The Kōura market wrap for July

Table of Contents

The Kōura market wrap for July

9 Aug 2023

The market rally is broadening beyond tech

July was another strong month for investment markets, with the prevailing narrative increasingly favouring the prospect of a no/very soft landing. The question is, what’s next?

Markets were up almost 3% in July, taking their year-to-date gains to a staggering 21%. And unlike prior months, the market rally has broadened, with non-tech companies delivering the strongest performance in the month.

Employment markets around the world are holding up well, and confidence surveys continue to surprise to the upside. Market participants have effectively priced out a 2023 recession, and even the delayed 2024 recession increasingly looks like a slowdown rather than a traditional recession.

The big question is – what’s next? Markets are already trading well above even the most optimistic forecasts for the full year. And it is now much more than a tech recovery, or AI boom; it’s a broad market rally driven by significantly stronger economic growth.

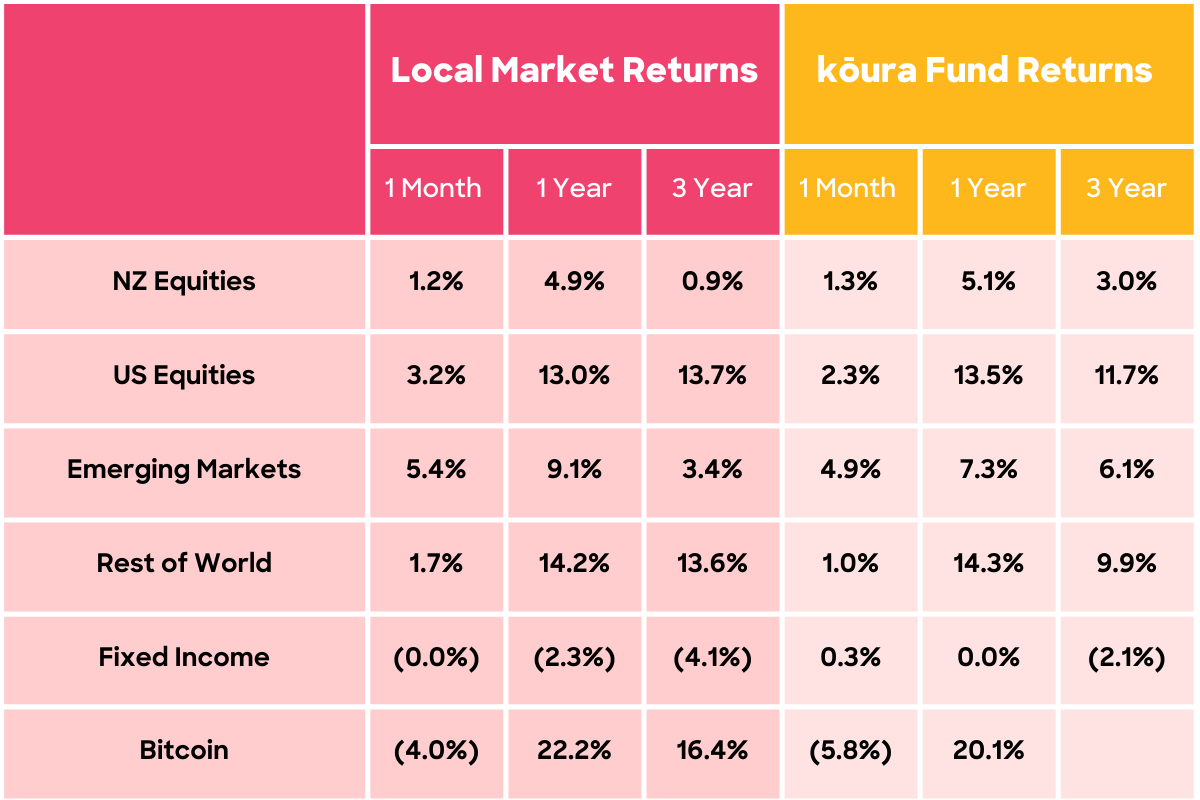

Kōura returns are pre tax and post fees. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ.

Local market returns use the relevant market indices; NZ Equities uses NZX50 index; US Equities uses S&P500 index; Rest of World uses MSCI EAFE Index; Emerging Markets uses MSCI Emerging Markets Index, Fixed Interest uses Bloomberg Aggregate NZ Composite Bond Index.

