The kōura market wrap | July 2022

The kōura market wrap | July 2022

4 Aug 2022

Is this the start of the recovery?

With investors starting to anticipate a ‘policy pivot’ from the US Federal Reserve, markets soared in the month of July. The big question – is this the start of the recovery or a bear market bounce?

As we noted in the past, markets are currently driven by interest rates and the fight against inflation, increasingly, there is a view that the fight might be closer to its end than the start.

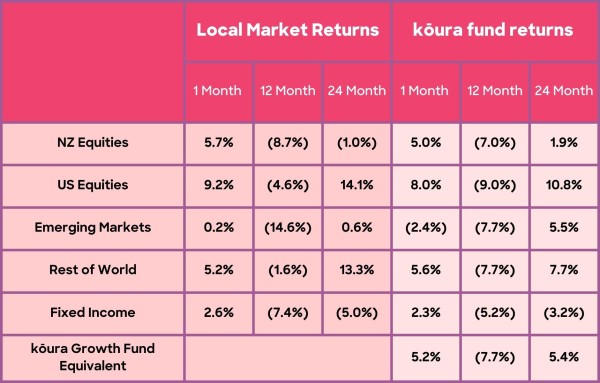

Looking at markets’ performance, the S&P500 had its best month in over two years and the tech-heavy Nasdaq index had its best month since the post-Covid rebound of April 2020. Even European markets were up over 6%, despite the prospect of Russian gas being turned off and the European Central Bank (ECB) starting its first round of rate hiking in over a decade.

Now, the big question circling around in everyone’s mind is whether these results signal the start of the recovery or just a bear market bounce.

Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 36.6%, Emerging Markets 7.8%, Rest of World Equities 15.6%, Fixed Income 20%. The Kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the Kōura funds invest in. Past performance does not equal future performance.

What did the Federal Reserve actually say?

On Wednesday 27 July, the US Federal Reserve moved to raise interest rates by 0.75%, taking their target rate to 2.25 – 2.5%. It was the second 0.75% increase in a row.

Markets rallied following the announcement, with the tech-heavy Nasdaq lifting more than 4% over the day. And while the actual interest rate move was significant – it was expected, what really mattered was the unexpectedly strong commentary from US Federal Reserve Chair Jerome Powell.

In short, Powell highlighted that, as economic growth slows, it will be appropriate to slow the pace of interest rate increases – implying that the central bank has already done the bulk of what is needed to combat inflation. Powell also commented that he saw 2.5% as a neutral interest rate, which is a level of the cash rate when the economy is in equilibrium. In other words, the ‘neutral rate’ is meant to neither enable growth nor slow the economy.

These comments have been interpreted as meaning the sharp rises in interest rates might be close to an end and that the fight against inflation may be close to an end.

Plus, more good news came on Friday 29 July, with data confirming that the US was actually in a technical recession – which again gives investors greater confidence that interest rate increases may soon stop.

If the US (and potentially others) are in recession, what does it mean?

On Friday 29 July, it was announced that US GDP shrank by 0.9% at an annualised rate, the second consecutive fall. Technically, this signals that the US economy is in a mild recession.

To be clear, the US is unlikely to be the only country in this boat: while data is yet to confirm it, we would not be surprised if many parts of Europe and New Zealand are also in recession. And it may not all be bad news.

In a normal recession, we see reduced demand for goods, which in turn drives unemployment and significant falls in corporate earnings – which ultimately impacts share prices. But at this stage, this recession is slightly different from others, having been caused by central banks and sky-high commodity prices rather than financial or other reasons.

Importantly, unemployment has remained strong and labour shortages persist globally: a short slowdown might deliver the inflation relief that central banks around the world have been looking for.

So, does that mean recession is actually good news? Well, maybe, as long as it is short and shallow, and does not flow through to the labour market.

What happens if Russia turns off its supply of gas into Europe?

Another critical piece of news over the month was whether Russia would allow gas supplies to recommence through Nord Stream 1, the primary pipeline supplying gas from Russia through to Germany and the rest of Europe.

Without heating requirements, Europeans typically use significantly less gas during summer, so the warm season is a critical period for building up gas supplies for the winter months. If supply is cut off now, it will become impossible to move sufficient gas into European storage facilities to use through winter.

This scenario would require significant reductions in European energy usage, impacting on economic growth. Economists have estimated that up to 3.5% of European GDP could be wiped off if gas supplies are interrupted, with Germany likely to be the most impacted.

To help prepare for a gas shut down, all EU countries have agreed to reduce their gas usage by 15%. However, for the time being markets are discounting a scenario of gas being turned off. They rather see it as a negotiating ploy by Russian president Vladimir Putin to get sanctions relieved, or even have their Nord Stream 2 gas pipeline certified by the European Union.

What is happening in China?

The ‘Red Dragon’ continues to go through a world of economic pain, with its flagship market index falling almost 3% in July while the rest of the globe gained ground. There are a number of issues affecting the Chinese economy, including:

-

A weak property market: The housing market continues to slide. Prices keep dropping and property sales are expected to fall by up to 30% this year, compared to 2021. Exacerbating this issue, developers are struggling to complete projects due to financing issues as well as Covid-related and supply delays, meaning buyers are trying to pull out of previously committed purchases;

-

A vulnerable banking system: There are increasing concerns that the banking system may not be able to withstand a full-blown property crisis, with 35% of assets currently invested in residential mortgages and a significantly higher share of credit extended to property development companies;

-

Covid-19: Ongoing Covid restrictions are hampering growth due to lockdowns and significant restrictions on travel and socialising; and finally,

-

The tech crackdown: Many had thought it was over, but the tech crackdown continues to rear its head with new regulatory pressure put on Ant Group.

To top it all, given the political risks and difficulty in getting real data on what is going on, many American investors are now calling China ‘uninvestable’. And Nancy Pelosi’s trip to Taiwan will only make things more interesting from a geopolitical perspective (think fireworks!).

Why didn’t we see the bounce in the New Zealand market?

The New Zealand market rose only 5.7% during the month, well below the global market return of 8% and the US market return of 9.2%. Two things are important to note here:

-

This performance has brought the New Zealand market in line with the rest of the world’s year-to-date performance, with a loss of 11.5%.

-

New Zealand is slightly further ahead in the economic cycle than our peers internationally, and it appears that concerns around an economic slowdown are stronger here than overseas.

What is happening in the crypto markets?

Lastly, here’s an update from the crypto world. The crypto market rallied in the month, with Bitcoin recovery 23% up to almost $24,000 and Ether lifting 67% in the month. As risk appetite returns to the market and we start to see the end of the ‘market liquidations’, the prospects for crypto currencies are improving.

Over the past few months, we have seen a number of crypto exchanges and investment funds liquidated due to excess leverage. This has removed many retail investors from the crypto markets, while also resulting in a significant amount of crypto currency placed on the market as lenders have tried to recoup losses. Now, with that trend coming to a close, we are hopefully moving back toward a more normal investment environment.