May 2024 Market Wrap: The market bounces back

Table of Contents

May 2024 Market Wrap: The market bounces back

17 Jun 2024

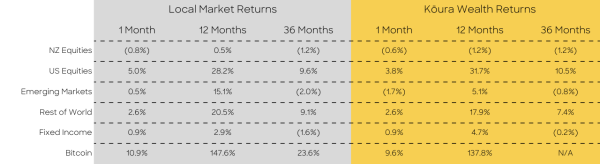

After a tough April, the upward march continued in May with global stock markets lifting 4% driven by strong earnings results, increasing confidence in the timing of interest rates starting to fall and the AI boom! Two consistent themes that continue to drive the markets.

Here in New Zealand, the budget was the only thing on people’s radar, everything in the budget was very well flagged, so no real surprises. It was all about tax and spending cuts.

Interest rates starting to come down?

Globally interest rates are clearly starting the descent down from their recent highs.

The European Central Bank cut their headline interest rate down to 3.75% and the Bank of Canada reduced it’s interest rate down to 4.75% from the 23 year high of 5%. Interestingly neither bank expects inflation to fall back within their target ranges until 2025, though have pre-emptively cut interest rates in an attempt to engineer a soft landing. They are more concerned about the damage they will do from keeping interest rates too high for too long.

Weaker economic data in the US has revised calls for a July rate cut from the Federal Reserve. We believe this is unlikely due to the volatility of the data points. But one thing is clear, people are very nervous and uncertain around where we sit. The big question is around the impact November’s election will have on rate cuts. The prevailing theory had been that the Federal Reserve will not want to cut rates too close to the election, so if no cut comes in July, we are potentially looking at a December rate cut to get things going.

Closer to home, economists in Australia are pencilling in a rate cut until later in the year and here in New Zealand the expectation has been pushed well out until 2025 (more on that below).

AI goes from strength to strength

Nvidia reported earnings on 30 May and managed to deliver revenue and earnings 10% above expectations. Demand for Nvidia products remains strong across the board, a good example of this is Tesla who have placed a $4b order for Nvidia hardware to continue to develop their AI offering.

The strong Nvidia results pushed up a number of other technology and AI related stocks as it demonstrated that the current AI boom has a lot further to run. The Nvidia share price is now up 144% year to date and has become the 3rd US company to ever each a $3 trillion market cap following Apple and Microsoft. It now has a market cap greater than Apple.

NZ Budget was a bit of a nothing announcement

Nicola Willis announced her first budget on 30 May. The tax and spending cuts were well flagged resulting in minimal surprises on the day. The big debate on the day was whether tax cuts are inflationary or not.

Most economists believe that they are inflationary, but they were promised so therefore needed to be delivered. The government is still expected to run an annual deficit of $7.6b and we are not expected to reach surplus for another 3 years. In our view, any government deficit is inflationary as it is adding spending into an already overstretched economy.

In our view the most interesting (and scary) part of the economy was the economic forecast from Treasury. They are expecting a 2.9% GDP per capita contraction in 2024, slightly higher than many had initially anticipated. The economy is clearly a bit sicker than initially anticipated. The positive to this sobering news is that it means interest rates could fall much quicker than anticipated.

Bitcoin remains range bound

Bitcoin continues to trade in the range of $60,000 – 70,000 with the price largely moving in line with broader risk on and off sentiment. Clearly ETF volumes are driving most of the price action though that is clearly a result of risk sentiment in the broader financial markets.

With the Bitcoin halving completed in late April, we have yet to see any price action resulting from this, though it is still early days.