Kōura Market Wrap | September 2023

Table of Contents

Kōura Market Wrap | September 2023

11 Oct 2023

Markets are finally coming to grips with continued higher interest rates

Over the past 12 months markets have continually wanted to believe that the fight against inflation is almost over and interest rates will start to fall shortly. Economists have continued to forecast that interest rates will fall in 9 months’ time for the past 12 years. However, that reckoning finally shifted in September, as investors appear to have finally got their heads around the fact that interest rates are likely to stay higher for longer. This updated perspective on interest rates had an unfortunate impact on the markets, resulting in global stock markets falling by 5% during the month. This performance made it the worst month of 2023. Given interest rates have been driving so much of the markets this month, that is the focus of our Market Wrap this month.

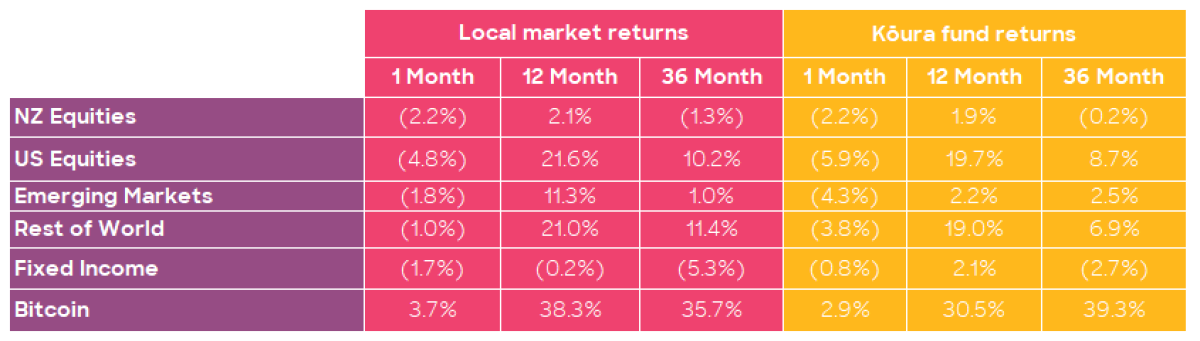

Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ. Local market returns use the relevant market indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index. Bitcoin return is the USD change in price of Bitcoin.

A soft landing is now the consensus view, does that make it more or less likely?

Economic data increasingly demonstrates the resilience of the global economy. Inflation appears to be falling broadly as expected, though contrary to expectation, manufacturing unemployment and other economic indicators remain extremely buoyant, and it looks as though the global economy may manage to avoid the dreaded recession that was so widely predicted at the start of the year.

Why? No one is really sure, but it appears as though there are competing forces in the economy right now that are countering the higher interest rates. Consumers started this hiking cycle in stronger positions than they had ever been before. Through COVID lockdowns, consumers stayed at home, and many were even lucky enough to receive stimulus cheques or other forms of support to ensure they started this tightening cycle feeling richer than they had ever been before.

Simultaneously we have Governments around the world throwing money at companies to onshore manufacturing and build a range of new industries. Governments around the world no longer feel the need to balance their books and the significant amount of spending has contributed to higher inflation, though also is driving further growth.

A soft landing means no recession, which also means interest rates never really fall. Central banks have no impetus to drop interest rates as there is no need to stimulate the economy. Which means higher for longer.

Some have said this feels very similar to 2007, where economists were predicting a soft landing after a short hiking cycle in late 2006 and 2007.

If interest rates stay higher, what does that mean for stocks?

Higher interest rates should be bad for stocks for two simple reasons. As interest rates rise it will result in company earnings falling as their interest bills rise (just like all of us with our mortgage payments).

Secondly, their valuation metrics should fall. If investors can now get good returns on cash and bonds, then the returns they need to earn on equities should also fall. The US market is currently trading at a price-to-earnings ratio of c.18x, significantly higher than its long-term average of 14-15x. If interest rates are expected to remain high permanently, then we probably need to expect that price-to-earnings ratio to fall. What this means for investors is that the price they are willing to pay for a share in a company will fall if they expect a fall in company earnings.

Are interest rates high by historical standards?

Interest rates are still trading broadly in line with their historical averages. Looking back to 1985, the 5 year NZD Government Bond has traded at an average yield of 6.6% compared to the current yield of 5.3%, implying that interest rates are still low when looked at on a very long-term basis. This period includes the ultra-high interest rates of the 1980s and also includes the period of ultra-low interest rates over the past 15 years.

At this stage, no one knows what is normal and where the long-term neutral interest rate should be. Economists in the US have suggested that 4.5% - 5.0% is the neutral long-term interest rate as it will deliver a 2.5% return over inflation over the long run.

Unfortunately, you should not be surprised if the current high-interest rates are the new norm.

Are we really done with interest rate hikes?

Consensus around the world is that we will have at least one more interest rate hike. That seems consistent across Europe, New Zealand and the US. Inflation is still above preferred levels, unemployment is still at all-time lows indicating there is no real slack in the economy.

The good news is that a further hike should not impact mortgage rates too much. Markets already expect the hike so that should already be priced into your mortgage.

Will the New Zealand election change anything?

Unfortunately, not. The change being talked about by either party is incremental at best, and as we have talked about in the past, the New Zealand market is driven more by interest rates than anything else. We should not hope that the election magically conjures New Zealand out of its economic funk.

Crypto is up and markets are down, are we breaking out?

Bitcoin was up 4% in the month, against a backdrop of markets. Over the past 2 years, we have seen bitcoin effectively behave like a leveraged play on equity markets, when markets rise, bitcoin does extremely well, and when markets fall, conversely bitcoin falls significantly.

Crypto will continue to be in the news over the following few weeks for all the wrong reasons with the FTX saga continuing to play out in the New York courts.

So, what next?

2023 has been a year of surprises. We started the year expecting a recession to hit, interest rates to fall and markets to remain volatile. So far, we have seen the opposite, markets are up almost 20% year to date, interest rates have continued to rise, and we now appear to be heading for a soft landing (no recession at all).

Looking ahead for the next three months you would be brave to make a call on where markets go next. We could still be headed for a recession or AI could be driving a productivity boost that allows markets to continue moving higher.

Unfortunately, we are still living in very uncertain times, and that is unlikely to change soon.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.