Kōura Market Wrap | November

Table of Contents

Kōura Market Wrap | November

7 Dec 2023

November was one of the best months in the markets for an extraordinarily long time. For a diversified investor, it was the strongest month since December 2008 with both bonds and equities rising in sync.

For the equity markets alone, global markets were up 8.1%, making it the 6th best performance month since December 2021 and the best month since November 2020. The weakening economic data spurred on the soft-landing narrative - that inflation is under control and interest rates will start to fall in the first half of 2024.

It appears we are back to the party with all risk assets rallying and we have even seen a return of the meme stocks with Safety Shot joining the GameStop party (which has rallied 20% since the start of November).

Bitcoin also spiked; on December 3rd it was hovering just under $40,000. On December 5th, Bitcoin had surged through the $42,000 level, increasing year-to-date gains to 154%.

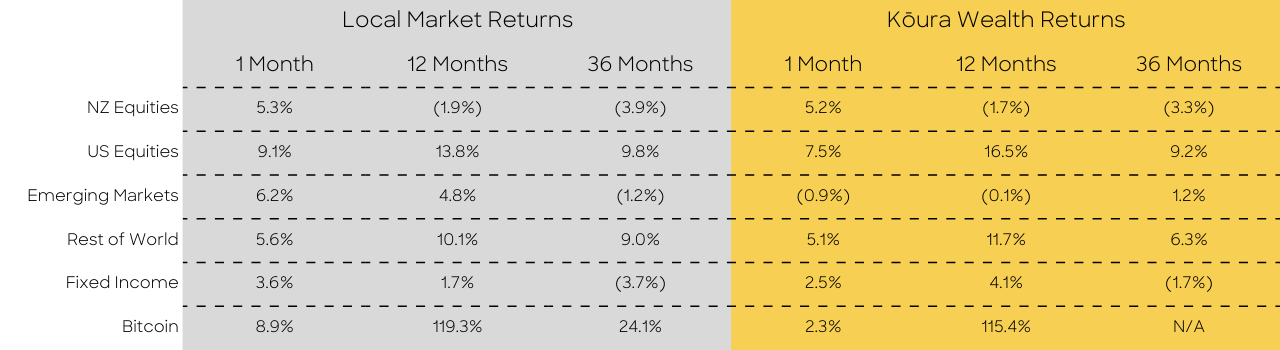

Source: Factset: Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ. Local market returns use the relevant markets indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin.

1. What drove the sudden shift in sentiment

Interest rates fell by c.0.5% through the month as investors started to believe that rates have peaked, and that interest rates will start to fall in Q2 or Q3 2024. During the month, we saw weakness in employment data and a drop in manufacturing sentiment (how companies feel about the world) which has led markets to believe that a soft landing is coming.

Pleasingly, the weaker economic data does not yet seem to be showing up in growth numbers, with the US and European economies continuing to show strong growth, thereby confounding expectations.

The question is: how long can this continue? We are starting to see signs of increased stress at the consumer level with credit cards and debt levels rising and arrears. We might finally be starting to see the long and variable impacts of monetary policy which have been so widely talked about for an exceptionally long time.

2. Interest rates are falling, what does that mean for mortgage rates

Interest rates have fallen by 0.5% across the board and that means that mortgage rates should start to fall soon as well. While cuts in the OCR (Official Cash Rate) might be a long way off, mortgage rates should fall sooner. Fixed term mortgage rates are priced based on the expectation of what will happen with mortgage rates over the time period of the mortgage, not what is happening today.

Therefore, as we are increasingly confident that a cut in the OCR will happen sooner rather than later, mortgage rates should start to fall.

Our prediction is that mortgage rates will start to fall in the early parts of 2024. This could cause a few headaches for the RBNZ (Reserve Bank of New Zealand), as they will not want to see any loosening of financial conditions until they are confident that inflation is well and truly beaten.

3. Why is Adrian Orr still talking tough

On 29 November, Adrian Orr came out stating that interest rates needed to stay higher for longer and that he might need to raise interest rates further in the new year. This surprised investors who were confident that the next move on interest rates would be down and that could be as early as Q2 2024. Interest rates shot up following the statement, as predictions for falling interest rates were further delayed and pushed out.

In the 1970’s inflation came in two separate bursts, the early 1970’s and then again in the later half. In 1972, economists and markets believed that inflation had been beaten and therefore eased up on monetary conditions. This relaxation of monetary conditions was seen to be a big driver of the second longer and more painful inflation push.

The RBNZ are fearful that the recent falls in interest rates will mean that mortgage rates also start to fall. This will ease monetary conditions and result in people increasing their discretionary spending. Combining lower interest rates with tax cuts could be the inflationary boost that pushes the next wave of inflation.

4. New Zealand dollar was up over 6% in the month against the USD, what happened?

The New Zealand dollar reversed recent declines and hit nearly 62c for the first time since July. This 6% growth was driven by a combination of US dollar weakness, higher NZ interest rates, and improved risk in sentiment here in New Zealand.

As economic data in the US has weakened, interest rates have fallen which has driven down the exchange rates. Following the 29 November RBNZ policy announcements, we had the complete opposite here in New Zealand with interest rates rising strengthening the NZD against all our peers. And finally, the NZD is seen by many to be a high-risk speculative asset, when risk assets do well (which they clearly are doing now) then the NZD will often do well too.

5. Bitcoin is over $40,000, where does it stop?

Bitcoin continues to surge and has pushed through the $42,000 mark. This recent surge has been driven by a combination of ETF (Exchange Traded Fund) chatter and also clarity around what will happen with Binance. With a settlement now agreed with the US Department of Justice, we now know that the largest exchange will continue to operate and will be able to offer services to US clients.

The reason for the spikes in prices also comes back to liquidity. Glassnode (a crypto analysis company) estimates that less than 30% of the Bitcoin market supply is actively traded ($245m equivalent), with the rest sitting in long term holders' wallets. This means it does not need a massive amount of demand to push prices up sharply. The converse of this is that when demand drops, we also see some very sharp falls.

It will be interesting to see where we go from here.

Conclusions

We are in risk sentiment now. Investors are picking a soft landing with inflation falling, interest rates falling, the global economy escaping recession and improved productivity resulting from AI to usher in a new golden age. It feels like a lot and like a Goldilocks scenario.

The one thing that the last few years have taught us is that economies are extremely resilient and have continued to adjust and perform despite significant challenges. While markets do appear to be pricing in the upside right now, you would be very brave to bet against the markets.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.