KiwiSaver through life: Your 20s

Table of Contents

KiwiSaver through life: Your 20s

4 Aug 2023

KiwiSaver through life: Your 20s

Hundreds of thousands of Kiwis in their 20s are investing in KiwiSaver. Are you one – or maybe just considering joining? Here’s a quick guide for you.

Welcome to your 20s! High school’s behind you and maybe you’re at university, or you’ve made a start on your career. Retirement? That’s miles away. And KiwiSaver? Not at the top of your list now, right? Think again – now can actually be a great time to think about it.

For many 20-somethings like you, KiwiSaver may be the secret weapon for buying that first home. And if you’re already a homeowner, or if homeownership isn’t your thing, the scheme can be your ticket to a comfortable retirement. What you do with your KiwiSaver plan today can make a colossal difference in your future.

As we’ll see, the key thing is to: (1) play it safe, though only if you’re planning to use your KiwiSaver savings to buy your first home; (2) once you’ve bought a home (or if you already own one), attack and get as aggressive as you can. The good news is that it’s not rocket science! Here are some key steps you can take to get on the right track.

1. Like to buy your first home someday?

Choose the right KiwiSaver fund.

KiwiSaver is designed to be used for two goals: buying your first home and/or saving for retirement. Either way, it’s crucial to be in the most appropriate fund for your primary goal, in terms of risk level.

If you’re in your 20s and dreaming of homeownership, you’ve probably heard that KiwiSaver can give your deposit a nice boost. You can withdraw most of your savings, except for $1,000. However, many people don’t realise that, in the lead-up to their withdrawal, they need to protect their savings – which means playing it safe. If you’re planning to buy your first home within the next five years, a conservative or balanced fund is generally more appropriate than an aggressive fund.

Why? Because your investment horizon is short, so your savings cannot withstand much risk (aka volatility). In this case, a growth fund or aggressive fund is not ideal, as they’re more exposed to the global share markets and will therefore experience bigger ups and downs in the short term.

To illustrate the impact of a market downturn on your potential first-home deposit, imagine it’s 2020 all over again. You’re relying on a $50k KiwiSaver balance to boost your first-home deposit. And all of a sudden, Covid-19 arrives. During Q1 2020, the average aggressive growth fund fell 15%(1) meaning that your KiwiSaver balance would have fallen to $42,500. It would have recovered 12 months later, but that is not helpful if you needed to purchase your first home during those scary few months.

While conservative (lower-risk) funds are not immune to market volatility, they’re likely to provide steadier, smaller returns with less dramatic short-term fluctuations. In other words, they can often offer a more predictable savings journey – which is what you need when buying your first home.

Have you just bought your home? Maybe you already own one – or homeownership is simply not in your plans? Well, then your KiwiSaver plan is purely a retirement savings tool now. You’re in for a long ride, so a growth or aggressive fund has the potential to deliver higher returns over time. And given the long journey, you have the time to weather any temporary downturns and come out ahead.

For example, over the past 10 years, the average aggressive fund has experienced significant fluctuations, but it has delivered a return of 8.4% per annum in the same period versus 4.1% for a conservative fund.(2)

This goes to show that, while an aggressive fund is probably not appropriate for a short-term horizon, if you’ve bought your home and your next goal is retirement, your investment horizon is most likely long enough to take advantage of a more aggressive approach (e.g., a growth or aggressive fund, depending on your needs).

2. Start early (or not too late) and stay invested.

Now that you know about the importance of choosing the right fund, let's tackle another critical factor: timing.

Ever heard the saying “The best time to start investing was ten years ago, but the second-best time is today”? It may sound a bit like a cliché, but it’s true. While many people invest a lot of time thinking about strategy, the best strategy is as simple as getting started early and staying invested.

Even small contributions to your KiwiSaver plan can snowball over time, thanks to the magic of compounding returns (your returns are reinvested and generate further returns). So, the earlier you start, the better.

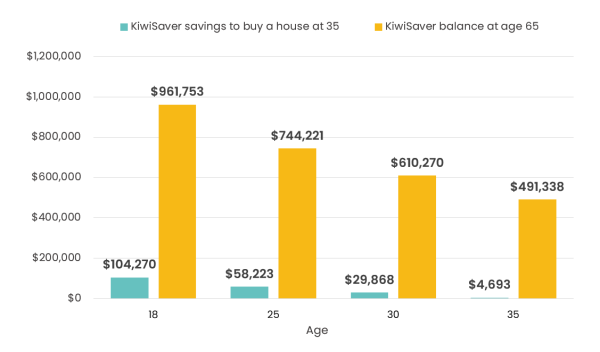

To illustrate this, let’s assume Josh is an 18-year-old with a starting salary of $50,000 (growing at 3.5% p.a. in line with FMA assumptions). Here’s the balance Josh could have for a house or retirement depending on when he starts saving (contributing 3%):

Key assumptions:

-

Assumes that the KiwiSaver member is invested in a growth fund earning 5.5% per annum. This may be too aggressive for a first-home buyer, but is used for comparison purposes.

