The Kōura March market wrap

Table of Contents

The Kōura March market wrap

7 Apr 2022

The kōura market wrap for March

Inflation, rising rates and the Ukraine conflict are now priced in, but there are other headwinds gathering, in particular for sustainable investments.

After a rocky start to 2022, March was this year’s first positive month in the markets, with the broader MSCI world index eking out a hard-fought 3% gain. What’s more, to everyone’s surprise, share markets have risen by nearly 7% since the Ukraine invasion began in late February.

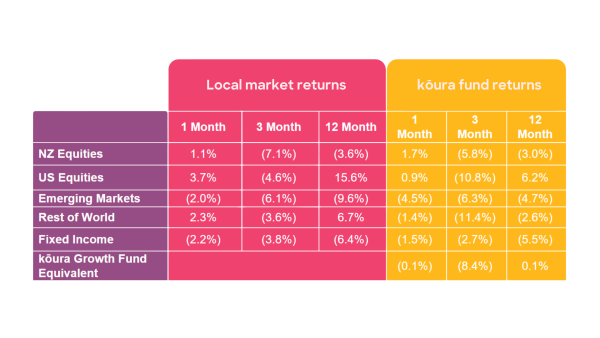

So, some good news there. But as illustrated in the graph below, both Emerging Markets and Fixed Income continued to underperform. For Emerging Markets, this was largely due to continued uncertainty in and around China. As for Fixed Income, interest rates and medium-term interest rate expectations continue to rise, which is pushing the value of Fixed Income assets down.

Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4%, Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%. The Kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the Kōura funds invest in.

This month’s performance shows, once again, how difficult – if not impossible – it is to ‘time’ the markets and predict the peaks and bottoms accurately. Interestingly, some key factors that have been driving global market behaviours of late, like inflation and interest rates, are now being absorbed and normalised. But the market is still rife with uncertainty, so this is not the time to become complacent.

For more on this, here’s our Market Wrap.

1. Companies appear to be shrugging off high inflation

Despite the high levels of inflation seen in the economy, over the past few weeks several companies have reported strong earnings growth. This has been driven by companies passing price rises on to consumers without impacting demand – which has resulted in higher profit numbers.

It’s a trend we’ve seen in the past and appears to be the case once again here. However, the big question is around consumer demand: how long can that hold up with the combination of rising interest rates, inflation, and fuel prices?

2. Markets no longer expect a drastic impact from interest rates

We know how investors hate surprises, and the unexpectedly high inflationary pressure has certainly been one of those. In January and early February, investors reacted strongly to high inflation and the prospect of interest rates quickly rising.

In March, however, the market seems to have found more solid footing again. And that’s despite the fact that the Federal Funds Rate (the US version of the Official Cash Rate) is now forecast to hit 1.8% by the end of the year, from its starting point of 0.25% - a significant increase. It appears that the market has processed this information and no longer expects a drastic impact from it.

Of course, any further acceleration in rate increases will likely cause markets to wobble, but they seem to have a much better understanding of what higher rates might mean for them from here.

3. China seems to be going from bad to worse

This year, the Chinese market has been by far and away the worst-performing global market, currently down 15% year to date. And March was no different, with China’s benchmark Shanghai Composite index falling a further 9%.

There are many factors behind this trend, including the ongoing crackdown on the technology and property sectors and lingering concerns about the impact that a ‘zero Covid’ policy might have on their economy.

Added to this, investors are now nervous that China might look to help Russia evade sanctions, which could in turn result in sanctions or penalties on Chinese companies. It might not be a far-fetched concern, as there’s a strong contingent in Washington who wouldn’t mind punishing China, and China’s support to Russia would offer a great opportunity to do so.

4. The Ukraine war does not appear to be having a major impact on economics

And speaking of the Russia-Ukraine conflict, markets seem to be pricing in a long drawn-out stalemate, with no real change from the status quo. In other words, markets are taking the view that whilst Ukraine is catastrophic from a humanitarian standpoint, it’s unlikely to have a significant impact on the global economy or markets.

The sanctions will cause devastating impacts on the Russian economy, but with it being a small player on the global stage, Russia’s further isolation is unlikely to cause material issues for many companies. In addition to this, Germany has made it very clear that it will not stop purchasing Russian gas: according to chancellor Olaf Scholz, costs would be too great for the German economy and population.

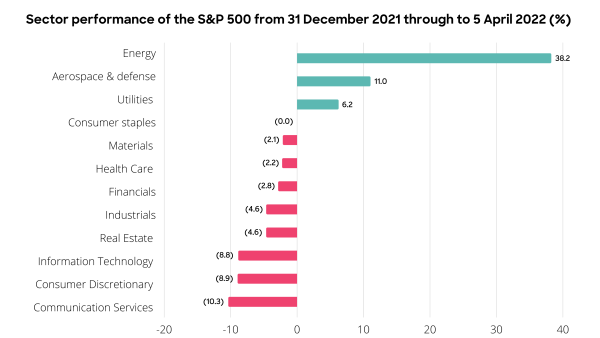

5. Sustainable funds are starting to feel the pinch

‘Sin sectors’ like fossil fuels, mining, aerospace and defence are the top performers year to date, while the technology sectors remain are the tail-end. As you may know, most sustainably focused funds are not allowed to invest in the sin sectors, and as a result, are heavily focused on technology and consumer-orientated companies.

This has been a great strategy for the past two years, but it’s quickly starting to unwind. As the chart below shows, sin industries have largely outperformed other sectors for the year to date in the US market. This has been driven by a combination of higher interest rates (which overly punish growth-orientated tech sectors) and the Ukraine war, which has led to higher energy prices and increased demand in the aerospace and defence sectors.

Kōura fund performance

Unfortunately, the kōura funds have underperformed the markets year to date, as a result of two key factors:

- The strengthening of the New Zealand dollar, driven by rising interest rates and our country increasingly being seen as a safe haven in these uncertain times;

- The lackluster performance of sustainable funds, as shown above, has not fared well in the current war-driven economy.

As always, it’s impossible to tell from here where the markets will go. Our view is to focus on the long term: KiwiSaver is a long-term investment, and the best course of action is to calmly wait it out and see what might happen next. We’ll continue to keep a close watch on market trends and update you as additional insights are brought to light.