The Kōura market wrap for August 2023

Table of Contents

The Kōura market wrap for August 2023

6 Sep 2023

Hard landing, soft landing or no landing? August had it all.

The Kōura market wrap for August 2023

August was a volatile month, with investors going through the full spectrum of emotions (whilst enjoying their summer breaks in the Hamptons or on the French Riviera!). Risk antennae are on high alert following a very strong market performance, which has seen global markets trading significantly higher than even the most bullish forecasts made at the start of the year.

Early in the month, very strong economic data released in the US, confirmed that the US economy is growing at a much higher rate than expected – and that pushed interest rates higher.

On this note, markets have finally come to the realisation that interest rates will stay higher for longer, which is also the reason that banks continue to increase mortgage rates. This narrative prevailed for the first three weeks of the August, driving markets 6% lower.

But this quickly changed in the last week as investors realised that companies and consumers can withstand higher interest rates, and a strong economy is actually good news. This allowed markets to recover a significant portion of their gains to end the month only 1.7% lower.

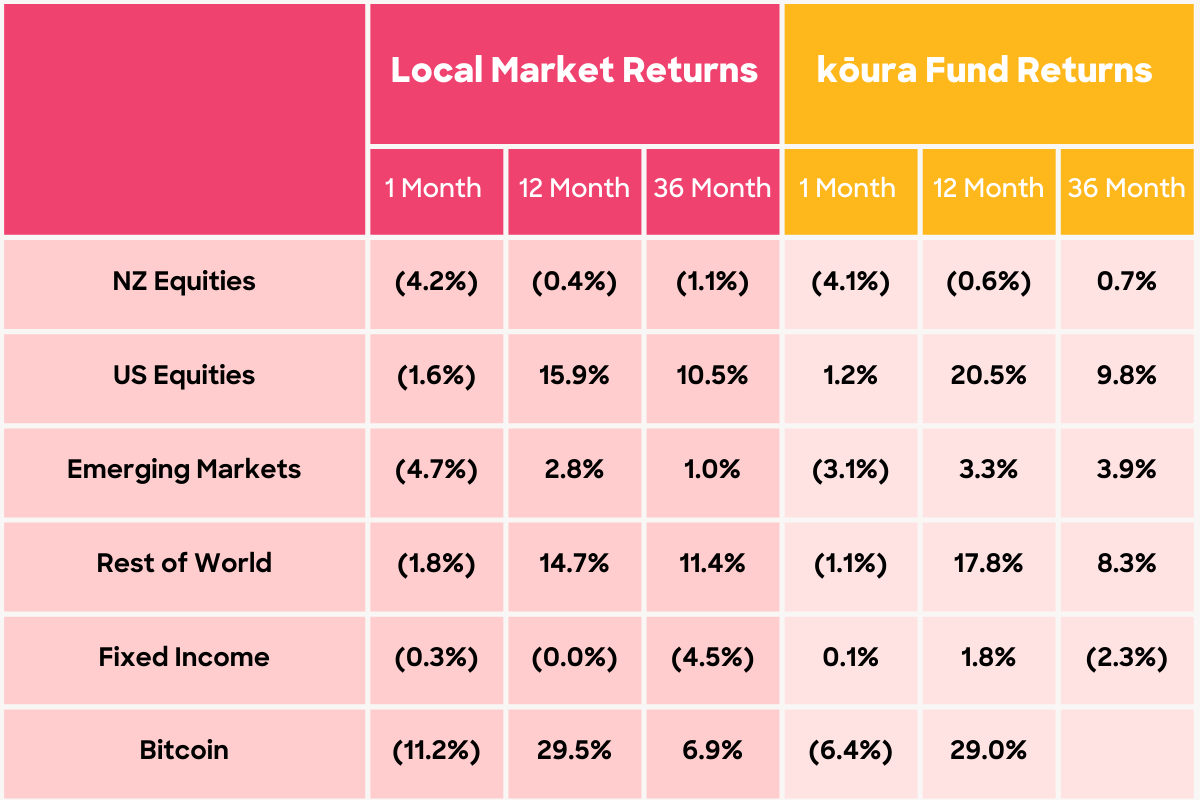

Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ.

Local market returns use the relevant market indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin.

To give you a bit more context, below is a summary of some of the things that we have been thinking about over the past month:

1. Why have markets not crashed? Can companies actually withstand higher interest rates?

Yes, it’s increasingly clear that companies can withstand interest rates. Why is that? To put it in context, borrowing costs have now returned to where they were in the mid 2000s, just before the Global Financial Crisis. This is due to two things: on the one hand, companies locked in lower interest rates over the past few years; on the other, consumers continue to spend, which means corporate earnings and margins remain extremely strong.

