Choosing the KiwiSaver fund that’s right for you

Choosing the KiwiSaver fund that’s right for you

30 Oct 2020

How do you choose a KiwiSaver fund that's right for you? Check out our basic guide.

Almost thirteen years into KiwiSaver, there are 30 different KiwiSaver providers and over 150 funds to choose from. Comparing funds is a bit like comparing apples and oranges – with a few nuts mixed in there too. Trying to assess different underlying asset mixes, fees or historical returns is really hard. No wonder Kiwis put investing in the ‘too confusing’ basket and leave their KiwiSaver account where it is.

68% of Kiwis consider KiwiSaver to be a very important tool for their retirement. Yet, we don't realise the importance of getting it right. A recent survey done by Kōura uncovered that less than half of people are sitting in the type of fund that's right for their risk appetite and objectives. Not making a decision (or making the right one) could cost you hundreds of thousands of dollars.

That’s why we’ve put together this guide to help you choose the right fund for you.

Meet Ben

Ben is a mince & cheese pie loving marketing executive that's just returned from his OE and is stoked to get a job that's paying him $80,000. He ticked a box on the first day of his new job agreeing to contribute 3% of his salary to KiwiSaver account with another 3% being matched by his employer. With marriage and renovations to his do-her-upper on the horizon, he's relying on his KiwiSaver plan for retirement.

If Ben invests in a selection of funds appropriate for his objectives and achieves the expected returns, he can expect to have a KiwiSaver balance of $590k when he retires, giving him an allowance of $625 a week including his NZ Super payments. Though for this to happen, there are a number of different decisions he needs to get right!

Let's look at each of the things he should be considering (and why they are more important than watching another re-run of Friends on the telly).

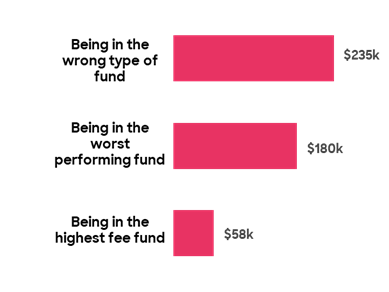

Impact of different decisions on Ben's KiwiSaver balance at age 65

Choosing the right type of KiwiSaver fund

Getting this decision wrong could cost Ben $235k by the time he retires (that's a 40% difference!)

Each KiwiSaver fund has a very different makeup of assets. Growth funds have much higher money allocations to growth assets like shares, real estate and infrastructure while conservative funds have much higher allocations to fixed income products like bonds and bank deposits. Growth assets will typically be more volatile (have more ups and downs), but they’ll usually deliver higher returns over the long term.

Mention 'volatility' in the same sentence as 'your KiwiSaver' and most people get scared and tend to just go with whatever seems to be the safest option. While the type of fund you invest in should definitely take your risk appetite into consideration, you also need to assess your decision in terms of your objectives and investment horizon.

If you're like Ben saving for your retirement, then you need a higher proportion of growth assets because even if there's a market downturn, you will have plenty of years for your investments to recover. However, if you're planning to purchase your first home in the next few years or approaching retirement then you need a higher proportion of fixed income and cash assets. These assets will deliver a lower return but will have less volatility, giving you the protection of your portfolio not falling as much in value even if there's a market downturn.

To understand more about risk and return, and how you should think about it for your KiwiSaver portfolio, check out our post What does risk mean in the context of your KiwiSaver.

Most providers offer a generic Growth, Balanced and Conservative fund structure to cater to people’s needs. But you need to be careful because a growth fund could mean different things to different providers. Check the asset allocations of your chosen fund to make sure that it is giving you an appropriate asset allocation mix for you. For more on this, check out our post, Is a growth fund really a growth fund?

Key points:

- If you’re investing for the longer term you need a high proportion of growth assets (though you will be exposed to more ups and downs).

- If you’re investing for the short term (approaching retirement or looking to purchase a home) then you need to have a higher proportion of fixed income assets.

Click here to ask Kōura what the best fund type is for you

Historical returns

Getting this decision wrong could cost Ben $180k (that's $123 less per week in retirement!)

Lots of people will choose a fund based on historical performance. The most important rule in finance is that historical performance does not determine future performance.

If you’re going to choose a fund based on the performance you need to look at performance over both the short and long term. It’s easy for a fund to be lucky for 1 or 2 years, though it is very hard for a fund manager to consistently beat the market over a long period of time. In fact, research shows that it is almost impossible. If you’re selecting a fund manager based on historical returns, you’re effectively saying that fund manager is more skilled than the rest of the market. You need to hope that they will still have the skills for the duration of your KiwiSaver investment, which is a very long time!

