Investing in difficult times

Investing in difficult times

13 Nov 2022

Investing in difficult times

There’s no missing it: investment markets have been on a rocky ride this year. So, here are some insights and practical tips to invest in tough times.

In this guide, we’ll put things in context, starting with understanding what ‘bear markets’ actually mean. Then, we’ll move on to four sound investing principles that are all-the-more crucial during times of volatility: keep emotions under control, avoid market-timing, don't stop investing, and diversify your portfolio. So, let’s get started.

A summary of key takeaways:

-

Understanding bear markets – Did you know that there have been 26 bear markets since 1928? Read on for this and other interesting facts.

-

Controlling your emotions when investing – Easier said than done? Our tips and insights may help you put things in the right perspective.

-

How market-timing almost never works – By trying to time the market, you may actually miss the best days in the markets, missing out on significant opportunities.

-

Why you’d be nuts to stop your KiwiSaver contributions now – During bear markets, investments are on sale and you can buy at a lower price.

-

Why diversification is so important in times of volatility – Diversification is always crucial for investing, and even more so when markets are volatile and uncertain.

It’s time to understand bear markets

As you know, investment markets go through cycles, which are measured from peak to trough. When prices go down by about 20% from their most recent high, we say that the market is a ‘bear market’, whereas a ‘bull market’ is defined as a gain of 20% or more.

The origin of the term ‘bear market’ is a fascinating one. According to one theory(1), it may come from the proverb “Don’t sell a bear’s skin before one has caught the bear”. In the 18th century, ‘bearskin’ was used as a metaphor for speculative stock buying. Another theory tells us it’s because bears attack by swiping their paws downward, while a bull thrusts its horns upward.

Either way, a bear market is not a rare event: it’s a natural part of the sharemarket lifecycle. Here are some interesting facts to consider(2):

-

There have been 26 bear markets in the US since 1928. That’s an average of one every 3.6 years, though bear markets have become less frequent recently, with only seven such events since 1974 (one every 6.7 years). There have also been 27 bull markets in the same period.

-

On average, shares lose 36% in a bear market, and since 1928 the market dropped over 50% only three times: 1931, 1937 and 2008.

-

Bear markets tend to be shorter than bull markets: 9.6 months on average compared to 2.7 years.

-

The average share market performance for the three months post-hitting rock bottom was 26%, which shows just how hard it is to time the recovery (we’ll come back to this shortly).

-

There are typically at least three or four ‘false starts’ where markets rally by 10% more in the middle of a bear market, before quickly falling below previous troughs. These are called ‘bear market rallies’.

Interesting, isn’t it? Of course, past performance is never indicative of future performance. But based on data collected since the Great Depression of 1929, a KiwiSaver member invested from the age of 20 to 65 can expect to see through 7-12 bear markets along their KiwiSaver journey.

As unsettling as bear markets can be, they happen. And when they do, it’s all-the-more crucial to ignore short-term movements and focus on the long journey ahead. Which brings us to the next point…

Controlling your emotions when investing

There are many things more fun than seeing your KiwiSaver balance or the value of your investments drop. Your first instinct may be to run for cover, trying to hide your hard-earned savings from the raging storm by switching to lower-risk options.

We saw this happen in the Covid-related downturn of 2020: the sudden market drop caught many KiwiSaver members off guard, prompting them to de-risk their KiwiSaver plan. So, when the markets bounced back just a few months later, they missed out on the recovery. Of course, no one could know that the downturn would be so short-lived. But that’s the point: markets do recover, we just don’t know when. And to avoid turning ‘on paper’ losses in real losses, the key thing is to stick to your long-term strategy.

When investing, more often than not, giving in to your emotions means making short-term and at times irrational decisions, which will impact your long-term performance. So, how can you keep emotions under control? Let’s take a closer look.

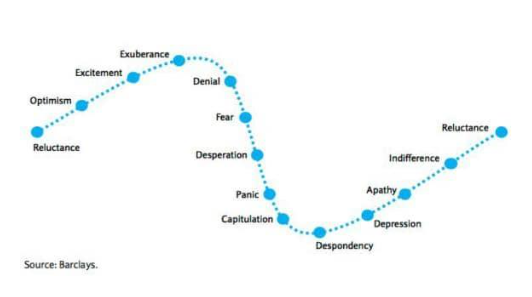

The average cycle of investor emotions

According to Barclays(3), investors experience emotions in four stages. Do any of these ring a bell?

-

Reluctance – This is the default state for many would-be investors, when the fear of taking risks and getting it wrong is more prevalent than the ‘fear of missing out’.

-

Optimism, excitement and exuberance – In bull markets, the initial reluctance wanes and gives way to a new stage of optimism. Concerns over losses and risks are put aside, and more people are willing to enter the market.

-

Denial, fear, desperation and panic – When markets turn volatile, reality suddenly bites, pushing investors to move into denial. And the only way is down from here: scared of future losses, the average investor sells out.

-

Capitulation, despondency and depression – Once they’ve cashed in, investors usually don’t get back to a state of optimism right off the bat. First, they’ll need to go through periods of apathy and indifference, before returning to reluctance once again. Rinse and repeat.

Types of emotional decisions

Emotions vary from person to person, but these are some common emotional decisions that might sabotage your future returns:

-

Trying to time the market – Market movements are by nature unpredictable, so it’s impossible to pick the highs and the lows. And there are consequences to trying and missing the mark. Vanguard analysis(4) of investor behaviour before and after the height of the GFC (2004-2013) found that the average market-timing investor was at least 0.5% a year worse off, whereas their buy-and-hold counterparts were 0.5% better off.

-

Following trends – Once again, past performance is not a guarantee of future performance. Make sure you don’t invest in something because of great historical returns or because everyone is doing it.

-

The broader fear of investing – To get over a certain risk aversion, the best way is to understand that time is your friend. Market risk is an unavoidable component of any investment journey, but it can also be managed and transformed in an opportunity.

How to avoid emotional investing

As we talked about in more detail in our recent article Breaking the cycle of emotional investing, there are steps to rein in your emotional response. Here are some practical examples:

-

Don’t look at your investments too often – Seeing your KiwiSaver balance fall in value almost in real-time can trigger an emotional reaction, and it does make for a rather uncomfortable long-term ride. In most cases, checking in once a year is more than enough.

-

Build your investment strategy – Write down your long-term strategy, set up your KiwiSaver plan accordingly, and then leave it be until your next annual reassessment.

-

Invest in funds rather than individual shares – As former CFO at Morningstar, Patrick Geddes suggests(5), investing in funds can help take the decision-making out of it, reducing the need to constantly look at your investments.

-

Temper your expectations – As we’ve seen, bear markets happen and will continue to happen, most likely till the end of times. So, keep this possibility always on your radar: it will make it easier to stay the course when that finally happens.

Why trying to time the market almost never works

We briefly talked about timing the market as one of those common emotional decisions that can easily derail your long-term plans.

The evidence against market-timing continues to mount, and we know now why this strategy doesn’t work. As the chart below shows(6), by trying to get in and out at the right time, you’re likely to miss the market’s best days – further proof that the better way to go is to simply stay invested.

Looking at the way back to 1930, if you had excluded the 10 best days in each decade, just one day per year, your return would have fallen from 17,715% over the period down to just 28%.

In other words, if you had started investing in 1930 with $1, and left it invested throughout the entire period, by 2021 you would have had $177 – 177 times (+17,715%) your initial investment. But if you had tried to time the market and missed the best 10 days in each decade, which is highly possible, your return would have only been 28% and your $1 would have turned into $1.28.

That’s how big a missed opportunity market-timing can lead to.

The markets are on sale: why would you stop contributing now?

Imagine there’s a big sale at the supermarket: for an indefinite time (anything from one day to months or years), the price of all products is significantly lower than usual. You also know that, at some point in the future, prices might increase again.

Would you continue to buy those products or wait until their prices are going up again? The same principle applies to investment markets. And yet, many investors seem to shy away from the markets when prices are down.

Historically, markets have always recovered, with the typical period from peak to recovery being three or four years. So, think about it for a second: if markets are down 30%, that means that you’re highly likely to make 30% on your investments over the next three to four years as markets recover.

When it comes to your KiwiSaver plan, by continuing to contribute (or even increasing your contribution rate if you can afford it), you’re effectively buying units at a lower price. Which means those will have more margin to accelerate when things pick up again.

Why diversification is so important

Finally, while you can’t control the volatility in the market, what you can do is manage the volatility in your portfolio – through diversification. It’s all about not putting all your eggs in one (fragile) basket.

As we’ve seen, hiding your money from investment risk is impossible. But there are opportunities to seize, if you bend the risk-return trade-off to your advantage. In the same market conditions, some investments tend to perform better than others. Rather than fleeing investment risk, the goal of diversification is to give you a wide exposure, so that bad returns from one investment are offset by the returns from others.

Diversification allows you to spread your money around by investing across a wide range of asset classes, sectors, and regions. Yes, regions too: it’s not just individual companies or sectors that experience volatility from time to time. As the Japan 1990s market crash showed us all, entire markets can be equally volatile.

To find out more about diversification, check out our other article Why diversification is so important right now, where we also talk about some lessons you can learn from past ‘market darlings’ like Tesla and Facebook/Meta.

Let’s create your diversified KiwiSaver portfolio

For our Kōura personalised portfolios, we use more than 200 proven portfolio strategies, based on a number of global investment and domestic KiwiSaver scheme models. And getting your personalised portfolio only takes a few minutes.

Use our digital advice tool to check what your KiwiSaver plan is on track to give you, and the recommended portfolio composition for your risk profile, needs and goals.

[hubspot type=cta portal=5033855 id=db7e955c-e95e-4fb0-a5ee-3e32514f0e4b]

Further reading:

(1) CNN.com – How bears and bulls became Wall Street’s mascots

(2) S&P 500 Index declines of 20% or more, 1929-2021, found on Hartfordfunds.com (“10 Things You Should Know About Bear Markets”)

(3) Barclays.co.uk - Understanding the cycle of investor emotions

(4) Vangard.com.au – The true cost of market timing

(5) CNBC.com - Here are 3 tips every young investor should follow to avoid emotion-based investing

(6) Bank of America, S&P 500 returns, found on CNBC.com (“This chart shows why investors should never try to time the stock market”)