July market update

July market update

10 Aug 2021

The Covid Delta variant sparks fear, China tightens the leash on big tech, and the U.S maintains its consistent winning streak

July market update

A lot happened towards the end of July so before we dive into the detail, here’s a super quick summary of how it ended by region:

- China - Down (due to regulation)

- US - Up (good earnings reports)

- Rest of World - Sideways (Mixed bag, but positive earnings reports as well)

- NZ – Sideways (Gains offset by downflow effects from Chinese regulations)

China is in the process of implementing new regulations that will restrain monopolies, better govern fintech firms, and protect data privacy. The NASDAQ Golden Dragon China Index (which tracks 98 of China’s biggest firms listed in the U.S.) plunged 22% (or $354 billion) in July and the broader Chinese market fell 6.05% and left investors scrambling and wondering where this regulatory crackdown might end.

While in the US, the S&P500 successfully managed a 6 month winning streak for the first time since 2018, finishing the month 2.38% higher.

Kōura fund updates

[1] Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4% Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%

China - The tiger fights back

It was a tough month for Chinese stocks as an increasingly assertive Chinese Communist Party continued its clampdown on foreign listed and tech companies.

China has signalled it will continue to make it harder for Chinese companies to list on U.S. stock markets, which would limit their ability to grow and raise capital outside China, new proposed rules would require nearly all companies seeking to list in foreign countries to undergo a CAC (Cyberspace Administration of China) cybersecurity review to ensure appropriate data protection measures are put in place.

The first tangible example of this new crackdown was felt by market-leading ride-sharing app Didi – China banned any new downloads of the popular ride-sharing app in the Chinese market until data security issues are resolved, this all occurred 2 days after its very successful US IPO (which the CCP had requested Didi to delay).

And finally, the CCP has banned all private company involvement in education, stating that all tutoring and education companies operating in China must be non-profit.

Why the new regulatory approach?

The new more assertive regulatory playbook started in late 2020 following Alibaba’s CEO Jack Ma’s unthinkable decision to publicly criticise the Chinese Government and its approach to financial regulation. Since then, the regulatory interventions have grown.

The Chinese Big Tech companies are even bigger and more powerful in China than the Western versions (Google and Facebook). The Chinese tech players platforms span as wide as payments, asset management, social media, search and gaming, a much broader set of services than any of their Western peers. These companies have become so big and powerful with vast amounts of consumer data they are increasingly being looked at as monopolistic beasts crushing innovation and skirting regulation (similar to the Western versions) whilst also having the potential to take on the Government and create social unrest.

So, you choose whether the crackdown is an attempt to protect data and consumer rights, or simply the CCP reasserting its dominance over a few companies that might have thought they were too powerful to be touched.

How the regulations impacted markets

The downstream effects are scary news for investors, this is tangible evidence that the cost of doing business in China has grown due to potential government interference.

Two days after DiDi successfully raised $4.4 billion in their IPO (becoming one of the largest overseas listings for a Chinese company since Alibaba) the ban on new downloads was implemented and DiDi shares fell a crushing 30%. The shares remain 35% below its $14 IPO price.

In recent weeks, 5 firms have been axed from their IPOs with a combined value of $1.4 billion, and another 17 who were scheduled for this year are now anxiously awaiting their fate.

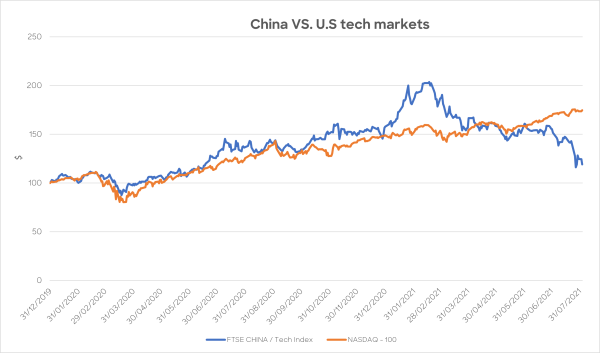

The below graph of ‘China VS U.S tech markets’ visually shows how China and the US tech stocks have historically moved in line with each other, until 2020 when China peaked due to outpacing the world with its Covid-19 economic recovery, swiftly followed by its decline due to tighter monetary policies, and now these new big tech regulations.

U.S

The US markets had another strong month with the SP500 on a 6-month streak of month-on-month gains, finishing the month 2.38% higher. The end of July saw the busiest week for the second-quarter earnings season with one-third of the SP500 companies reporting results, including some of the biggest tech names. 87% of them have exceeded earnings estimates by an average of 18%.

However, all of the good came with a little bit of disruption. Covid-19’s new Delta variant caused a mid-month sell-off (when people perceive impending risk and sell off their shares) which shook the markets briefly. And of course, the Chinese regulations caused market disruption as well, though this remained insulated to companies with high Chinese exposure.

US Economic Data

US weekly unemployment numbers rose unexpectedly in the middle of the month acting as a reminder that the US labour market is still not out of the woods.

Incredibly, 6 quarters after the most devastating economic shock ever experienced, the US economy has recovered and Q2 economic output (as measured by GDP) was higher than the previous peak experienced in Q42019. It is expected that growth in the second half of the year will slow down but it is still amazing to reflect on where we have been and how even from these elevated levels, can still expect a further 6-7% growth over the next 12 months.

Europe

European stocks hit all-time highs after strong earnings from commodity majors. Strong quarterly earnings and optimism around Europe reopening put the STOXX 600 on course for its sixth straight month of gains, ending the month up 2.07%.

In England, the lifting of many Covid restrictions, dubbed “Freedom Day,” was marred by new restrictions on travel to France and other countries due to the delta variant. From August the UK is allowing most travellers who have been fully vaccinated in the U.S. and Europe to enter England, Scotland, and Wales without having to quarantine, however even with all this positive news, the UK FTSE 100 was only up 0.07% for the month.

Overall, the Eurozone economy bounced back from recession in the second quarter, growing at a rapid pace, 2% faster than the first three months of the year. Inflation heightened to 2.2% in July from 1.9% in June and was primarily driven by higher energy prices.

NZ

The NZX ended the month 0.5% lower. It was a very mixed bag with a number of winners and losers in the month.

Z Energy held an investor day and gave strong guidance on its ability to retain earnings whilst transitioning away from oil in addition to its guidance that moving to import only fuel will allow it to release c.$200m of inventory. This news was liked by investors with Z Energy up 7.7% in the month.

Mainfreight’s strong performance continues, with the stock up 7.3% in the month off the back of strong earnings guidance delivered at its AGM. Its 12-month return is now a staggering 77%. Shares in infant formula brand A2 Milk were down another 4% taking their 12-month loss to 70% driven by an elevated risk around A2 Milk’s ability to renew its registration with China’s market regulator next year, which allows the company to sell its baby formula in Chinese retail outlets.

Another big faller were Fonterra units which continue to reel from the capital structure review. The units have fallen 37% over the past 3 months as investors worry about what will happen to the units and will be waiting for Fonterra to announce what price it will repurchase the units at (if at all).

Following the suspension of the quarantine free travel from Australia towards month-end, travel stocks went south with Sky City and Tourism Holdings both falling 7.1%.