The Kōura market wrap for November

The Kōura market wrap for November

7 Dec 2022

Bear market rally or true recovery?

After a positive October, November was another great month in the markets. But is it going to last?

As we have said many times before, investment markets are always looking for good news to move higher and get money back to work. November confirmed a lot of the hypotheses that had been built in October with positive news across multiple fronts. Global markets (as measured by the global MSCI index) were up over 5% taking their total return to almost 9% over the past two months from their lows in late September.

Unfortunately for New Zealand investors, returns were somewhat muted by the strengthening of the NZ Dollar, which diluted their profits. Over the past few months, the New Zealand dollar has bounced from a low of 56c per USD up to almost 63c per USD.

The question is, can this strength in the markets continue? You can argue that we are seeing a market recovery before the market has even glimpsed the recession, which might be a little horse-before-cart. Or the recession might not ever turn up. The market is clearly banking on a soft landing, it will be interesting to see whether this is the permanent view, or simply the November view.

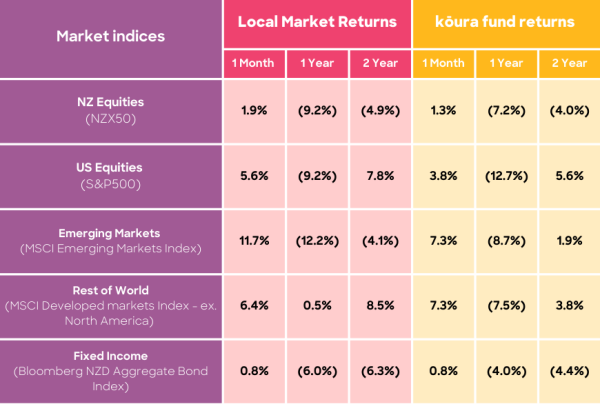

Here’s a summary of the returns we’ve seen in the past month.

Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 36.6%, Emerging Markets 7.8%, Rest of World Equities 15.6%, Fixed Income 20%. The Kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the Kōura funds invest in. Kōura returns are net of tax. Past performance does not equal future performance.

Read on for an overview of the factors that influenced the market’s performance in November.

1. The US Federal Reserve confirmed that they would slow down interest rates hikes

After many weeks of speculation, on the very last day of November, markets finally got the confirmation they had been looking for. Chair of the US Federal Reserve, Jerome Powell said in a speech that they were “likely to slow the rate of federal funds rises”, effectively confirming that the next rate rise on 13 December will be 0.5% rather than the jumbo 0.75% rate rises that we have had for the past few months.

The market has interpreted this as a policy pivot confirming that we might be getting close to the end of the fight against inflation (we have said this before!). US markets jumped almost 5% on the day reflecting this positive news.

Interestingly, markets ignored other comments in the speech suggesting that this announcement reflected a slight tweak to policy rather than a full-blown pivot. To keep the bulls at bay, Powell also said that he did not anticipate rates falling any time soon (markets expect rates to start falling in late 2024), and that the final federal funds rate will need to be significantly higher than had been anticipated back in September.

We fear that markets might have gotten ahead of themselves here, we still have not seen any changes in the global labour market which is seen to be the key driver of inflation.

2. China’s zero-Covid policy might be coming to an end

Recent Covid outbreaks in China have emphasised just how difficult it will be to keep Covid out of the country hard lock downs no longer work and the economy can’t really handle the damage they cause. Covid infected people are being allowed to isolate at home and there appear to be softening of travel and crowd restrictions. These are all signals that that policy has shifted from ‘eradication’ to ‘flattening the curve’ (language that all New Zealanders should remember from the 2021 daily press conferences!).

Why now? There appears to be a broad recognition that the economy cannot withstand the continuation of zero- Covid. The policy has slowed economic growth, with only 3% GDP (Gross Domestic Product) growth so far this year – significantly lower than the 6% targeted and for the first time in many decades, Chinese citizens are starting to feel poorer rather than wealthier.

From a global economic perspective this is great news as hopefully China growth will restart just as the rest of the world enters its interest rate induced recession. As expected, Chinese markets reacted positively rising 10% in the month.

Meanwhile, Hong Kong has accelerated its reopening, easing limitations on large gatherings and making international travel easier. And as a result, the Hong Kong market was up 25% in the month.

3. Somehow, Europe appears as though it will avoid energy blackouts this winter

Gas storage levels remain in Europe and the Europeans are doing good at sharing gas and moving it to where it is needed. This is leading to politicians and economists taking the view that energy blackouts might be avoided (for this winter!).

This better than expected energy situation is thanks to one of the warmest Autumns on record and an abundance of gas available because of China’s ongoing zero-Covid policies. Shipments of LNG (Liquefied Natural Gas) have been diverted from China to Europe as China’s industrial world has slowed down.

If China’s reopening accelerates faster than forecast, it could have a profound impact on global energy markets as their demand for oil and gas will soar at a time when further restrictions on Russian supply are coming into play.

The big questions for Europe are what happens if the weather turns very cold, and how do they refill storage facilities next summer without the Russian supply.

4. Adrian Orr has positioned New Zealand as the leading light in the fight against inflation

The Reserve Bank of New Zealand (RBNZ) grabbed headlines in the month with one of the most hawkish policy announcements of all time. On 23 November, the RBNZ raised interest rates by 0.75%, which was not entirely unexpected. But the tone of the commentary surprised everyone. The RBNZ stated that they see interest rates rising significantly higher than previously anticipated and that they are now expecting a shallow but long recession from April 2023. This made it clear to everyone that the RBNZ now thought it imperative that they engineer a recession to get inflation under control.

This is a far more aggressive stance than any other central banks in the world are taking. In fact, most are taking a wait-and-see approach, wanting to see the impact of the higher interest rates before continuing the march higher. Only time will tell who is correct in their approach.

New Zealand is proud of its credentials as a leader in implementation of monetary policy, we were one of the first countries in the world to focus central banks entirely on inflation, and this announcement seems to be an attempt to rebuild the credibility that might have been lost over the past few years.

5. The crypto world was rocked by another failure

The crypto world was rocked by the failure of the world’s third-largest crypto exchange, FTX –further eroding the limited amount of trust that crypto currencies had amongst mainstream investors.

FTX’s Sam Bankman-Fried (SBF) had become the poster child of the crypto world in the USA, appearing before Congress and lavishing billions of dollars on marketing. It appears, though, FTX was a business that did not understand the core fundamentals of risk management or segregation of customer assets. The business was lending money (potentially customer funds) to staff and a related hedge fund. The business owes customers at least $3 billion, and receivers are currently working their way through to figure out exactly what happened.

What is clear from this debacle is that regulatory oversight is necessary for the crypto industry to survive. FTX was effectively running an extremely complex trading business with no systems, risk management or effective regulators – for the system to thrive and reach its full potential this will need to change.

Meanwhile, the price of Bitcoin fell over 20% on the news and was sitting around USD$16,500 from the pre-FTX high of $21,000. This has subsequently recovered to c. $17,500.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.