Are we at the start of a new AI-powered golden age that will drive higher productivity growth? What is the new normal in terms of interest rates? Can the large technology behemoths continue to deliver double-digit returns (their valuation levels require them to)? These are all questions that investors are asking themselves right now, and unfortunately no one knows the answers.

So, let’s have a look at the detail around what happened over the past month.

1. The US Fed raised interest rates even further

As expected, on 26 July, the US Fed raised their policy rate once more, nudging the benchmark borrowing rate by a further 0.2% to a range of 5.25%-5.5% – the highest level in 22 years.

Unlike other meetings, the Fed effectively removed all forward guidance, clearly stating that any future decisions would be data dependent. This means that there is clear potential for further rate rises, depending on how inflation and labour market data perform moving forward.

The market will closely watch the Fed's next policy statement on 20 September, as well as the updated economic projections and dot plot that show the expected path of interest rates.

Increasingly, interest rates markets are predicting at least one more rate increase. Unlike previous rate rises the equity markets continue to take higher interest rates in their stride. The previous concerns around what higher interest rates would do to the broader economy and company earnings seem to have dissipated.

2. It appears interest rates will stay higher for longer

It’s becoming increasingly clear that interest rates are likely to stay higher for longer. Ten-year interest rates in both New Zealand and the United States are reaching highs previously seen in October 2022. The 10-year interest rate – widely assumed to be the new ‘neutral interest rate’ – is now sitting just above 4.0%.

With an increasingly resilient economy, central banks will have no need to make drastic cuts to interest rates. As proof of this, drops in the interest rates previously scheduled in for late 2023 and 2024 are gradually being removed from forecasts.

Unfortunately, this is likely to be particularly bad news for mortgage holders, as 6%-plus interest rates could be the new norm for the medium term.

3. China just can’t catch a break

China's economic recovery continued to lose momentum in July: the official Purchasing Managers' Index (PMI) for manufacturing dropped for a fourth consecutive month, indicating contraction in the sector. The non-manufacturing PMI, which covers services and construction, also fell to the lowest level since December 2022.

China's GDP growth slowed to 0.8% in the second quarter, down from 2.2% in the first quarter. Consumer spending, the housing market and youth unemployment all showed signs of weakness. China unveiled a series of measures to boost domestic consumption on 31 July, but contrary to many investors’ hopes, they stopped short of announcing a major stimulus package.

Despite this, the Chinese share market performed well, delivering a 3.5% return for the month – though this had more to do with improving global risk sentiment than anything China-specific. This rally has prompted many European and US-based funds to withdraw investments from China. It will be interesting to see how the Chinese economy proceeds over the next six months and the impacts that has on the New Zealand economy.

4. Europe continues to outperform

The European recovery continues to outperform expectations, with manufacturing sentiment delivering better than expected outcomes. The ECB has sustained its interest rates increases, and it has become clear that the European economy and banking system can actually handle higher interest rates.

European markets keep pushing up, and interestingly the Euro Stoxx 50 has not delivered the same return as the S&P500 over the past three years – something unthinkable only a few months ago.

5. Japan gives up on its easing cycle

On 28 July, the Bank of Japan (BOJ) surprised markets by announcing a shift in its yield-curve control policy, lifting its cap on ten-year Government bond yields from 0.5% to 1.0%. Government bond yields climbed to around 0.57% after the announcement, the highest in nearly a decade.

With inflation currently running at 3.3% in Japan, the BOJ's decision has spurred speculation that they might be considering more significant alterations to Japan's ultra-low interest rates.

6. Commodity prices are pushing higher again

Oil prices have surged past recent highs, reaching $80 per barrel. This is driven by a unilateral decision from OPEC, led by Saudi Arabia, to cut oil supplies and push prices higher. The Saudis are worried about strong supply at a time when economies start to fall, which traditionally has led to drastic falls in the price of oil.

In the meantime, prices for wheat and other food commodities have spiked following Russia's withdrawal from a deal allowing Ukraine to export grain supplies through its Black Sea ports.

The bottom line

Amid these ever-changing global economic dynamics, maintaining a diversified KiwiSaver portfolio is crucial. Not quite sure where to start? Use our digital advice tool to create a personalised KiwiSaver portfolio that’s tailored to your individual needs and goals.

Further reading: