The rising tide of Digital Advice: How New Zealand compares to the rest of the world

The rising tide of Digital Advice: How New Zealand compares to the rest of the world

14 Feb 2020

Digital Advice has taken off overseas but is a relatively new concept in New Zealand.

Relying on digital platforms for everything from dinner reservations to dating is routine for many of us in 2020. But, when it comes to managing our money we have been slow to catch on.

Why is digital advice important?

Robo advice can cover a broad spectrum of services. Essentially it aims to replace the face to face savings and investment advice one can secure from an advisor with online, automated financial guidance based on algorithms.

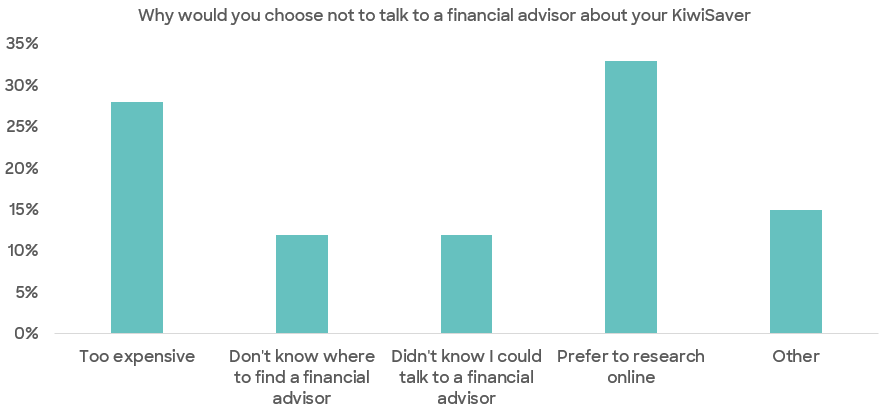

We can all agree that the key to making the right decisions is asking for help. There is however only about 2000 authorised financial advisers in New Zealand and Kiwi Bank research has found that less than 20% of Kiwi’s have an adviser. Our own follow-up research confirmed that only 41% of people would even be open to talking to a financial advisor citing cost or lack of trust as being the key issues.

What is scarier is that while 68% of Kiwi’s believe their KiwiSaver fund will be a very important tool for their retirement, an FMA review of KiwiSaver sales in 2015 found only three in 1,000 KiwiSaver sales or transfers occurred with personalised advice. It is no wonder then that 53% of Kiwi’s are invested in the wrong type of KiwiSaver fund.

What is scarier is that while 68% of Kiwi’s believe their KiwiSaver fund will be a very important tool for their retirement, an FMA review of KiwiSaver sales in 2015 found only three in 1,000 KiwiSaver sales or transfers occurred with personalised advice. It is no wonder then that 53% of Kiwi’s are invested in the wrong type of KiwiSaver fund.

Robo advisors are designed to play the role of the financial education teacher most of us didn’t have growing up and by not having as many digital advisers as our international counterparts, we Kiwis are missing out.

We have an industry that’s dominated by the banks

The FMA changed the regulation to allow for the introduction of digital advisers in the NZ market in 2018. Despite this, we only have a handful of providers in the market with Kōura being one of the first to provide free personalised digital advice for your KiwiSaver.

Part of the reason for this is that we have a KiwiSaver market that is dominated by banks. According to the research house, Morningstar, there are six providers who between them have around 75% of the KiwiSaver market. ANZ alone has 24.5% of the KiwiSaver market, as measured by Morningstar which is closely followed by ASB Bank.

Banks have won a large share of the KiwiSaver market because many of them are default providers and not because they have historically provided great returns or customer service. The banks would like customers to think that KiwiSaver is like any other simple savings account and not something you need to think about. If people actually realised the decisions they need to make with their KiwiSavers money and the fact that your KiwiSaver fund is extremely different from a traditional bank product they would probably look elsewhere.

