The KiwiSaver default fund changes, and what they might mean for you

The KiwiSaver default fund changes, and what they might mean for you

15 Nov 2021

The KiwiSaver default fund changes, and what they might mean for you

you might've heard there's going to be a change in default KiwiSaver providers soon. If you're wondering what this means and whether you're impacted, here's what you need to know!

What exactly are Default funds?

When you join KiwiSaver, if you don’t make an active decision on your preferred KiwiSaver provider, then you're randomly allocated to a KiwiSaver default fund with one of the KiwiSaver default providers.

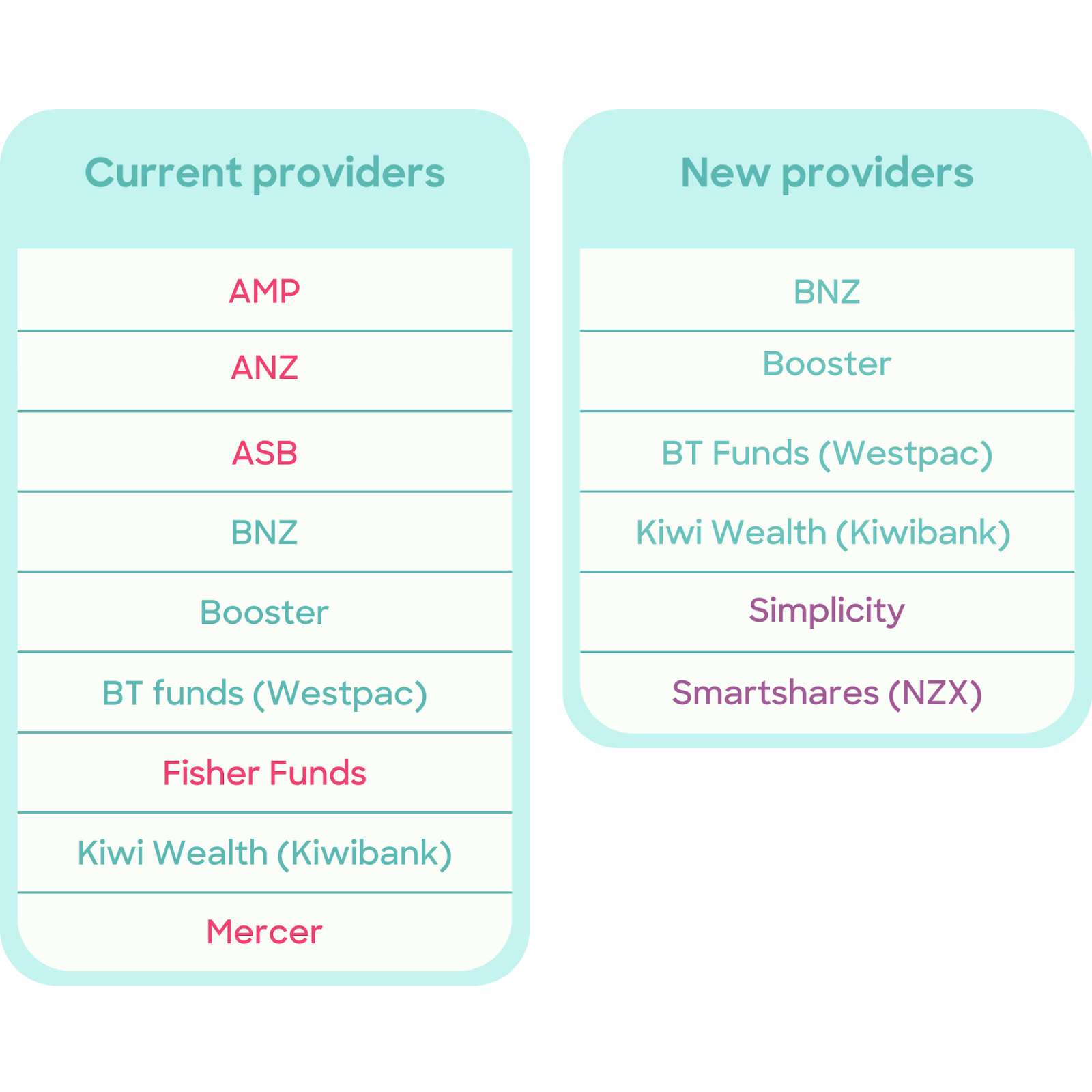

Every 7 years, the Government selects a new panel of default KiwiSaver providers (and evaluates whether the current default KiwiSaver providers should stay or be swapped out). A new set of default KiwiSaver providers were appointed earlier this year, and the changes are set to take effect from 1 December 2021 (see the below table for who's staying, who's getting the boot and who's joining!)

So who’s the new default fund providers?

What happens if I'm in a default fund?

If a KiwiSaver provider has had their default status removed (Like ANZ, AMP, ASB and Mercer) then their members that are currently sitting in a 'default fund' will be reallocated to a new default provider on the 1st of December.

If you're with a provider that is losing their default status but AREN'T in a default fund (for example, you're in an ASB 'conservative' or 'balanced' fund) then you won't be impacted by these changes and your KiwiSaver provider and fund will stay the same.

So what should you do if you're in a default fund with a default provider that's getting the boot?

This is a great chance to take active ownership of everything and figure out if your KiwiSaver provider and fund your in is the right one for you (and if it isn’t - make the switch!). Doing this won’t only benefit you long term, but it will also stop you from being randomly moved to another KiwiSaver default provider/fund. Some other things you can check up on or change whilst doing this:

- Check what your contribution rate is, the default setting is 3% - this isn’t anywhere near enough to have a comfortable retirement, so if you can afford to increase this, do so!

- Take the time to think about whether you are still comfortable with your risk appetite and investment timeline (check out our blog that covers these things if you’re unsure)

If you're not sure where to start - check out our digital advice tool that builds you a recommended KiwiSaver portfolio.