During 2021 and 2022, companies issued a significant amount of debt to ensure they locked in the ultra-low interest rates for as long as they could. So, just like households, many companies are yet to feel the full pain of higher interest rates on their earnings.

The one big question mark on investors' minds is what happens to valuations. The US equity market is currently trading on a P/E multiple of 21x 2023 earnings, compared to a long-term average of 14.8x. That means you are willing to pay $21 for every dollar of earnings the market generates. If interest rates continue to stay higher for longer, the P/E ratio will need to fall to ensure investors are sufficiently rewarded for the risk they are being asked to take.

2. Why do mortgage rates keep going up when the OCR stays flat?

Frustratingly for many mortgage holders, the RBNZ have not changed interest rates over the past six-eight weeks, yet fixed-rate mortgages continue to rise.

Up until very recently, banks had expected interest rates to start falling in the last quarter of 2023. Now that banks expect interest rates to stay higher for longer, however, their new pricing will need to consider these higher interest rates.

Where to from here? The market currently expects interest rates to start falling in the 3rd quarter of 2024. If that assumption proves wrong and interest rates need to stay higher for longer, then we can expect interest rates to rise further.

3. What is happening in China and why is the Government not stepping in to solve the problems?

China continues to go from bad to worse, and the few snippets of economic data that are released seem to show the economy getting worse rather than improving. Unlike the rest of the world, prices and wages are falling (deflation), reflecting the difficulties in getting the economy back on track.

The real estate crisis continues to drag on with property prices falling and yet another large developer (Country Garden Holdings) on the cusp of default. The slowdown is particularly impacting young people who are finding it harder to find jobs, with reportedly one in five young people currently out of work.

So, what’s happening? In short, the crisis is a combination of US sanctions and the crackdown on leverage and real estate, which has driven so much of the previous cycles. On top of it, being largely fearful of the current political climate, foreign companies are moving manufacturing home (onshoring) or to other markets that are viewed as more politically friendly with the US. For example, Apple and Tesla have recently announced production in India. This realignment of global supply chains is contributing to inflation in the rest of the world, and causing a world of pain in China.

So far, the Chinese Government has refused to step in and help. Over the past few weeks, interest rates have been lowered and lending conditions have improved, but we are yet to see any of the large central Government stimulus measures that have historically accompanied economic slowdowns.

4. Is New Zealand at risk from a China slowdown?

Short answer: most definitely yes. China is New Zealand’s largest trading partner, taking 24% of our total exports. What’s more, our second-largest trading partner, Australia, exports 33% of their total exports to China.

Weaker consumers in China will mean weaker demand for all our commodity exports and a slower recovery for tourism. Milk prices have already fallen significantly with many expecting them to fall further, and while less public, we are also seeing similar moves in meat commodities and log exports.

5. Why is the New Zealand sharemarket continuing to underperform?

The New Zealand sharemarket has been one of the worst global performers over the past three years, having delivered a 1.6% per annum loss compared to a 16% per annum return for global markets. The past 12 months have seen much of the same: our sharemarket continued to drift sideways whilst other markets have had a very strong recovery.

Unfortunately, the New Zealand market is a small market largely made up of property and infrastructure companies (c. 65% exposure), two sectors that are very sensitive to interest rates. Historically, New Zealand investors have rewarded companies for delivering safe stable dividends rather than striving for growth. In the current environment, retail investors in particular would prefer to take a 6-7% bond coupon rather than earn a 2-3% dividend yield on a stock with limited growth prospects.

6. What’s happening in the crypto market?

Crypto prices fell sharply in August. After reaching a peak of US$31,000 in mid-July, the price of Bitcoin has subsequently fallen below US$26,000.

This is due to both regulatory and sentiment reasons. In July, BlackRock and Fidelity filed applications to launch a Bitcoin spot ETF on the Nasdaq. This triggered a wave of excitement, thinking it would open up crypto currencies to a whole new world of investors. However, the SEC delayed the decision yet again and it appears they may even be looking to decline the application.

There is no doubt that crypto trades on sentiment: when investors get nervous, Bitcoin is often punished. This is what happened here: over the past four-to-six weeks, markets have become nervous and are not sure on where the market goes next. Increasingly, it appears that Bitcoin is becoming a leveraged play on risk sentiment.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.