The kōura market wrap for June

The kōura market wrap for June

5 Jul 2023

The bulls are back, but have they won?

China shop owners should lock their doors because the bulls are well and truly back!

June was a great month for the markets with global markets lifting by almost 6% taking us well and truly back into bull market territory. Markets are now up over 23% from their October peaks and remain only 4% below their January 2022 highs. Markets were driven by ever-strengthening economic outlooks. Economic data continues to show that the global economy is strong and the much-feared recession keeps on getting pushed out further and further away.

This is great news for all the KiwiSaver members who have managed to ride this uptick and should all now have KiwiSaver balances significantly higher than 12 months ago.

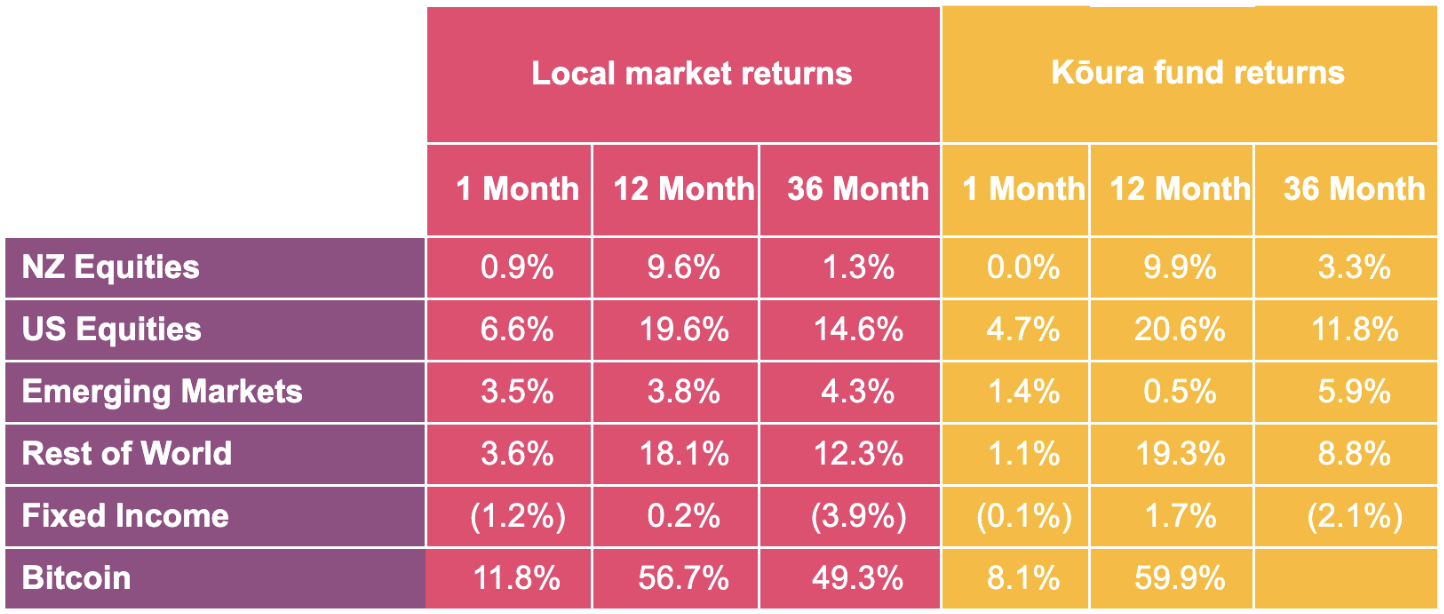

Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ.

Local market returns use the relevant market indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index.

So what are some of the things that we have been looking at over the past month?

Economic data continues to show resilience.

Economic data around the world continues to outperform and shows that the economy is standing up to higher interest rates significantly better than expected. Whether it be GDP estimates, unemployment rates or manufacturing surveys, the data continues to beat estimates. Even the highly interest rate sensitive housing sectors are starting to pick up, with the US (and hopefully New Zealand) starting to come out the other side of the housing market troughs.

All of this is causing economists and market analysts to push out their timing of the impending recession. The most talked about recession of all time continues to be pushed back and some are now suggesting that it may not turn up at all.

It is truly staggering to think that the global economy will still grow at 2.5% this year despite the 4% rise in interest rates across most countries.

Globally, interest rates are starting to go up

The flip side to better economic growth is that core inflation remains high and seems to have stalled at levels much higher than where central banks are or should ever be comfortable.

Central banks have been looking for unemployment to increase to drive out excess demand, but unfortunately that has not been happening. As a result, Central Banks are continuing to need to push interest rates higher and higher.

The Reserve Banks of Canada and Australia both lifted interest rates in June, despite previously announcing that the rate hiking cycle was over.

In the US, Jerome Powell took a break in June and did not raise interest rates, though stated he expected another 0.5% of rises through the remainder of the year to get inflation under control.

Interestingly, market now interpret higher interest rates as good news as it signals stronger economic growth. Over 6 months ago, higher interest rates was what the market feared the most, now it seems the world has turned.

The market recovery is starting to broaden

More sections of the market are now starting to show signs of an improved economic situation.

Up until the start of June 75% of the US market performance was down to a handful of tech stocks. But throughout the month we saw that rally broaden with the smaller company orientated fund Russell 2000 significantly outperforming the broader market. The Russell 2000 delivered a return over 8%, prior to June the Russell 2000 performance had been relatively flat year to date.

One of the biggest criticisms of this market rally has been its concentration among the tech mega cap companies. Focusing on the performance of the major tech funds can disguise the fact that the largest recovery rallies have been the biggest companies on the block, with smaller ones not doing as well.

But June saw this criticism dispelled with performance broadening out among the broader market. This is a key requirement for a long-lasting market recovery.

New Zealand is in a “technical recession”

Mid-month came the announcement that many had anticipated proving that New Zealand is technically in a recession.

A recession is called when you have two quarters of negative GDP in a row. This is difference from other countries where a board of economists “call” a recession and will take into account business sentiment and employment data.

This is being referred to as a “technical recession” because it was based on a 0.1% negative GDP print. So it really is only just negative and we are yet to see any impacts on the employment market.

Typically, recessions are accompanied by significant upticks in unemployment. Whilst the economic picture is not overly rosy, it does not have a recessionary feel to it just yet (it does help if you ignore the media reporting on it too!)

Crypto could be about to go mainstream

Crypto had another stellar month with Bitcoin extending its Year to date gains up to 84%. The price raised above US$31,000 for the first time since early 2022 following news that Blackrock had filed to launch a spot ETF on the Nasdaq.

Rather than being dead, it appears that traditional finance has spent the past 12 months of crypto winter building out new products and custody solutions to attract a whole new investor during the next uptick.

The US SEC continues to battle against Binance and Coinbase with their lawsuits threatening both business models.

In essence the SEC has said that most crypto tokens are in fact securities, therefore investors should have the same level of protections in place that traditional securities law provides.

In my mind, this is a great thing and is a key necessity for allowing crypto to move to the next stage in its evolution.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.