How to build an investment portfolio - using kōura’s digital advice tool

How to build an investment portfolio - using kōura’s digital advice tool

4 Sep 2021

How to build an investment portfolio

If you’re starting to think more about your financial future, have your KiwiSaver sorted, and now want to build the rest of your investment portfolio, then this is for you.

The everyday investor is pretty spoilt for choice when it comes to investing platforms, but rather than just diving in and buying some Tesla and Apple stocks, how do you build an investment portfolio that is more likely to deliver you more consistent returns in the long-term? Let’s break it down.

We’re going to talk you through how to build a portfolio that follows a passive investment strategy, is tailored to suit the timeline you’d like your money invested in, and the level of risk you’re willing to take.

You can jump ahead and use kōura’s digital advice tool to create an example investment portfolio for you - but we highly recommend sticking around to read how to turn your example investment portfolio into the real thing, and understand the thinking of how it’s all created.

1. Understanding your investment horizon and risk appetite

Your investment horizon is how long you plan to have your money invested without needing to withdraw it. It’s a key factor in determining what types of things to invest your money in.

Your risk appetite is how comfortable you are with the ups and downs of the market. It’s also a key factor in determining what types of investments you should have, and what percentage each investment makes up in your overall investment portfolio.

Two general investing rules:

- The longer your investment horizon, the more risk you can take in your investments because you have longer to ride out short-term market volatility (ups and downs). Therefore, the shorter your investment horizon, the less risky your investments should be (in simplistic terms, less shares and more bonds, term deposits and cash).

- Once you set an investment strategy you should stick with it through market ups and downs. So if you feel uncomfortable or worried seeing your investments drop in value in a market dip or downturn (and therefore what to take out your investments to protect them from further loss), then your risk appetite is low, and you should choose lower-risk investments. If you’re comfortable with swings in the market and fluctuations in your investment portfolio value then you have a high-risk tolerance.

Answering these two questions will allow you to create an investment portfolio that suits you and what you want to achieve.

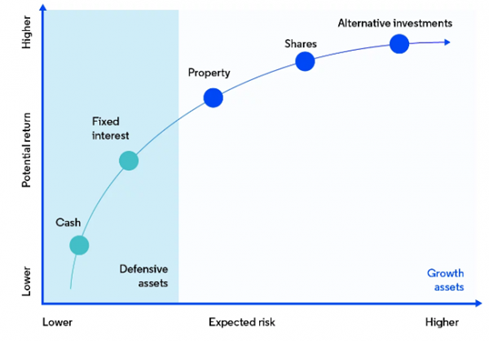

The different investment types:

Each type of investment sits somewhere on a scale of high to low risk, with higher risk investments generally having the potential to bring higher returns.

Cash

This is the most readily and easily accessible asset you have (AKA it’s a liquid asset). Cash is what you think it is - the money you’ve got sitting in a band account or term deposit. It has the lowest risk, but also usually the lowest return.

Fixed income

Fixed income is a fancy name for things like government and/or corporate bonds, and money market funds. It’s a lower-risk investment option that will likely generate a small return (so that you’re not losing out to inflation if you were to keep your money in cash).

Equities & shares

Equities (AKA shares) are when you invest money in a company (or selection of companies) by purchasing shares in the stock market. This is a higher-risk form of investment but generally brings higher returns.

Investment horizon timelines:

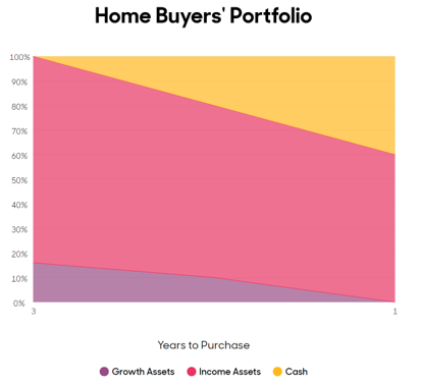

0-2 years - your portfolio should be mostly cash and fixed income assets

As you get closer to drawing on your funds you should start to hold more of your investments in more easily accessible, lower-risk assets like cash. This is to protect your balance leading up to when you need to use it. See the graph below for how Kōura starts to de-risk an investment portfolio when the investment timeline nears the end (e.g. you’re about to withdraw and buy your first home).

