Kōura Market Wrap | February

Kōura Market Wrap | February

7 Mar 2024

What a year to be an investor

The last 12 months have been a spectacular time to be an investor. Looking at both the market and Kōura fund returns, it has been an incredibly special time. February was no different with global markets continuing their upward march putting on an extra 5%, the US and Japanese markets hit record highs and Bitcoin is getting closer and closer to its previous peak of $66k USD.

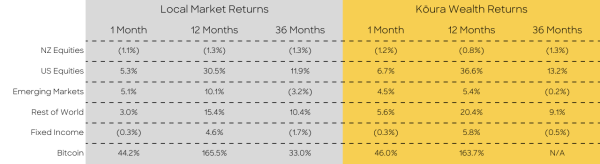

Source: Factset: Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ. Local market returns use the relevant markets indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin. Returns to February 29th, 2024.

Strong earnings results have driven companies back to record highs

February saw reporting season in the US come through and fair to say, results were far better than anticipated. 95% of companies have now reported Q4 earnings, and 73% of the companies beat earnings expectations reporting earnings growth of 4% on average. For the full year, earnings estimates have now been pushed up by 11%.

Two massive results announcements were Meta (Previously Facebook) and Nvidia, both of which set records for the biggest market cap gains in a single day - $197 billion and $227 respectively.

Nvidia continues to go from strength to strength with earnings and revenue growth surpassing expectations. Nvidia is now up 256% year-on-year but interestingly earnings and revenue growth have been even bigger. The big question on everyone’s minds is whether this is sustainable growth or not.

China had a strong month as markets reacted to government stimulus

Over the past 6 – 12 months, investors have become increasingly nervous about the potential for the Chinese economy and stock market. The market is down 20% over the past 12 months, compared to the rest of the world being up 25%.

The fall has been driven by an ugly combination of a declining population, falling property market, unpredictable Government, and geopolitical tensions that have made China uninvestable. The Goldman Sachs Wealth Management CIO has even gone as far as to publicly advise clients to stay away from China and avoid being tempted by the recent falls.

In February the Government finally stepped in, recognising that its legitimacy will be tested if it can no longer promise to improve the wealth and prosperity of its population. During the month, the Government instructed state-owned firms to start purchasing shares who spent almost NZ$100b propping up local share prices. In addition to the direct support, it has also reduced headline interest rates and allowed banks to hold lower levels of capital to support the beleaguered property market.

Who knows whether this is enough? Other measures such as bans on short selling and restrictions around short-term quantitative are likely to backfire as they merely reinforce foreign investors' fears of Government control in the markets.

All of this drove the Shanghai Composite up a very respectable 9.7% in the month, though it is still down 6.7% year to date reflecting the very poor January.

US economy is holding up better than expected, creating nervousness around interest rates

Economic data in the US continues to trend toward the upside resulting in a bit of nervousness around the timing and extent of interest rate cuts. Unemployment remains stubbornly low at 3.8%, GDP growth remains strong, and January’s monthly inflation data has come out higher than it had for previous months.

To make investors even more nervous Jerome Powell, (the US Reserve Bank Chair) come out with a 60-minute interview stating that while they have confidence, they will not need to raise rates again they need to see more evidence of a sustained reduction in inflation before they can start cutting interest rates. Shipping issues in both the Panama and Suez canals are unlikely to be good for inflation data.

Investors are increasingly uncertain on whether we will see interest rate cuts in 2024. Though it is important to remember employment and CPI data is backward looking and can often be some of the slowest data to react in the event of a downturn.

New Zealand interest rates journey have remained unpredictable with no one really having any idea on what is happening

ANZ economists managed to throw a cat among the pigeons in early March stating they thought the RBNZ may need a further two rate hikes to control inflation. It is hard to understand what the announcement was meant to achieve, they were well out of the market with the call, though it did make interest rate and foreign exchange markets a bit nervous. Short-term yields jumped because of the news.

Though on 28 February, RBNZ Governor Adrian Orr announced that he would hold interest rates flat and gave investors' confidence that we are winning the fight on inflation. Yields quickly dropped following the announcement and banks have even gone so far as dropping (very slightly) their mortgage rates. Hopefully we will see more mortgage relief shortly.

Crypto went sky high with Bitcoin approaching its record highs

Bitcoin breached the US$60,000 mark for the first time in almost 2 years. Excitement over the ETF’s has driven more net buying with net inflows now exceeding $7 billion into these ETF’s.

According to Bloomberg margin lending and derivative interest is at all-time highs which can be seen as a risk factor. With the halving approaching on 1 April, it is unclear how high we go from here, are firmly back in bull territory or is this a short-term run.

Disclaimers

Cryptocurrencies are highly volatile assets and not suitable for everyone. If this fund had existed over a 2–3-year history, the performance would have been negative due to the inherent volatility of cryptocurrencies. This underscores the importance of understanding that cryptocurrencies still have an uncertain future and are therefore not appropriate for all KiwiSaver members. Before investing part of your KiwiSaver balance in cryptocurrency, it is crucial that you have a clear understanding of all the associated risks: https://shorturl.at/irERY

Past performance is not a guarantee of future returns.

Members can only allocate a maximum of 10% of their portfolio to our Carbon Neutral Cryptocurrency Fund.

Kōura Wealth is the issuer of the koura KiwiSaver Scheme. View our PDS at kourawealth.co.nz/documents

The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.