-

Assumes an 18-year-old with a starting salary of $50,000 growing at 3.5% per annum in line with FMA assumptions, contributing 3% and with their employer matching at 3%.

-

The balance at 65 assumes no withdrawal for first home.

-

All numbers have been shown as nominal numbers, and therefore not adjusted for inflation.

Keep in mind that this is just an estimate and many factors can affect retirement savings, such as investment performance, inflation, and personal expenses. It's important to seek advice, from a financial adviser or through our digital advice tool, and make a retirement plan tailored to your situation.

But as this example makes clear, time is the greatest asset to someone in their 20s. Make sure you use it to your advantage!

3. Make active choices for your future.

Your 20s is a stage of life full of boundless opportunities, adventures, and growth. And amongst all these exciting things, it’s also a good time to take control of your financial future – by actively managing your KiwiSaver plan.

Here are some important steps to take:

-

Make an active choice of KiwiSaver fund

As we’ve seen, choosing the right type of KiwiSaver fund for your goals is crucial. When you first sign up for KiwiSaver, you may be placed into a default fund. This type of fund was always designed as a holding pen, a safe place for your money while you find a more appropriate fund for your needs. Default funds are also usually ‘balanced’, offering a middle-of-the-road approach to risks and returns.

While, in some cases, a balanced fund may be appropriate for first-home buyers, it’s unlikely to be a good option if your investment horizon is decades long. It could mean missing out on potential growth opportunities.

So, the key thing is always to ask yourself: Am I in the right fund for my circumstances? Does the risk level match my goals, investment horizon, and attitude to risk? You can use our digital advice tool to identify the right type of fund for your individual needs and risk tolerance.

-

Choose your contribution rate

You also can control the percentage of your income that you're contributing to your KiwiSaver: 3%, 4%, 6%, 8%, or 10%. Choosing a higher contribution rate can speed up the growth of your KiwiSaver balance. However, this should be balanced against your current financial situation and your other financial goals. Not quite sure where to start? Check out our comprehensive guide ‘How much do I need to save for retirement?’ or use your digital advice tool to run your numbers.

-

Use KiwiSaver to your advantage

The KiwiSaver scheme comes with some pretty sweet perks that can help you grow your savings: employer contributions and annual Government contributions. If you’re employed, your employer will contribute a minimum of 3% to your KiwiSaver balance. Over time, this can add up to a considerable amount, and it’s all extra money that’s helping you grow your savings.

On top of this, the Government also chips in with annual Government contributions. Every year from the age of 18 to 65, if you’re contributing to your KiwiSaver plan, the Government will add 50 cents for each dollar you put in between 1 July and the following 30 June – up to a max of $521.43/year. Think of it as a little bonus for being a diligent saver.

4. Keep an eye on the fees you’re paying.

Like all investment fund managers, all KiwiSaver providers charge fees to manage your money, which varies widely from provider to provider. Since every dollar counts when saving for the future, you may want to ensure that fees are not gobbling up your hard-earned savings.

So, why does this matter so much for you, as a 20-something? Because the sooner you start monitoring your fees, the more you could save in the long run. That’s because you have a long investment horizon ahead of you, and even seemingly small differences in fees can add up to significant amounts when compounded over several decades.

In a nutshell, fees are not the only factor to consider – but they are one of the factors. And by selecting a KiwiSaver fund with reasonable fees, you can maximise the potential returns on your investments over time.

5. Review your KiwiSaver plan regularly.

Your 20s are a time of change and exploration: your KiwiSaver plan is one of the all-important seeds you’re planting for the rest of your financial life. But it will not grow like you want it to, if you just ‘set and forget’.

As you evolve – your career advances, your income changes, your life goals shift – your KiwiSaver plan needs to adjust alongside you. Ongoing reviews can help you ensure it remains aligned with your current situation and future ambitions.

Of course, there’s a lot to think about. So finding a guide, like a financial adviser or a reliable advice tool, can make a lot of difference. They are there to simplify the process, provide essential insights, and help you make informed decisions about your KiwiSaver plan.

Here at Kōura, we have designed an innovative digital advice tool to provide personalised KiwiSaver advice based on your circumstances and goals – just like a human adviser, but with the convenience of being available anytime, anywhere. Like to try it out? Click here, follow the prompts, and you’ll get a personalised KiwiSaver portfolio in minutes.

Retirement may be far off, but it will happen

While it’s too early for comprehensive retirement planning, being young means you’re in the best position to plant the seeds of your financial future and watch them grow. Time is your number-one ally, and by setting up your KiwiSaver plan for maximum growth, you can make the most of this advantage.

Use our digital advice tool to run your numbers in a few minutes, or call the team at Kōura on 0800 527 547.

References:

1. Morningstar Australia – KiwiSaver Survey | March Quarter 2020

2. Morningstar Australia – KiwiSaver Survey | March Quarter 2023

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.