2-5 years - your portfolio should be an even balance of growth and fixed income assets

You have a bit of time in the market, but not long enough to take on TOO much risk. If you’re investing for 2-5 years then it's usually best to allocate 50% of your funds into high growth assets (so you can still benefit from market returns), but keep 50% in lower-risk fixed-income assets in order to help protect your final balance against market downturns as you get closer to withdrawal in the coming years.

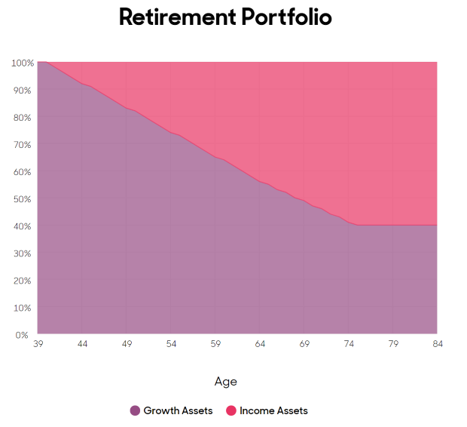

5-10 years - your portfolio could be largely growth assets offset by some fixed-income assets.

You’re still a while away from withdrawing any funds so you have the time to take on more risk. If you’re comfortable taking risk, this could mean you have a portfolio that’s around 70% growth, 30% fixed income. However keep in mind that as your timeline shortens, your portfolio should slowly be made up of more lower-risk assets.

10+ years - your portfolio could be mainly high-growth with a very small amount of fixed-income.

If your risk appetite is high then you can afford to create a portfolio that is high growth (e.g. 90% growth assets, 10% fixed income). That way you’re likely to generate more returns from your investments. With such a long timeline you can usually afford to carry more risk due to there being more time for your portfolio to recover if there is a market downturn.

See the glide path below as an example of how Kōura starts to de-risk a long-term investment portfolio as the investment timeline nears its end (e.g. moving towards retirement and thereon after).

Putting it into context - investment horizon examples:

Say you needed your savings in 6 months to put toward your home deposit, your investment horizon is very short. It would be better advised to hold mostly low-risk investments (like cash and fixed income) rather than holding a lot of higher-risk investments like shares (whose value could drop more significantly in a short period of time).

However, if you're wanting to put your money away for 25 years, choosing higher-risk investments like shares is less risky as you have a longer period of time to ride out the market ups and downs, and will likely end up with a bigger balance at the end of your investment horizon. They are much more likely to outperform inflation and provide a better long-term outcome.

2. Putting it all together to create a diversified portfolio

If you start by investing in a few of your favourite companies (like Tesla or Apple) it's unlikely you'll have a very diversified portfolio. Investing in lots of different companies, across lots of different markets and sectors means if a few do badly, they'll be offset by the others that do well.

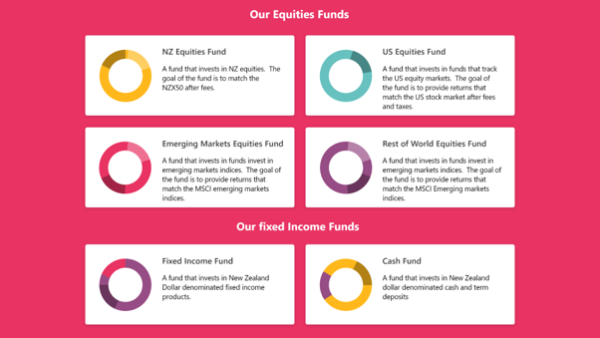

A general rule of thumb is to have at least 10 different investments, ideally across 2 or 3 global markets (Like the US S&P 500 or the MSCI emerging markets). One of the best and easiest ways to achieve this is by using a managed fund - this is because a single fund can have hundreds of investments from around the world!

