KiwiSaver through life: Your 40s

Table of Contents

KiwiSaver through life: Your 40s

21 Aug 2023

KiwiSaver through life: Your 40s

Are you in your 40s? You may not be feeling it yet, but retirement is getting closer than you think. And here’s a handy guide to make the most of your KiwiSaver plan.

Everyone’s different, but generally, in your 40s life usually settles down a bit. You’re mid-career and maybe reaching your peak earning years. If you have children, they might be older now, plus the mortgage is possibly becoming more manageable.

Amidst all this, something should probably be gaining more of your attention – your retirement planning. So, let’s dive into some key steps to take.

1. Time to ramp up retirement planning.

With life’s everyday distractions, it can be easy to lose sight of your long-term goals. But your 40s are a time to put those goals in sharp focus.

You’re likely earning more now than in your earlier years, and your commitments – like the mortgage or family expenses – may not be as overwhelming. This breathing space in your financial life makes your 40s an ideal time to make your KiwiSaver plan work harder for you.

Think about your goals and take a closer look at your plans: are you on track to achieve the retirement lifestyle you’re envisioning? And how much do you need to save? As we outlined in a previous article, it’s a good idea to aim to replace between 70% and 100% of your weekly pre-retirement income. If you don’t want to dust off your calculator, our digital advice tool can help you understand how much you’re on track to save, and the corresponding weekly income you could get.

You might find there’s a gap to fill, in which case increasing your contributions can be an option (if your budget allows it, of course). A small increase may not seem much, but the magical powers of compounding returns make every dollar count. This is because the returns you earn are reinvested and earn returns of their own – allowing your money to grow faster the longer it stays invested.

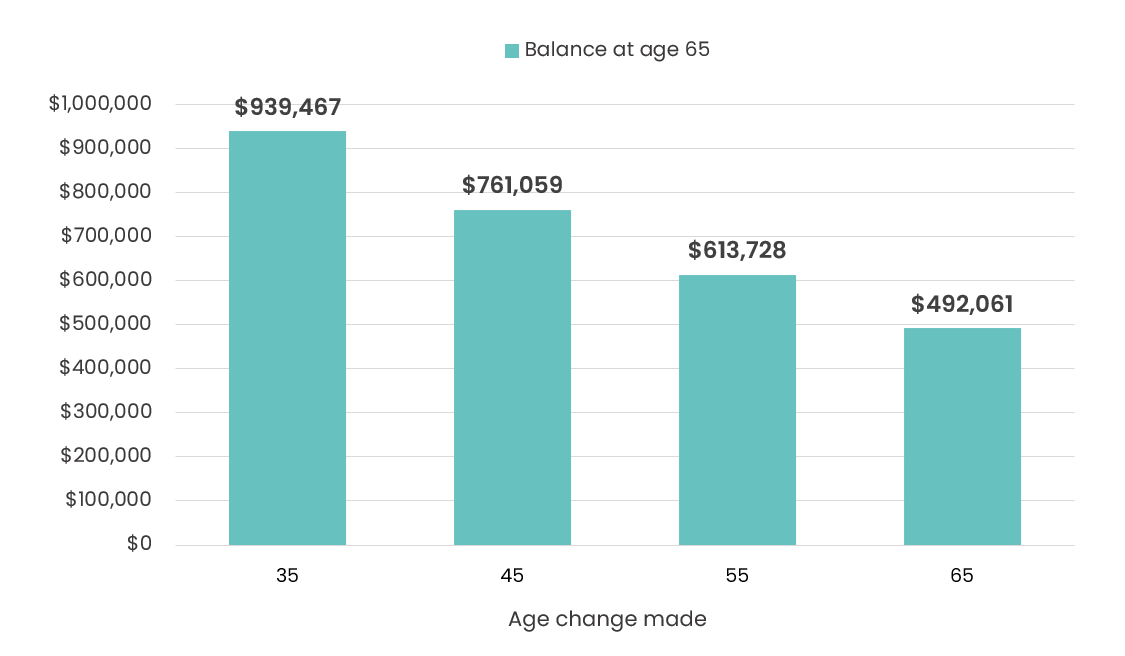

To illustrate the difference that boosting contributions can make, here’s Jane, a 35-year-old earning $80,000 and contributing 3%. Here’s what her retirement savings could look like if she selected the 8% rate at different ages.

