Inflation bites: Thinking of reducing or stopping your KiwiSaver contributions?

Inflation bites: Thinking of reducing or stopping your KiwiSaver contributions?

2 Nov 2022

Inflation bites: Thinking of reducing or stopping your KiwiSaver contributions?

Data shows(1) that three million people (60% of the New Zealand population) are now invested in KiwiSaver – that’s pretty impressive! But, there’s a ‘but’…

1,862,129 members didn’t contribute anything in the year to March 2022, up 25% from the year before. And it’s not the only big red flag: the number of members contributing 8% or 6% also significantly fell year-on-year.

Are you thinking about reducing or stopping your KiwiSaver contributions? Pause here. We have something important to tell you first.

-

Why now is not the time to give up on retirement – Inflation is affecting Kiwis’ finances in unprecedented ways, but it’s still important not to ‘throw in the towel’ on your long-term goals.

-

Understanding the long-term impact – While reducing or stopping your contributions may give short-term respite to your budget, it may not be worth the long-term consequences.

-

Calculating how much you need – At the end of the day, contribution reductions or ‘breaks’ take you further from your retirement goal. And that’s why knowing and keeping your ‘magic number’ in mind is all the more crucial.

Don’t throw in the towel on your retirement

The latest KiwiSaver findings are concerning, but not surprising. Inflation is (largely) the villain in this story, cutting into people’s budgets and outpacing growth in pay. But while there’s no denying that affordability has become an issue for an increasing number of people, if possible, it’s important not to put your long-term goals in the backseat.

Your financial future may feel less ‘tangible’ than your current needs, but it will be determined by today’s decisions – including how much you choose to contribute into your KiwiSaver plan. And it’s not just about regular contributions: you also earn returns on the returns you earn over time. So, the more you contribute, the more opportunity your money has to grow. It’s the ‘magic’ of compounding.

This also means that any reduction or break you take from KiwiSaver contributions translate into an even bigger missed opportunity to save. In many cases, the short-term respite you get may not be worth the long-term consequences.

Understanding the long-term impact

To illustrate the long-term impact of reducing or stopping your KiwiSaver contributions, let us introduce you to Kaia and Jim.

The impact of reducing contributions

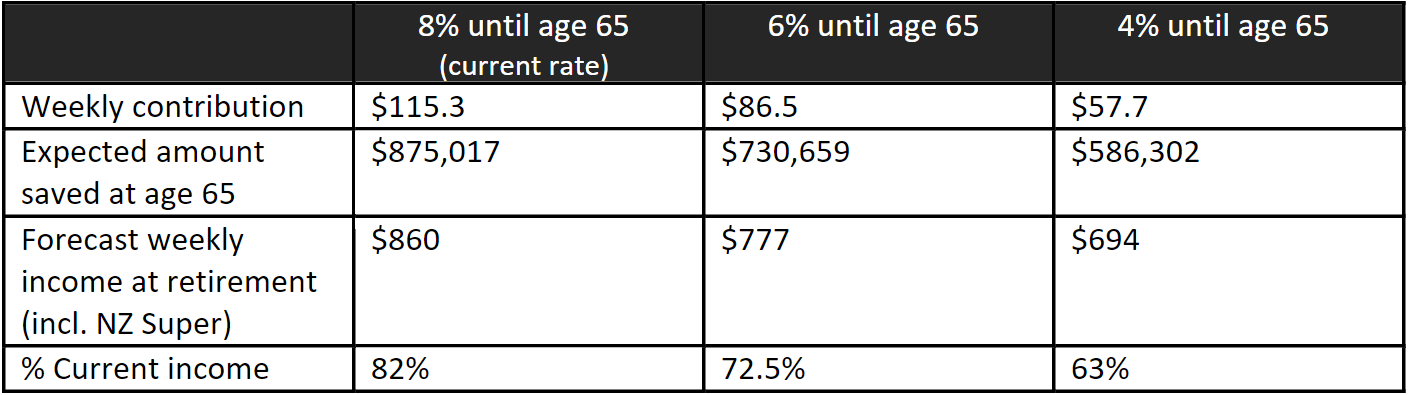

Kaia is 35, is invested in a growth KiwiSaver fund, and has a KiwiSaver balance of $30,000. She earns $75,000 and, up until now, she has been contributing 8% of her salary. This year, some unexpected expenses cropped up and her living costs have also increased. So, she’s thinking of moving down to 6% or 4%.

This scenario is based on a $30,000 KiwiSaver balance with a starting salary of $75,000 growing at 3.5% per annum between the ages of 35 and 65 using a neutral Kōura glide path. We have used the FMA prescribed returns for our growth assumptions:

- All equity funds are expected to generate a return after tax and fees of 5.5%;

- Our fixed income fund is expected to generate a return after tax and fees of 2.5%;

- Our cash fund is expected to generate a return of 1.5%.

