, low cost and don’t ever need to change with a smaller group of holdings that are more actively managed called ‘satellites’. Ideally you would only look at your core every year, or potentially even less.

This approach allows you to take measured risk whilst minimizing costs, volatility (risk) and tax liability. It also allows you the opportunity to test out different investment strategies and participate in the latest crazes - and maybe even outperform the wider stock market as a whole.

What makes the core - satellite strategy so good?

Well for one, it allows you to take a much more measured level of risk with your investments – allowing for better diversification by not having all your eggs in one basket. It also gives you the opportunity to be more involved and engaged with your investments – with the whole ‘set and forget’ strategy being boring and often leaving you to wonder whether you could do better.

It also helps to reduce FOMO (fear of missing out) investing as you can afford to take small bites, and if something doesn’t work out, you’ve only allocated a small portion of your portfolio toward it. It also means you can try out different investment strategies and approaches without taking too much risk overall.

So then what exactly are core and satellite holdings?

The core is the central part of your portfolio, which if set up properly can be the backbone of your portfolio which you can expect to leave long-term and not really touch. In our opinion this should be a series of passive funds, though it could also be a series of actively managed funds as well. When setting up your core, make sure you can tick off some of the core fundamentals:

- Is it well diversified (across different companies, countries, regions, and sectors). A single (or potentially multiple) fund can give you diversification, but if you want to build your own portfolio make sure you have at least 15 – 20 holdings across the factors mentioned above. Just remember, the more concentrated your portfolio holdings are, the more you need to watch it.

- Is it low cost – remember expensive trading, holding and funds management costs will eat into your returns

Satellites on the other hand are some of the more active short / medium term investments that you want to add to your portfolio where you might be willing to take on a bit more risk. For example, if you were to invest in a single stock (e.g. Tesla), commodity (e.g., Gold) or Crypto (e.g., Dogecoin) because you think it has interesting characteristics - these would all be components of a satellite structure.

A good general rule of thumb is that your core holdings should make up around 80-90% of a portfolio, with satellites making up the remainder.

Most active fund managers employ a core - satellite strategy. They basically invest in the market and then make specific decisions around the edges, for example they might decide to own a bit more of a certain company than the market does or avoid a company because of concerns.

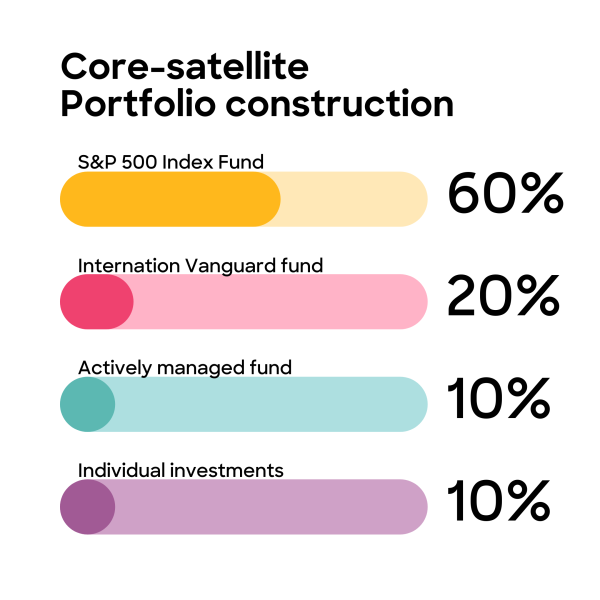

We've put together a little example of what that could look like below. In our example, you could put 80% toward passive investments and 20% toward a mix of actively managed funds and individual picks of companies that you would personally like to invest in. The asset allocation is shown below:

Fig 1. Disclaimer: Kōura has not researched the non-Kōura funds mentioned above. This is just an example of how someone could choose to create their portfolio.

So, you have built your core holdings and satellites, now what?

Once you’ve sorted out how much you’re allocating to what, the key is to keep on top of things, making sure you do regular check-ups where you can rebalance your portfolio if you feel you are too heavily weighted in one area.

Also be sure to keep an eye on your fees. Even though most of your portfolio might be made up of passive investments, its still a good idea to watch how much you are paying for your active portion. Every dollar you pay in fees means a dollar less for you.

Now we’ve said it before, and we’ll say it again. Once you have set your investment strategy, make sure you stick to it! One of the worst mistakes you can make as an investor is attempting to change strategy and try to time the market, or even worse getting scared in a market downturn and converting your investments to cash!

Finally, if something sounds too good to be true, it probably is. What we mean by this is – it’s really important to do your own research, don’t get caught up in the hype of ‘the next big thing’ and instead only invest in things you’ve properly read through and understand.

The final takeaway

Hopefully, this has given you a better idea of how you might approach your investment portfolio strategy, there’s a lot to take in, so it's okay to feel a bit overwhelmed – but by setting yourself up with the right strategy now, you’ll be in a much better position in the long run.

Please note none of this should be deemed as financial advice and we strongly suggest you do your own research.