The kōura market wrap for August 2022

Blog Contents

Table of Contents

The kōura market wrap for August 2022

7 Sep 2022

The investing ‘crystal ball’ is cloudier than ever

The kōura market wrap for August

August was the month that proved almost everyone wrong and demonstrated just how hard it is to pick market and economic cycles.

There is no question that the data is confusing and very rarely delivers what people expect. During the past quarter, we have seen real GDP growth fall to zero, yet companies continue to deliver great earnings growth and the labour market remains infuriatingly strong. Inflation factors appear to be receding (commodity prices are falling and supply chains are unjamming), yet the Federal Reserve Governor warned markets that the Federal Reserve will keep fighting hard on inflation until they see the labour market softening. Meanwhile, European energy markets are going from bad to worse, though equity markets have a belief that politicians will protect consumers and industry from the worst of these impacts.

All of this saw markets fall by almost 4% in the month, giving back some of the June and July gains. In particular, risk assets like tech and crypto have fallen harder, with the Nasdaq dropping by 5% and Bitcoin ending the month 17% lower. We are starting to see a clear pattern: a slight ripple in equity markets results in a tidal wave in the crypto markets.

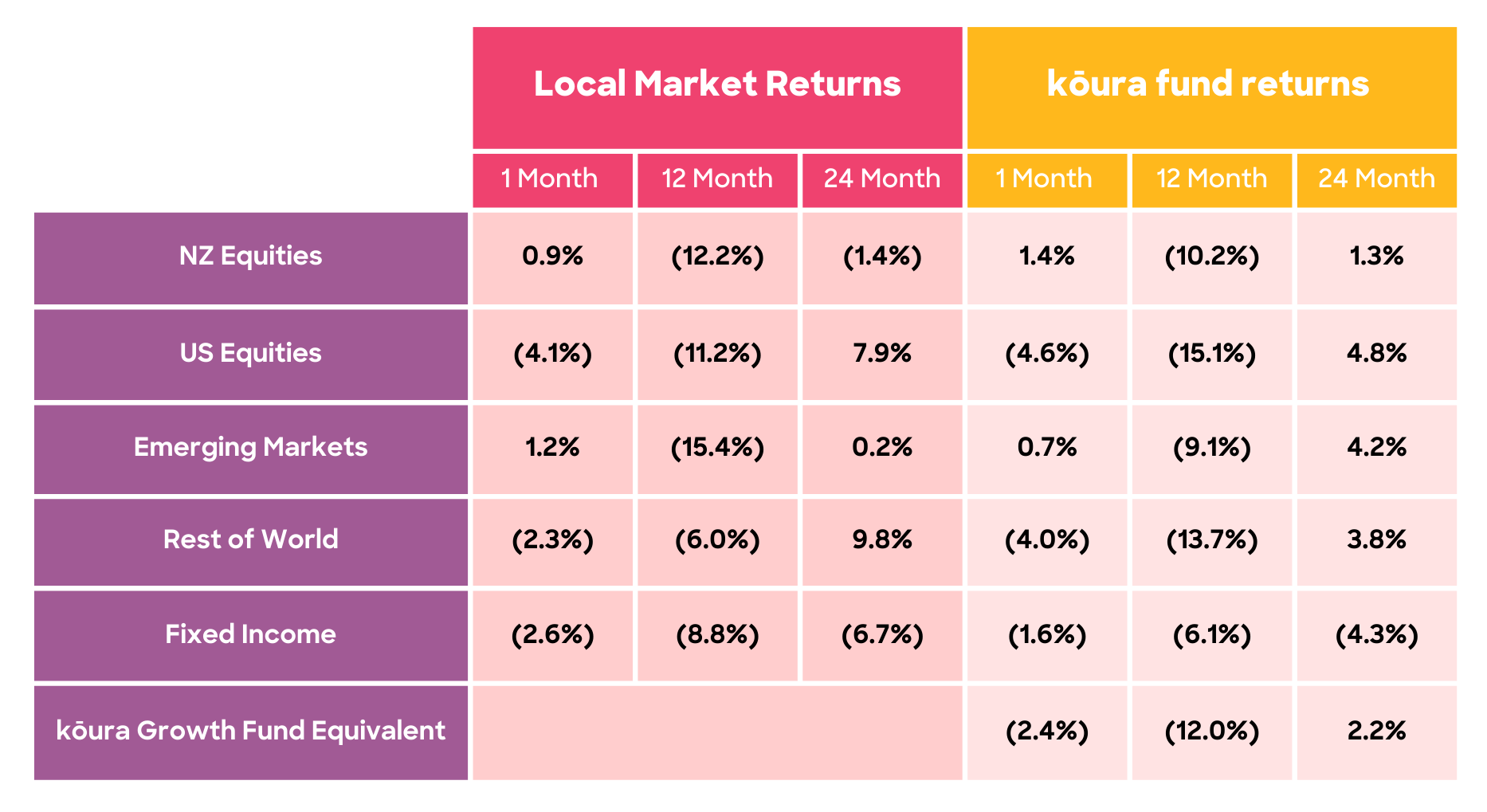

Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 36.6%, Emerging Markets 7.8%, Rest of World Equities 15.6%, Fixed Income 20%. The Kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the Kōura funds invest in. Past performance does not equal future performance.

So, what has actually happened? Read on to learn more.

1. Earnings Season delivered great results

Looking at the Earnings Season, it is fair to say that Q2 results delivered well ahead of expectations. With real GDP growth falling to zero and sky-high inflation, many analysts thought that companies would struggle to deliver good earnings in this environment. But defying these predictions, US companies delivered 6.5% EPS growth in the quarter and 75% of companies beat analyst estimates.

We saw the same thing happen here in New Zealand, with most large companies reporting strong results. Some of the Covid-hit companies (A2 Milk, Sky City and THL) appear to be on the mend, while a red-hot economy has benefitted the building sector (Fletcher Building and NZ Steel) and the electricity companies with wholesale energy prices rising.

