Kōura Market Wrap | October 2023

Kōura Market Wrap | October 2023

9 Nov 2023

October was another tough month in the markets with strong economic data driving interest rates higher around the world, which resulted in stock markets falling. Global markets fell a further 3% in the month, adding to the September losses meaning that markets finished the quarter down 6.5%. At times like this it can be tough being an investor, there appears to be nowhere to hide with rising interest rates causing both bonds and equities to fall.

The only place that continues to perform well is Bitcoin, where excitement about the prospects of a Bitcoin spot ETF (read more about that below) continues to push the price higher.

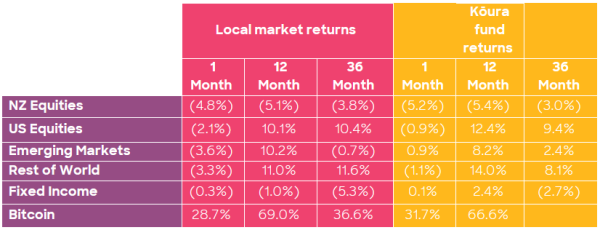

Source: Factset

Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ. Local market returns use the relevant markets indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin.

So, what have we been thinking about in the month?

1. Interest rates, and more interest rates

Interest rates dominated the month with yields in the US reaching levels that have not been seen since 2007. Economic data continues to show a strong consumer that wants to spend money meaning the employment market remains strong. All of this is forcing markets to believe interest rates may continue to climb and are likely to stay higher for longer.

Higher interest rates call into question company valuations and also increase the chance of a “hard landing” occurring at some point in the near future as consumers and companies start to struggle under ever increasing interest costs.

Here in New Zealand, we have seen interest rates continue to move higher, despite the Reserve Bank maintaining interest rates on hold. This is being driven by offshore moves and a growing belief that interest rates are likely to stay higher for longer. Unfortunately, this means that mortgage rates keep moving higher for everyday Kiwis’.

2. Earnings season in the US

We are a long way through Q3 earnings season in the US (where we find out how US companies have performed in the previous quarter), surprisingly companies performed well with 83% of companies beating expectations. The flip side though is that CEO’s appear to be extremely uncertain and pulled back guidance for the rest of the year, so despite stronger than predicted earnings this quarter, uncertainty about the future created a negative buzz around the results.

3. War in the Middle East

The Hamas attack on Israel rocked markets for a few days while markets took time to understand the ramifications and see whether it would spread further through the Middle East. While oil initially spiked upward, it has now retreated as fears over broader contagion appear to be dying down. The tensions initially seen between a number of Arab countries have started to even out and it is becoming increasingly clear that external countries do not want to get involved. This should keep oil flowing and, hopefully, the price of oil under control.

4. The New Zealand election

Here in little old New Zealand, we had the election and as predicted by many the electorate was desperate for a change and voted the National Party into power. This is likely to have very little impact on financial markets with our markets being driven more by international events than what is happening in New Zealand.

The one area that is expected to be pushed higher are house prices. The National party have announced a number of housing friendly initiatives (interest deductibility, foreign buyers, and improvements to landlords rights) which are likely to push house prices higher.

5. The launch of crypto ETF’s

Despite all of the uncertainty, the price of Bitcoin continues to rise consistently hovering around the US$35,000 mark for the past few weeks. The primary reason being the expectation that Fidelity, BlackRock and others will launch Bitcoin spot ETF’s which will drive significant demand for the asset class which is very tightly held. You can find out more about it in our blog here.

A week into November, the markets have turned sharply positive. A few negative economic data points have changed the narrative, interest rates have quickly fallen, and markets have rallied. This shows how uncertain and fragile the current economic environment is, investors are reacting strongly to individual data points and continue to jump between positivity and negativity. Unfortunately, this uncertainty is unlikely to change in the short term. Investors expect things to get worse economically and markets to head south but are constantly wrong footed when markets turn positive. It is clearly a very tough time to be an investor. The only way to succeed in the current environment is to ignore the short-term noise. We know markets will do well over the medium to long term and that is what KiwiSaver investors need to remain focused on.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.