The investing world is split into two separate camps: the active world and the passive world. Passive investing is when a fund manager invests in a market index rather than picking individual stocks. Research consistently shows that very few investors outperform the market over the medium term, particularly after taking into account fees so passive investing is becoming the norm rather than the exception. For more detail on this topic see our post, What is passive investing and why is it good for me?

Key points:

- Research shows that people very rarely outperform the market over the long term. Historical performance is often not a good indicator of future performance.

- If you’re going to use historical returns to choose your fund, make sure you look at both the short term and long term performance of that fund.

Fund Fees (not fun fees)

Getting this decision wrong could cost Ben $58k by the time he retires (enough for several great holidays in his golden years!)

Fees are an important metric to consider as they are a fixed expense that will be deducted each and every year. Until very recently KiwiSaver providers haven't been very transparent with their fee structure though that's changing now thanks to regulations that require providers to mention their fees as a dollar amount in their statements, making it easy to understand for everyday folk. Investment performance will fluctuate, and funds will have periods of strong performance and weak performance, but fees are a constant and hence an important consideration.

In thinking about the fees you need to consider a few different components:

- The management fee - most funds will charge a management fee based on the assets in your KiwiSaver account. The average KiwiSaver fund fee is 1.19% though it can go as high as 2.0% for some growth funds

- The administration fee - many funds will charge an administration fee to recover some of the costs of administering the accounts. These fees average $27 per member per year, though can range from $0 all the way up to $49.80 for some providers.

- A performance fee - a number of the growth funds will have performance fees in place. If the fund performs above a certain threshold then a portion of the return is given to the manager as a performance fee. This can make a significant difference - one provider that charges a performance fee has seen their annual fees grow from 1.1% to 1.5% as a result of the performance fees

Fees are important because they will always need to be paid irrespective of how the fund performs or how much you have contributed to your KiwiSaver plan this year. This is especially important if you open a KiwiSaver account for your child but don't make regular contributions. In some cases, the fees may end up materially reducing the balance your child ends up with, which is why you need to consider how much you can really contribute before you open an account for your child.

Key points:

- Make sure you review and understand all of the components of the fees.

- If you’re investing in a higher-priced fund, make sure you understand why that is the case.

How does Kōura stack up against these considerations?

| Choosing the right type of fund | Kōura is unique in the market, we have a digital advice tool that will create a personalised portfolio to match your personal objectives and profile. Our tool will give you honest and impartial advice to help you make the most out of your KiwiSaver account. |

| Historical returns | Kōura is a new KiwiSaver scheme so we do not have historical returns to compare with. Though we are a passive investor which means that we will perform in line with the market over time. Interestingly, the average KiwiSaver growth fund has underperformed the market by 1-2% over the past 5 years5. So we are pretty confident that our passive investment strategy will allow us to deliver better than average returns for our investors |

| Fees | Kōura has an asset under management fee of 0.63%, a little over half the average management fee of the growth funds in the market. We also charge a $30 annual administration fee which is broadly in line with everyone else in the market. |

If you want help making the right decisions with your KiwiSaver account, come and ask Kōura. We will develop a personalised portfolio that is right for you allowing you to maximise your financial future, giving you hundreds of thousands more dollars to play within retirement.

[hubspot type=cta portal=5033855 id=fa1b6a4c-f6e7-4d5f-8361-86a4b53afd00]

Notes

- Base case assumptions: Ben earns a salary of $80,000 and invests 3% (matched by his employer) from the age of 30; Investment portfolio matches the Kōura neutral glide path; Return assumptions are in line with FMA assumptions (5.5% for equity portfolio, 2.5% for fixed income portfolio, 3.5% salary growth, 2.0% inflation)

- Wrong fund type assumes investments remain in a conservative fund for the duration of the investment horizon rather than in an appropriate fund type

- The worst performing fund takes the difference between the Morningstar average 10-year returns for growth funds (10.6% as at 30 June 2019) and the worst performing fund over the 10 year period (8.5% per annum)

- Highest cost fund applies the difference between Morningstar average growth fund fees (1.19%) and the most expensive fund (1.77%)

- Based on Morningstar analysis of average growth funds performance versus the Morningstar Multi-Sector Growth Index (1 year Avg Return of 7.4% vs Index return of 9.0%, 3 years Avg Return of 10.0% vs Index return of 11.0%, 5 years Avg Return of 9.6% vs Index return of 10.5%