The Kōura Market Wrap for April

Table of Contents

The Kōura Market Wrap for April

4 May 2023

Markets in 'wait and see' mode after turbulent start to the year

Inflation, rate cuts and fall out from an averted banking crisis all leading to lackluster markets as investors wait to see what is coming down the pipe.

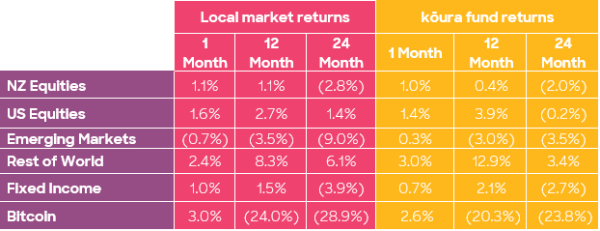

Global markets had a quiet month in April, squeezing out a 1.7% gain during the month, though extended their year to date returns to almost 9%, what recession you might ask. In terms of news and updates, April was a very quiet month with no major news events or announcements. Most Investors seemed to be sitting on their hands trying to guess when or if the most anticipated recession of all time will actually turn up and what it might mean for the markets.

Some of the things that we at Kōura have been thinking about this month are:

1. The market is clearly not expecting a recession

Markets have been expecting a recession all year following 2022’s rapid ascent in interest rates. But the timing for this recession continues to be pushed out and the expected severity continues to diminish. While the debate continues the market continues to rally.

Over the past month we have seen more evidence that the supposedly inevitable recession may not be quite so inevitable:

- Employment data around the world remains extremely strong.

- Energy prices are falling which will act like a red rag to a bull for the global economy.

- We are starting to see a housing recovery in the USA.

- European confidence and growth continues to grow.

This slew of positive data continues to push the recession debate into 2024 rather than being a 2023 phenomenon.

But another key plank of the market story at the moment is inflation. Markets expect inflation to normalize early in 2024 which will hopefully allow central banks to start cutting interest rates.

2. Inflation is falling back, but is it falling far enough?

Inflation has peaked and is clearly falling across most markets. In New Zealand the latest Consumer Price Index came in lower than expected at 6.7% for the year, a significant fall from the previous peak of 7.2% and much lower than many expert’s expectations.

This trend has been repeated in Australia, Europe and the USA which have all seen inflation numbers starting to fall.

It appears across most economies that inflation is currently running at 5-6% on an annualized basis versus the prior peaks of 7-9%. This is a material improvement from where we were, but still a long way from most Central Banks targets of 2-3%.

Since the start of this journey, we have talked about how moving from 7 to 4% inflation would be relatively easy, but moving from 4% down to 2% could be extremely difficult.

Forecasts are for inflation to return to normal in early 2024. We are not convinced that will be possible without a pretty sharp recession to pull the labour market back into shape.

3. Markets still expect rate cuts to hit toward the end of 2023 or early 2024

Interest rate markets still expect rate cuts in early 2024 off the back of inflation returning to normal and (most probably a recession). This assumption is important as the falling interest rate levels are supporting current valuation levels (18x PE on the S&P 500 versus a long-term average of 15x over the past 20 years) which can only be supported by a lower than long term average cost of capital.

5-year interest rates in the USA have fallen from highs of close to 4.5% at the start of the year all the way down to 3.5% driven by the expectation that rates will start falling shortly.

This will only happen if inflation is quickly tamed which in all likelihood will be caused by a recession. The fixed interest and equity markets are clearly telling two very different stories at the moment.

4. The banking crisis has a bit of a tail, though the sting is largely over

March was all about the banking crisis in Europe and USA with the failures of Credit Suisse and some regional US banks. First Republic reported earnings in the last week of April, and it was clear that they needed to raise capital as like the others, they had not managed their interest rate risk or funding appropriately.

Apart from First Republic though, there does not appear to be a slew of banks looking for bailouts which is giving the markets confidence that the crisis might be heading towards an end.

5. Technology is clearly the big driver of 2023

The S&P500 is currently up 9% for the year to date, though if you normalize out the large technology names the S&P 500 is broadly flat.

Many of these large technology companies are up 30 – 40% this year off the back of strong corporate earnings and the recognition that they are very large platforms that should be able to withstand competition and a potential recession.

6. Adrian Orr was brave with a 0.5% rate rise, though appears to have got it right

Adrian Orr shocked the New Zealand market with a 0.5% interest rate rise in the middle of the month. This shocked mortgage holders and investors who had been hoping that the RBNZ might even pause rate hikes.

Like many decisions over the past 2 years, the RBNZ actions differed from what was happening around the world. They have tended to go earlier and be more aggressive. The Reserve Bank of Australia had paused their rate rises, and the US Federal Reserve had hinted that their previous rate rise was likely to be their last, leading New Zealand commentators to suggest it was time to hold here in New Zealand as well.

The reason for the significant rate rise was that market pricing had indicated sharp falls in interest rates through the remainder of 2023 which would have allowed banks to start dropping interest rates, easing financial conditions and potentially spurring inflation higher, the opposite of what the RBNZ had hoped to achieve.

In hindsight, it appears Adrian Orr may have been correct in his assessment, labour market data continues to appear stronger than expected which may mean we have even more rate rises coming.

Our conclusion is that certain sections of the market are starting to show some positive signs, but we are certainly not out of the woods yet. Inflation is slowing, and the market has priced in expectations of rate hikes to slow or stop towards the end of this year. But just because some quarters of the market are not expecting a recession does not mean it won’t happen.

Our thinking is that investors need to remain vigilant while we wait and see where the markets land.