Key Assumptions:

-

Assumes KiwiSaver invested in a growth fund earning 5.5% per annum, this may be too aggressive for someone approaching retirement, but is used for comparison purposes.

-

Assumes 35 year has a starting salary of 80,000 and this salary grows at 3.5% per annum in line with FMA assumptions, contributing 3% and employer matching at 3%.

-

All numbers have been shown as nominal numbers, and therefore not adjusted for inflation.

2. Stay aggressive, stay the course.

Choosing the right type of fund for your retirement goals is crucial. You need to consider both your attitude to risk (how you feel about seeing your KiwiSaver balance drop in the short term) and your investment horizon.

This brings us to you and your 40s. You’re still a couple of decades away from retirement, which means it’s probably too early to de-risk your portfolio. If your attitude to risk allows it, a higher-risk fund (growth or aggressive) remains a good option.

Let’s be clear: investing in these types of funds is not about being reckless. It’s about understanding that, at this stage of life, you have time to ride out any market storms that come your way. If your attitude to risk can withstand short-term fluctuations in value, growth and aggressive funds are likely to provide higher long-term returns.

Of course, in times of market volatility, it can be easy to fall victim to market noise and run for cover. Maybe you’re starting to be concerned about your future retirement savings, and you’re thinking that moving to a more conservative fund will help you protect your money. But as we said, you still have time: time to grow your funds significantly, and time to weather the storm.

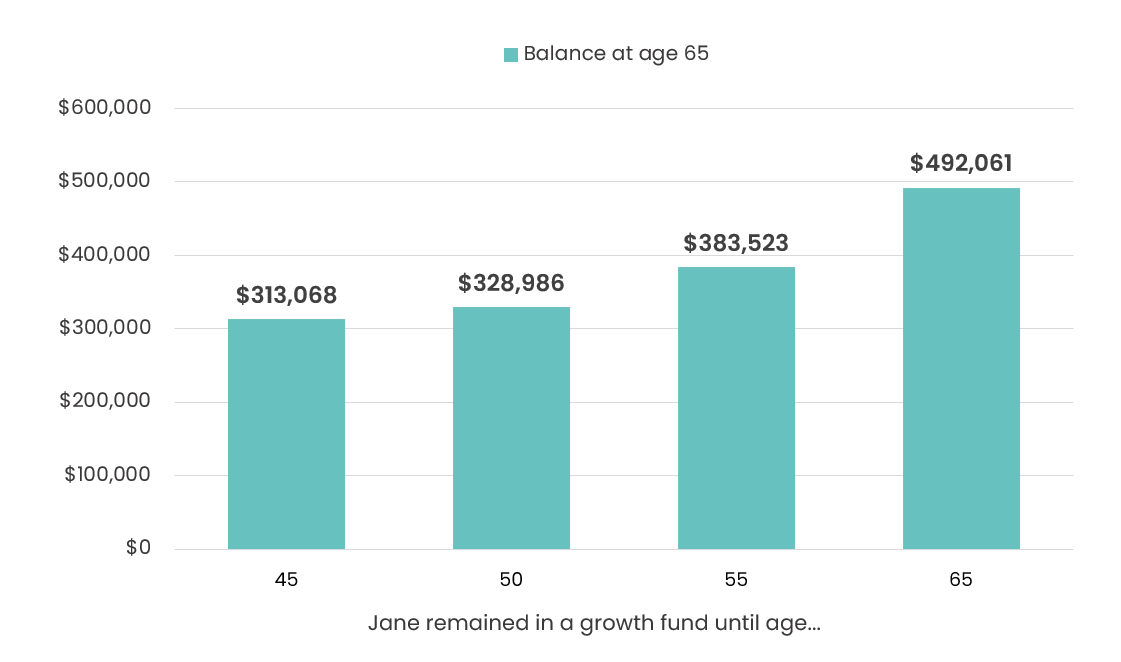

Now, let’s return to Jane for a second. Here’s the difference in potential retirement savings if she switched to conservative in her 40s, or stayed in growth for a bit longer.

Key Assumptions:

-

Assumes KiwiSaver invested in a growth fund earning 5.5% per annum, this may be too aggressive for someone approaching retirement, but is used for comparison purposes.

