June Market Wrap: The freight train appears impossible to stop!

Table of Contents

June Market Wrap: The freight train appears impossible to stop!

4 Jul 2024

Overview

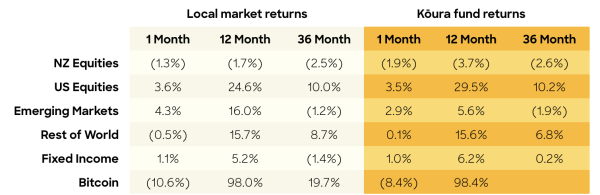

Markets keep heading higher rising 3% in June. The US stock market has hit 35 records so far in 2024, an amazing feat considering most market participants expected 2024 to be a difficult year. The market continues to be driven higher by AI and technology enthusiasm rather than anything real. The constant march upwards continues to surprise most market followers, though anyone that has tried to bet against the rally continues to be badly burnt.

Where to next given markets are already up 14% this year, can this continue?

There is no doubt markets are on a roll and keep on marching higher and higher, though how sustainable is this. The growth this year has been driven entirely by improved valuation metrics due to excitement about AI and a more productive future. The average price / earnings rate (measures how much investors are willing to pay for each dollar a company earns) has grown to 21x over the past 6 months, it started the year at 19x. Earnings estimates have remained flat, so companies are basically delivering as expected (and priced).

Over the past few weeks we have seen a number of Investment Banks have put out their year end outlooks. Most strategists are predicting flat markets for the rest of the year, they are trying to triangulate between three individual factors:

- Markets are currently values at a significant premium to their long term averages

- Economic growth is likely to slow in the second half of the year which is likely to impact company earnings

- Interest rates should fall which should help support higher valuations

- AI could drive an economic wide productivity boom to drive higher long term earnings

Most importantly though, it appears strategists would rather stay on the fence right now given they have been consistently wrong over the past 3 years.

Do the political risks change anything

The last week has definitely been an interesting ride in the markets.

We saw the disastrous Biden / Trump debate which has raised the prospect of the Republicans completing a clean sweep in November. The Trump economic programme is pretty scary, lower immigration (this will push up wages and inflation), tariffs on all imports (higher inflation), lower taxes (bigger deficits) and more military spending (bigger deficits). At the moment a Trump world will look like higher inflation and higher deficits.

In France, we have seen the far right surge in the elections over the weekend. They are proposing lowering the pension age, limiting immigration and some form of soft exit from the European Union. Understandably markets were petrified and fell sharply off the back of this news.

Rather than react to the headlines though it is critical that we take perspective. Politicians rarely implement the extreme policies that they talk about once elected, and markets (and media) love to react to uncertainties (which these clearly are).

Looking back to 2016, the first Trump presidency ended up being great for markets due to the pro business policies and tax cuts. And looking to 2023, Italy voted in a far right Government and most agree that the policies have been extremely stable ever since.

Key is to make sure that you don’t let the headlines scare you and remain the course. There are enough checks and balances in the system to make sure outcomes are not too extreme, Brexit being the only exception to this.

NZ is probably looking at interest rate cuts sooner than expected

Here in New Zealand Q1 GDP was announced in late June (only 3 months after the end of the quarter!) We officially exited recession, though that was only due to the ongoing surge in migration.

The release confirmed that our GDP per capita continues to fall, over the past 18 months GDP per capita has fallen 4.3%, the worst period in New Zealand economic history since July 1991 (after the austerity budget to end all austerity budgets). This shows that the New Zealand economy is far weaker than anticipated. If immigration drops off as a result of reduced construction and infrastructure projects then our overall GDP numbers will start to look pretty sick.

Retail sales continue to fall faster than anyone had anticipated and business confidence is plummeting. It will be hard for the Reserve Bank not to look through these numbers and they will have to think very hard about whether they want to protect the economy or focus on inflation. If they want to protect the economy they should cut interest rates sooner.

The biggest unknown of course is the impact of the tax cuts that come into effect on 31 July. The Reserve Bank won’t say this, but they will want to wait until they understand the impact of those tax cuts before making any moves on the OCR.

My prediction is for an October cut, sensibility suggests we will need to move faster than anyone would like as it is about to get way too hard for every day people.

Crypto had a soft market with demand dropping away from the ETF

Demand has dropped off from the Bitcoin ETF’s, during the month net inflows were largely flat and that meant that the crypto price fell 11% in the month down to $60k. The big unknown is whether this is because those that were waiting for the ETF’s have now made their purchases and there is no more demand or whether people are starting to worry about the broader environment and looking to unload risk assets. A key metric to watch will be whether the ETF’s start to experience outflows.