September market update

September market update

7 Oct 2021

A recipe for volatility; Covid, inflation, China deleveraging, and supply chain issues

The end of September sees the end of Q3 in the markets and jitters are starting to show. After months of record-breaking returns, September has seen investors looking for reasons why this can’t continue. September global markets fell by 3.6%, breaking a spell of seven consecutive months of gains. The only exceptions to the rule were New Zealand up 0.4% and Japan’s Nikkei 225 up 5.5%. Judging by how we ended September and how October has started we could be in for a wild ride.

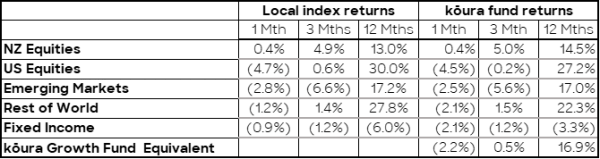

[1] Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4% Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%

So, what are the reasons for this seemingly sudden about-turn? September was a massive news month for the markets, so there was a huge amount to take in:

- US Federal Reserve Chair Jerome Powell confirmed that they would stop the purchasing of bonds on the market by the middle of next year (tapering). The US Federal Reserve is currently purchasing $120billion in bonds per month to keep interest rates low. This is expected to drive interest rates higher. Though at the same time Jerome Powell did clarify that any lifting of the fed funds rate (the equivalent of our OCR) are a long way away.

- Growth in China, the world’s second largest economy seems to be slowing with industrial production and retail sales numbers both coming in materially lower than expected. Economists are increasingly concerned that growth in China is slowing and we are starting to see the lingering effect of Covid in their economy. This is particularly concerning given China is a good 6-9 months ahead of the US in its Covid economic recovery, so does this mean that the US economy will follow through shortly?

- China’s crackdown on capitalism may finally start to hit mainstreet. China’s largest developer Evergrande looks set to lurch into bankruptcy. It has US$300billion of debt (6x New Zealand Government’s net debt) so there is concern that this default may cause chaos in the over leveraged Chinese banking system.

- Inflationary pressures seem to be increasingly persistent and are refusing to go away. We are seeing worker shortages, shipping and supply chain issues continue and commodity prices have returned to highs. Economists are increasingly concerned about stagflation, a period of high inflation, low economic growth and high unemployment.

- US economic growth estimates have fallen sharply over the month as a result of weaker spending, a sharp decline in consumer confidence and the lingering impact of Covid. Retail and hospitality have not recovered as quickly as expected which is largely attributed to the recent surge in Delta creating fear to stop people heading out.

- Washington's dysfunction appears to be hitting all-new levels with the fight moving from a partisan spat between Republicans and Democrats to a war within the Democratic party. The US$1trillion infrastructure bill (a core piece of the Biden agenda) has been put on hold because of infighting among Democrats in Congress. If Republicans continue to block Democrats efforts to raise the US debt ceiling by 18th October, the US Federal government is set to run out of money and will result in what President Biden describes as a “meteor” crashing into the US economy. How much longer can the world’s largest economy and politicians continue to operate in such a dysfunctional way!

With all of this doom and gloom, it is amazing that markets did not fall further in the month. Though investors still keep returning to the core fundamentals:

- Economic data remains positive - labour market data shows ongoing wage inflation, the falling unemployment rate and rising producer prices

- While GDP growth is not as high as initially expected, Q3 growth is still expected to be over 6% in many parts of the world

- Interest rates remain low, and are likely to stay that way, and finally

- Companies are doing extremely well – analysts have posted a record 5 consecutive earnings increases for companies in the US S&P500. A strong consumer keeps on spending on durable goods which is driving growth and a source of significant profit for many companies

Volatility is a part of investing, and we do appear to be seeing higher levels of volatility at the moment with so much going on. We expect volatility to continue over the next few months as markets digest the issues above but at the same time economies look to open up as vaccination rates allow. As we have seen and said many times before it is time in the market not timing the market that will lead to long term strong portfolio returns. Many of the doom and gloom issues that we have talked about have been around for many months – and in that period we have seen continued market growth – only now have markets started to take notice of some of the downside risks. At the time of writing, 5th October, four of the last five trading days has seen markets move 1% or more, and every day for the last five days this has been in the opposite direction!

USA

US markets all closed lower in September, the NASDAQ the worst-performing down 5.27% with the S&P 500 down 4.65%, its worst month since March 2020 reacting to the reasons mentioned earlier.

For some interesting stocks, Virgin Galatic was cleared for take off in space tourism, Moderna is up 260% in the year to the end of September, and Boeing rose on analysts expecting international traffic and aircraft demand to start to improve as COVID-19 vaccines begin to be administered in most major markets.

New Zealand

The New Zealand market closed in slightly positive territory in September even though the country remained under Covid restrictions. Stronger than expected GDP growth of 2.8% for the second quarter of 2021 pointed to strong momentum in the economy, but at the time of the release the country was in lockdown so was greeted with the uncertainty of whether it was a one-off or would be hampered going forward due to economic lockdowns.

The final stages of reporting season delivered over and above analyst expectations. Some of the standout performers were Synlait Milk (up 12.7%) and the retail stocks The Warehouse and Briscoes Group who both announced amazing very strong results and increases in dividends.

Companies associated with travel, Auckland Airport, Air New Zealand, and Serko all had positive share price returns in September. The spectre of travel for vaccinated passengers is getting tantalizingly close for investors!

Yesterday the Reserve Bank of New Zealand increased the Official Cash Rate by 0.25% which was widely expected given the “postponed” announcement that was due in August the day after NZ was plunged into lockdown. The immediate impact is an increase in the cost of borrowing, with some banks already increasing floating mortgage rates.

Europe

The FTSE100 was the best performing market in Europe in September, down by only 0.16%.

Toward the end of the month, some of the stark realities of Brexit appeared with the army called in to deliver fuel to forecourts as a labour shortage of truck drivers saw pigs being slaughtered and burnt as there was were insufficient workers to process the carcasses (no more Eastern European workers).

Growth for the second quarter in the UK was a higher than expected 5.5% as household consumption made the largest contribution following the easing of Covid restrictions. The energy sector performed well with BP plc up 14.6% over the month, and Banks gained as bond yields rise. Rolls Royce was up 22% after it announced the sale of its Spanish Unit.

Also in Europe, consumer confidence in September rebounded, while Industry Confidence remained unchanged at its second highest level on record. Meanwhile, Angela Merkel is staying on in a handover role in Germany as the new government elected in the German Federal elections is formed.

China

China was still dominant in Emerging Markets news, with Evergrande, listed in Hong Kong, and one of China’s largest real estate developers with debts totaling over $300 billion, warned investors of cash flow issues that could lead to default on interest payments. To date, attempts to sell assets and minimal disclosure on how the company intends to move forward has seen protests outside the company offices and pressure on the share price has seen it fall 79% since the beginning of this year. At the time of writing it has been suspended from trading. This is an issue for investors outside of China as Real Estate accounts for 30% of China’s GDP, and may have flow-on effects into other markets should Chinese growth slow.

Further tepid Economic data showed contraction in the manufacturing Purchasing Managers’ Index for September and a widening trade surplus. Meanwhile, the tighter controls on internet giants continue.

Supply issues through the Taiwan Strait continue to hinder Taiwan chipmakers which supply chips into smartphones and cars, as China continues to threaten the country.