-

Conserative fund assumed to have 2.5% annual return

-

Assumes 35 year has a starting salary of 80,000 and this salary grows at 3.5% per annum in line with FMA assumptions, contributing 3% and employer matching at 3%. Starting KiwiSaver balance of $0 at age 35.

-

All numbers have been shown as nominal numbers, and therefore not adjusted for inflation.

So, instead of de-risking, try this instead:

-

Have a personalised KiwiSaver plan, based on your goals and risk profile – like the one you can create with our digital advice tool.

-

Stay the course and keep your eyes on the horizon, so you can navigate through choppy waters and come out stronger on the other side.

3. Make active choices for your future.

Being in your 40s means you’re halfway through your journey to retirement. And you have the power to change the outcome, if you take charge and set your course.

Here are some key steps to take:

-

Actively choose your KiwiSaver fund

As we said before, being invested in the right type of KiwiSaver fund can mean a difference of thousands of dollars. And if you don’t remember ever choosing your KiwiSaver fund or provider – now is the time to take action.

You might have been invested in a default fund since you first joined the scheme. This type of fund was always intended as a temporary solution, a safe place for your savings until you found a more appropriate fund for your needs.

Why does it matter? Well, in terms of risk, default funds are usually ‘balanced’, not too risky but not too conservative either. And this may not be aggressive enough to give you a comfortable lifestyle. So, why not choose a fund that’s aligned with you?

-

Choose your contribution rate

Next, consider your contribution rate. Many people don’t realise that contributing the minimum amount of 3% is unlikely to give them enough to retire on.

The solution? Make sure the rate you choose is in line with your budget limits and high enough to achieve your goals. If you’re not quite sure which contribution rate to choose, you read our comprehensive guide ‘How much do I need to save for retirement?’, or use your digital advice tool to run your numbers.

-

Use KiwiSaver to your advantage

Lastly, remember the benefits that KiwiSaver provides, such as employer contributions and annual Government contributions.

If you’re employed, your employer will contribute a minimum of 3% to your KiwiSaver balance. Over time, this can add up to a considerable amount, and it’s all extra money that’s helping you grow your savings.

Regardless of whether you’re employed or not, if you’re aged between 18 and 65 and contributing to your KiwiSaver plan, you also receive the annual Government contribution. For every dollar you contribute in the year between 1 July and the following 30 June, the Government adds an extra 50 cents – up to a maximum of $521.43 a year.

These additional boosts to your KiwiSaver balance can significantly amplify the growth of your savings. And your 40s are the time to take advantage of every financial growth opportunity available to you.

4. Keep an eye on the fees you’re paying.

Just like any investment fund manager, KiwiSaver providers charge fees to manage your money. It’s a fact of life. But that doesn’t mean you should ignore fees. They may seem small, but over time, they can add up and take a significant bite out of your retirement savings.

Just as you’re mindful of where and how you invest your money, it’s good to be equally aware of how much you’re paying in fees. Be proactive and ensure that you’re not paying more than you need to: it’s your hard-earned money, after all! You can read about our fees here.

5. Review your KiwiSaver plan regularly.

Life is a journey and your financial needs, family situation, and goals may evolve over time. So, it’s essential to reassess your KiwiSaver plan regularly to ensure it keeps pace with you.

This includes reviewing your KiwiSaver fund, contribution rate, and overall plan. If your situation changes significantly – for example, you have a major pay raise, a child moving to university, or a shift in your financial goals – it might be time to adjust your plan.

And you don’t have to do this alone. Financial advisers, tools and resources are available to guide you through the process and help you make informed decisions.

Here at Kōura, we have designed an innovative digital advice tool to provide personalised KiwiSaver advice based on your circumstances and goals – just like a human adviser, but with the convenience of being available anytime, anywhere. Like to try it out? Click here, follow the prompts, and you’ll get a personalised KiwiSaver portfolio in minutes.

Time is still on your side, but it’s moving fast!

There’s no time like the present to secure your future. While retirement may still feel like ages away, it’s closer than you think. So, ensuring that your KiwiSaver plan is working at maximum efficiency is all-the-more crucial.

Like to see what that future could look like? Use our digital advice tool to crunch your numbers in a few quick steps. Or give the team at Kōura a call at 0800 527 547.

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.