The issue, now, is what comes next. Very few companies (both in New Zealand and the US) were willing to give guidance due to the significant economic uncertainty currently facing the world.

Despite facing down a recession and very weak consumer confidence, at this stage, companies are having no issues in passing through inflationary price rises to customers, who seem willing and capable to pay them. This is a result of the very tight labour market, coupled with the fact that many consumers are in a strong personal financial position following two years of lockdowns and Government stimulus.

2. Growth has stopped in the developed world (or has it?)

As we mentioned last month, real GDP growth in the developed world has effectively halted, with most countries reporting negligible (or slightly negative) real GDP growth through the quarter. That said, it is worth pointing out that real GDP growth is adjusted for inflation.

We typically focus on real GDP growth as inflation eats away at spending power and dilutes the impact of any growth through higher prices. But with inflation rates running in the 8-10% range, these real GDP numbers mean that there is still a significant amount of nominal GDP growth happening. And clearly companies are benefitting from that nominal growth, as they are able to grow and pass through the impacts of higher prices.

From a company performance perspective, it is becoming increasingly clear that we need to focus on nominal GDP growth rather than real GDP growth. It is also a good reason why it is important to own equities in a high inflation environment.

3. The labour market remains tight, is it structural or is it temporary

Globally, labour markets remain extremely tight. Across the entire developed world, companies are in dire need of extra staff and unemployment levels are well below pre-pandemic levels in most countries. It has never been a better time to be an employee!

So, how did we get here? There have been several driving factors, starting with the very strong economic growth seen over the past two years with the Covid 19 rebound. More importantly, though, this tight labour market is a function of a shrinking population of people looking for work. Workforce participation (the proportion of the population that are actually employed or seeking a job) has been declining for a number of years, but Covid has accelerated that trend.