It doesn’t help that most of us New Zealanders are quite apathetic about our KiwiSaver investment (surely, retirement is far away and I have a long time to sort things out) and because our account balances are quite low, we haven’t seen the need to proactively secure advice about our KiwiSaver fund or switch to a potentially better provider.

Why else are almost 400,000 New Zealander’s still sitting in default funds earning significantly fewer returns?

How Digital Advisers are helping with Retirement Savings Overseas

Recent research from the Westpac Massey Fin-Ed Centre revealed that a two-person household living in the city now needs to have saved $787,000 to fund a ‘choices’ retirement. Yet, a majority of Kiwis are currently only contributing 3% of their income to KiwiSaver account. We don’t realise that doing this means having a weekly income that’s less than half of what you would be currently earning.

It’s clear then that all of us need access to quality financial advice to help us achieve the kind of retirement we are aspiring to. Internationally, the retirement planning crisis has found a new friend in digital advice.

According to estimations by the European Banking Authority, Robo-advisors are expected to manage USD 450 billion by 2020. In fact, the industry has experienced such incredible growth, that by the year 2025 Robo-advisory could manage assets worth $5 trillion to $7 trillion in the US alone, estimated by Deloitte.

| The Investopedia Affluent Millennial Investing Study found that 20% of affluent millennials (ages 23 – 38) use Robo-advisors, compared to only 13% of Gen x respondents. The survey suggested that of those who do us Robo-advisors, 26% felt knowledgable about investing and were 2x as likely to manage their finances daily. |

Robo advisors like Wealthfront have remarkably low management fees and provide users with an array of services in addition to financial planning like goal planning assistance and a portfolio line of credit. Others, like Betterment, provide clients with the ability to sync all their external accounts and automatic rebalancing of portfolios.

“Robo-Advisors were born out of the confluence of the financial crisis and the rise of the smartphone,” says Caleb Silver, Investopedia Editor in Chief. “They're becoming more popular now as the first generation to grow up with smartphones enters into the investing and financial planning part of their lives, which they fully expect to be a digital and transparent experience.”

What does this mean for your KiwiSaver?

Robo-advice is poised to address the retirement planning advice gap, especially in NZ where most of us will be relying on our KiwiSavers for our ’20 Golden Summers’. Despite this being an emerging area, a Kiwi Wealth study on this topic shows that one in five New Zealander’s would be likely to consider using a Robo-adviser to manage their retirement finances.

Financial advisers typically only want to work with people that have a big enough balance to justify the commissions on the accounts. In comparison, Robo-advice is available for everyone to access, even those with a very small pool of assets. For example, At Kōura, we have over 200 portfolio variants that we use to construct personalised portfolios for our clients. This means we have a variation to match everyone’s goals.

Within KiwiSaver, the biggest value that digital advice also brings to the table is that it doesn’t let members ‘set and forget’.

Digital advisors remind clients to review their account so that their portfolio’s asset allocation can change as they get closer to retirement. Unlike life-stage based KiwiSaver schemes that move customers to an appropriate fund every 5 – 10 years, a digital advisor like Kōura rebalances portfolio’s using a glide path so that clients don’t lock in a loss should their ‘life-stage’ change when the market is experiencing a downturn.

Not only do Robo-advisors simplify investment but they also provide consistent advice that is beyond bias. The best part is that it comes with a minimal cost (at Kōura our advice is totally free and we only charge a 0.63% fee for funds under management) making it one of the most attractive investment options in the market. In fact, Professor Nir Vulkan from Saïd Business School, University of Oxford says, “Except for the very high-network individuals, Robo-advisers will become the dominant form [of financial advisors] in the next decade.”

Widespread take up of Robo-advice will unlock good, low-cost financial advice to more New Zealanders than ever before. A concerted effort from financial services providers is the only way to make digital advice a core instrument in financial services. Without it, we risk falling further behind the world in wealth creation.

.png)