Our Christmas wish list

Our Christmas wish list

24 Dec 2020

We’ve been nice, we promise, now we want the government to be nice to New Zealand’s financial future

Christmas at the Carlyon household is an exciting time, but a negotiation. My kids, bless their souls, have a wishlist longer than they are tall, and Santa Claus only has so many hands and dollars in his jolly pockets to bring all of these lovely things down the chimney.

Corporate Chrismas is not really different. Large organisations, both naughty and nice have their own long luxurious wishlists. And it’s up to the politicians to figure out how they can keep the kids happy while benefiting the most people possible.

Here at Kōura, we do promise we’ve been nice, and we’d like to ask for just a few things that will make us very happy on Christmas day. Our list is shorter than most, but they aren’t self-serving, they’re aimed at the financial wellbeing of our nation. At the top of the list and written in bold is the request for the Government to finally take KiwiSaver seriously and make the necessary changes to ensure that Kiwis get the retirements that they deserve. Before we go through this, it is essential to recognise that we all benefit from a successful KiwiSaver. If we succeed in making KiwiSaver a better product, we will:

-

End up with a higher domestic savings pool that can be used to help out in times of emergency or invest in infrastructure. Australian Superannuation funds invested over $130billion into Australian companies during the Global Financial Crisis, helping companies emerge through the recession.

-

Reduce the reliance on New Zealand’s increasingly stretched super scheme which will become harder and harder to afford as our population ages. Before we make any changes to the age of eligibility or means-testing our current Superannuation scheme, we need to ensure the alternative is fit for purpose.

The problems

1. Participation in KiwiSaver

New Zealand is one of the very few countries in the world that does not have a mandatory retirement saving scheme. To a certain extent, this is because we also have one of the most generous universal pension schemes in the world. New Zealand Super pays out 39.9% of the Average Wage; for the other nine countries in the OECD that payout universal benefits, the average is closer to 15% of the average wage. The other 26 countries in the OECD have targeted Government-sponsored retirement schemes combined with mandatory private savings programs.

In New Zealand, there are currently more than 3 million people enrolled in KiwiSaver, and the only 59% of them are regular contributors. This means that they are either living overseas or contributing the bare minimum to receive the $541 annual Government Contribution.

In our view, we can do three things to better incentivise people to contribute.

- Make the scheme mandatory. New Zealand is one of the only countries in the world which does not have a mandatory retirement scheme.

- We return to the original KiwiSaver settings introduced in 2007. Contributions will be matched up to 4% without the ability to contract out of KiwiSaver.

- Create tax incentives to encourage people to contribute. In the 12 months to 30 June 2020, there was $4.16b contributed to KiwiSaver. Assuming everyone is taxed at the top marginal tax rate (which is unlikely), there was a maximum of $1.3b of tax collected on those contributions. The Government could follow Australia and reduce the tax rate to KiwiSaver down to 15%, this would result in $0.7b of lost tax, and arguably more tax lost as more people contribute. Though over the long term, this would be offset by higher growth rates and lower funding requirements to assist older people living in poverty.

2. People do not contribute enough to the retirements they expect or deserve

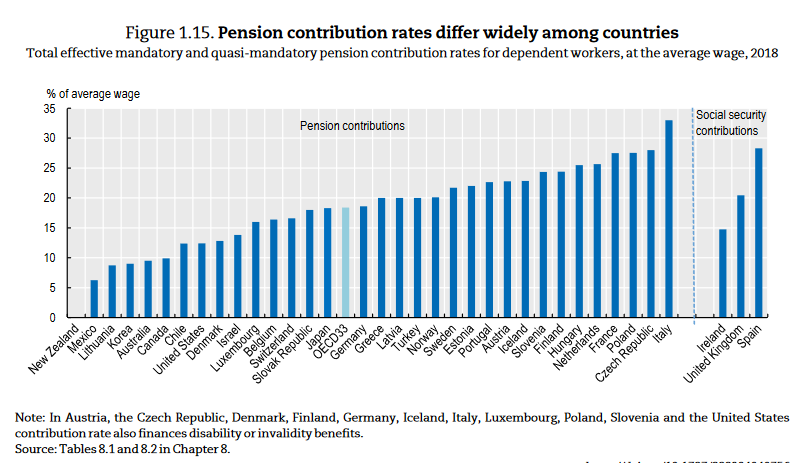

KiwiSaver contribution rates are the lowest rate in the OECD and well below the average OECD contribution rate of 18%. In Australia, contribution rates will grow to 12% of salary by 2025.

To a certain extent, New Zealand’s low contribution rate is offset by the fact that NZ Super is funded out of general taxation rather than a specifically focused fund.

Source: OECD Pensions at a Glance, 2019

The scary thing is what people will get from their KiwiSaver; many people assume that their retirement is sorted because they contribute to KiwiSaver. A recent survey we did found that 68% of people saw KiwiSaver as being very important for their retirement, the same survey showed that 49% of people under the age of 45 had no savings at all for their pensions.

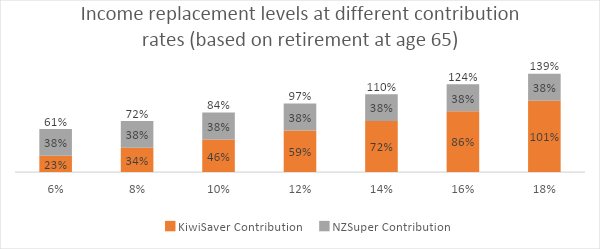

From our discussions with people, it is clear that people think that participating in KiwiSaver is sufficient and just by participating in KiwiSaver they have dealt with their retirement. Research from Massey University shows that a two-person household will need between $710 – 1,200 per week to have a comfortable retirement (depending on the single or 2-person household), of this, $316 – 411 will be provided by NZ Super, with the remainder needing to be provided by private sources. For the average Kiwi earning $60,000, who starts contributing at 20 years old (after they have purchased their first home) they will need to contribute c.13% of their income to achieve that level of income.

Source: Kōura analysis

-

Based on a glide path approach using FMA approved returns (5.5% for equity and 2.5% for fixed income returns)

-

The average salary of $60,000 growing at 3.5% per annum

We would like to see changes made to contribution rates to ensure that KiwiSaver delivers what people expect of it. In action, this would look like the gradual increase of contributions to 6 + 6% over time, in line with the Australian model.

3. People are not engaged with or understand their KiwiSaver, which means they do not make the necessary decisions.

An ASB survey in late 2019 showed that only a quarter of Kiwis have a good understanding of KiwiSaver. The same survey showed that investors believed bank term deposits would deliver the same returns as KiwiSaver funds over time.

This blatant lack of understanding reared its ugly head back in March during the market meltdown when up to 10% of customers switched out of growth funds into conservative funds.

By switching then, they effectively locked in their losses and missed out on the gains enjoyed by customers in growth funds as the markets have recovered. It is estimated that these customers have missed out on billions of dollars in returns cumulatively.

We put the lack of engagement and understanding down to 3 simple reasons:

- The default structure which allows people to tick a box and never think about their KiwiSaver again. At the same time, default funds are meant to educate and communicate with their customers, though they have had a very poor rate of communicating with their customers. Over 20% of customers remain in default funds, and providers only increased their efforts to move customers following pressure from the FMA and current review of default processes. Still, providers have only lifted their success rate to 15% - far too low, given they have been given large customer bases and are making millions of dollars in fees from these customers.

- The dominance of banks in this space means that customers believe that KiwiSaver is another bank product. This is made worse by the fact that banks will offer discounts on mortgages if a customer transfers their KiwiSaver and have untrained branch tellers selling KiwiSaver to customers.

- The digital signup process preferred by most providers puts fund selections as an afterthought. We need to change the sales process to place an understanding of our customers and helping them make better financial decisions at the centre of the sales process rather than using a traditional online sales model.

The changes we would like to see made here are:

- Penalties imposed on default providers if they cannot engage with their default customers and have them actively choose a fund

- Forbid the ability for banks to use KiwiSaver as a cross-sell opportunity

- Allow only trained specialist staff to sell KiwiSaver and ensure individual objectives sits at the centre of each conversation.

- Ensure all digital signup processes ask and consider personal investor circumstances so that investors need to opt-out of the right client outcome, rather than moving outside of the signup process to understand what is the right outcome for them.