As an example, here are the different funds that could make up a Kōura portfolio:

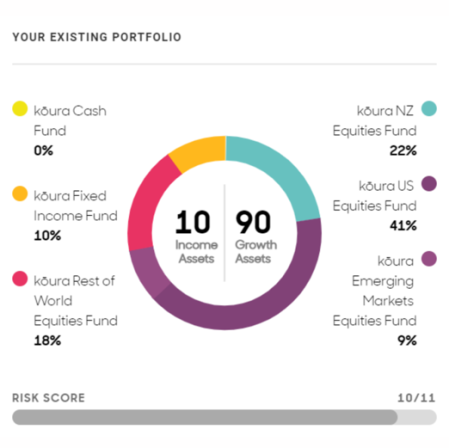

And here is an example of how those funds can make up a diversified investment portfolio:

A diversified portfolio is about not having all of your eggs in one basket (or market)

3. Where to go to create your investment portfolio

So you’re all schooled up and have an idea of the investment portfolio you’re going to create - but where do you go to actually create one?

Firstly choose whether you’re going to invest in individual companies or managed funds:

There are a couple of ways of going about it, the first is by investing directly in shares or bonds (i.e. individual companies like Fonterra or LuluLemon) - there's a range of new platforms around that make it easy to purchase bonds or shares directly. And remember if you’re going to invest directly in bonds or shares make sure you spread your eggs into a number of investments and only invest in the things that you understand (do your own research).

The other method (the one that Kōura uses) is investing through managed funds (e.g. a fund that tracks the S&P 500 which is a fund that holds a mix of the 500 largest companies in the U.S) - they are a vehicle where everyone’s money is pooled together and managed collectively. We’re big fans of managed funds as they’re a great way for everyday investors to achieve diversification (spreading investments across a variety of companies), keep costs low, and have someone else employed to monitor the investments full time.

Then choose the platform/s you’re going to use:

These days there are plenty of popular options for where you can easily access different types of investment. If you’re just starting out and want to get a better idea of how things can work. Here are some options of places you can use to invest in:

- For U.S or global equities, you could choose to invest in a fund like the International Vanguard ACMI through platforms such as InvestNow, Hatch, and Sharesies.

- For NZ equities there are funds like the SuperLife NZ SO through Superlife.

- For Fixed interest, you could invest in funds like SuperLife fixed interest which is available through the SuperLife website.

Just remember, wherever you start your investing journey, it’s important to still do your own research and understand what it is you’re investing in.

Disclaimer: Kōura has not researched the non-Kōura funds mentioned above. This is just an example of how someone could choose to replicate a Kōura portfolio outside of Kōura KiwiSaver.

A few other things to watch out for when investing

Now you know the basics of setting up a diversified investment portfolio, here are a couple more things to keep in mind:

- Once you have set your investment strategy, stick to it

One of the biggest mistakes you can make as an investor is continually changing strategy and trying to time the market, or even worse getting scared in a market downturn and converting your investments to cash.

Investing can be nerve-racking, so make sure you choose an investment strategy and stick with it through both the market upturns and downturns. Time in the market always beats trying to time the market. - Keep your fees low

Make sure you understand all of the fees in your investment strategy and think about how they impact your investments. Every dollar you pay in fees means a dollar less for you.

Paying a $3 trading fee might not seem like much, but if you are making a $50 trade every month, that means you will be paying around 6% in fees. That's a huge amount of investment you'll have to make up in performance for them to be worth it.

Low fees are also why we like passive investment funds, they're generally the most cost-effective way of investing. - If it sounds too good to be true, it generally is

Doing your own research is really important, but there's no shortage of information around 'the next big thing' to invest in - and FOMO (fear of missing out) investing is on the rise.

Instead of getting caught up in the hype, stick to your investing strategy and avoid investing in anything you don't understand. Investing is something to be thought through and if you don't understand it, or if it sounds too good to be true, it's a good idea to stay away.

Hopefully, this gives a better idea of how you can build an investment portfolio outside of your KiwiSaver, but if you’re still unsure - try using kōura’s digital advice tools to help you see how things could look.