- We assume 2.0% annual inflation, the mid-point of the Reserve Bank of New Zealand’s inflation targets.

As the table below shows, if Kaia reduced her contribution from 8% to 6%, her weekly contribution would be nearly $30 lower, but her expected weekly retirement income would be $83 lower. This means she would only be able to replace 72.5% of her current income, rather than 82% (we’ll talk about this in more detail shortly). And if Kaia decided to move to 4%, she would contribute about $58 less per week into KiwiSaver, but she would have $166 less in her weekly retirement income.

It's important to note that you can change your contribution rate once every three months, unless your employer agrees to a shorter timeframe. So, Kaia can revert to 8% as soon as her finances allow it. But even a small break can have an impact and take a bit of wind out of her ‘compounding’ sails.

So, it’s crucial to consider other options first. It all starts with a budget: it may not always be possible, but by taking a closer look at where your money is going every month, you might find ‘hidden’ opportunities to free up cash and let your retirement nest egg grow.

The impact of taking a ‘contribution break’

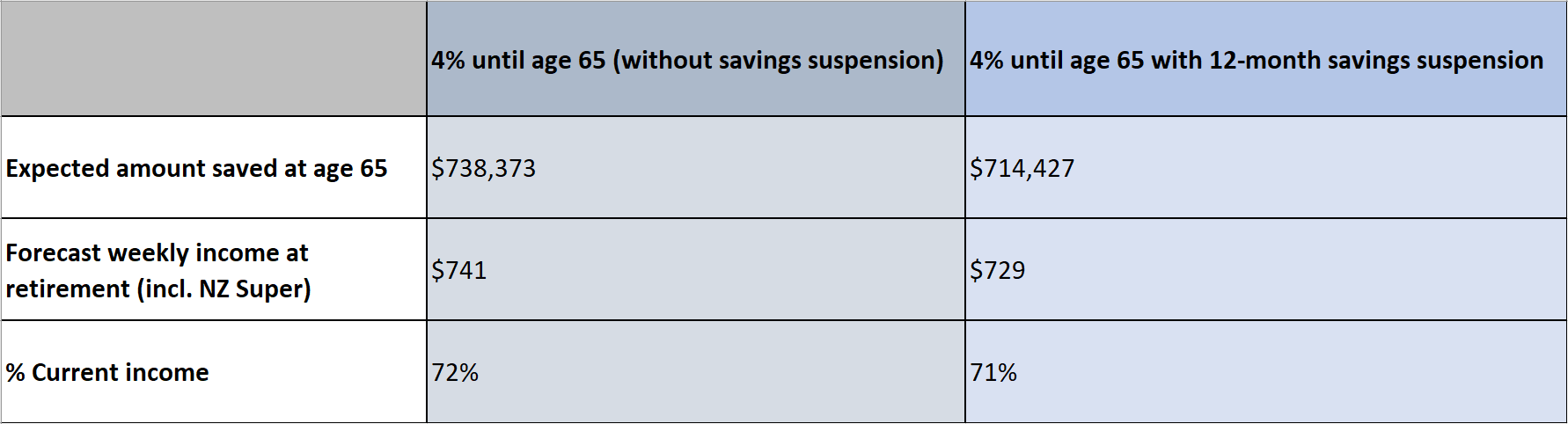

Meet Jim, a 30-year-old earning $70,000, invested in a growth KiwiSaver fund and with a KiwiSaver balance of $20,000. He’s contributing 4%, but is considering requesting a savings suspension of 12 months. This would mean that Jim’s employer contributions and the Government annual contributions will also stop. Here’s the long-term impact this may have on Jim’s retirement savings.

- All equity funds are expected to generate a return after tax and fees of 5.5%;

- Our fixed income fund is expected to generate a return after tax and fees of 2.5%;

- Our cash fund is expected to generate a return of 1.5%.

- We assume 2.0% annual inflation, the mid-point of the Reserve Bank of New Zealand’s inflation targets.

Stopping contributions for 12 months saves Jim $2,800 over the course of his contribution holiday, but he also loses the earnings on that $2,800 which means the total cost to him is actually $24,000 in terms of lost KiwiSaver. So, it’s always worth avoiding a contribution break if you can. While stopping contributions can provide respite in times of need, it’s essential that this option remains the ‘last resort’.

Calculate how much you need

Let this be a bump in the road, not a roadblock

Sources:

-

Financial Markets Authority – KiwiSaver Annual Report 2022

-

Stats NZ – Consumer price index: September 2022 quarter