The pandemic prompted people to evaluate their lifestyles and many started to recognise that there is more to life than just work. As result, a lot of those who were unhappy in their job did something about it. For example, we have seen people bring forward retirement plans and others reduce working hours.

It remains to be seen whether this is a permanent shift or temporary. Importantly, economic growth over the past 50 years has been driven by cheap labour, so a key question we need to be asking ourselves is: are the days of cheap labour over? More on that in a later blog post.

4. That Jackson Hole speech

On 26 August, Federal Reserve Chairman Jerome Powell gave a much-anticipated speech at the annual economics symposium in Jackson Hole. It was a short and sharp speech that only took 6 minutes but was extremely clear in its conclusions:

-

The Federal Reserve remains entirely focused on fighting inflation;

-

It has learnt the lessons from the 1970s, when the Federal Reserve called victory on inflation far too early and enabled a second bout of even higher inflation;

-

The labour market remains the key concern; and

-

Fighting inflation would most likely cause short-term pain for American households, which would be less painful than if they did not win the inflation battle.

As we mentioned last month, in his July speech, Powell seemed to imply that the Federal Reserve had done the bulk of what need to be done to combat inflation. Most analysts saw it as a sign that the inflation battle was close to an end, but Powell’s latest speech squashed this interpretation entirely.

Now, it is clear that the Federal Reserve will likely maintain interest rates higher for longer, even if that results in a hard landing. And that may keep a ‘lid’ on stock market performance. Of course, stock markets are not a direct responsibility of the Federal Reserve – but their performance matters to the central bank.

As The Economist(1) recently commented, stock markets play a key role in shaping financial conditions. Essentially, when share prices rise, consumers feeling wealthier and tend to spend more – which is problematic for a central bank fighting inflation. So, it is hard to see the Fed letting equity markets rise much further from here.

5. Why aren’t markets pricing in chaos in Europe?

At the moment, European energy markets are going through the ‘perfect storm’. A hot and dry summer has meant that there is not enough water to cool French nuclear reactors or fill Norwegian hydro dams. And on top of this, Russia has been playing around with gas supply and finally announced at the end of the month that Nord Stream 1 would be closed, due to a fault that apparently cannot be fixed until sanctions are lifted.

Wholesale electricity prices in Europe are ten times their longer-term averages and consumers in the UK are expecting their monthly electricity bills to be four or five times higher than they were this time last year. Industry will not be able to operate, and consumers will need significant financial support to get through a very cold winter.

Interestingly, however, markets do not appear to be pricing any of this in. Year-to-date equity market performance is similar to the US, and most European equity markets performed in line with their US peers in the month. There has been a significant weakening of the Euro, which has now fallen to 10-year lows, but the current situation has not yet hit company earnings or valuations.

In our view, markets expect Governments to bail out consumers and industry. This is not a crisis of their making and to keep people employed and warm/alive over the winter months, support will need to be provided – at a significant cost to individual country balance sheets (which is also why the Euro is falling).

6. And what’s happening in little old Aotearoa?

Given the market is largely driven by what is happening offshore, we don’t often talk about our own New Zealand market. But August was a good month for it, driven by strong corporate earnings and increasing confidence in our local economy. Amazingly, medium to long term interest rates in New Zealand have risen by 20% in the past month, with the five-year swap rising from 3.2% up to 4.0%.

Economists are increasingly taking the view that we might just experience a short and shallow recession, before quickly resuming growth. Economic indicators remain strong and many believe that, once we reopen the floodgates to immigration, all of our problems will be solved.

The big unknown, though, is the impact of housing on our economy. We have seen one of the strongest property markets in the world over the past two years, which means that now firmly in bubble territory and are severely exposed to a property crash. Blomberg lists New Zealand as the most at risk global property market. A significant fall in property values will result in everyday Kiwis feeling significantly poorer, potentially leading to further economic retrenchment.

Sources: