The Kōura Market Wrap for May

Table of Contents

The Kōura Market Wrap for May

8 Jun 2023

AI takes over the markets

The markets in May were all about Artificial Intelligence. A few months on following the hype of Chat GPT we are starting to understand what it can do for individual companies.

Global stock markets were very slightly down in the month, but the US tech heavy Nasdaq managed to post a very solid 6% gain.

In other news, economic prospects are starting to sharply diverge, the risk of a hard landing (read nasty recession) seems to be shrinking in the US while the growth prospects for Europe and China seem to be shrinking each and every day.

Here in New Zealand, we had Adrian Orr steal the show with a very definitive OCR announcement, boldly stating that interest rates have peaked and that we now have inflation under control.

A lot to go through, so let’s go through some of the detail:

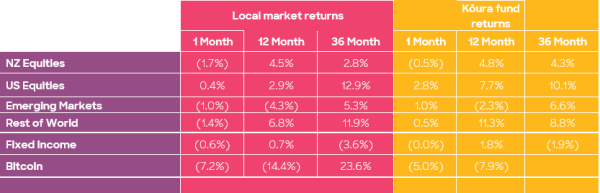

The Kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the Kōura funds invest in. Kōura returns are net of tax. The Kōura Carbon Neutral Crypto Currency Fund inception date was 23 May 2022. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ.

The AI craze has finally hit the stock market

3 months after Chat GPT became mainstream, investment markets have finally woken up to the possibility of what it can bring to company earnings.

Nvidia (the Chip maker) released Q1 earnings significantly stronger than expected and announced they expected Q2 sales to be 50% higher than expectations. Nvidia has come to dominate the production of Micro Chips for Artificial intelligence and as a result are now selling chips for over $10,000 compared to more traditional chips which were worth in the hundreds of dollars. The Nvidia share price has jumped almost 3x this year turning it into a trillion dollar company, one of only a handful in the world.

Nvidia is the most extreme example of this, but we have seen AI madness jump into every part of technology. Microsoft, Google, Apple and Alphabet are all expected to be huge beneficiaries of AI into the future and AI is expected to drive a surge in new products and earnings for all of these products. The AI craze is one of the big reasons why the Nasdaq has jumped 24% this year where the broader US market has only jumped 9%. In May alone, the Nasdaq jumped almost 6% whereas the broader US market was flat in the month.

The RBNZ appears to be leading the world again

On 24 May we saw the NZ Reserve Bank lift interest rates by 0.25% and very clearly state that they did not expect any further interest rate hikes, interest rates are expected to remain steady at 5.50%. This surprised the market with many economists predicting a 0.50% increase and guidance suggesting that we might need to go north of 6.00%.

The RBNZ decision was based on a few interesting observations:

-

They see the recent uptick in immigration as being temporary rather than longer term

-

They do not view the Government budget as inflationary as Government spending is expected to grow less than the broader economy

-

They do not see Cyclone rebuild picking up any time soon to drive the next level of inflationary spending

-

Commodity and shipping prices have fallen dramatically over recent months which will help reducing pricing pressure

While all of this was extremely disappointing news to the National Party (who were hoping that this announcement would confirm Grant Robertson’s economic incompetence) it was very welcome news to mortgage holders and everyday Kiwis who will be relieved to see mortgage rates and food prices start to wind decrease.

What’s happening with the NZ dollar? It seems to be all over the place...

Over the past 8 months we have seen the NZDUSD spot rate bounce between $0.55 and $0.65 cents. A very wide range of outcomes. The New Zealand dollar has two underlying drivers behind it, the fear factor, and the underlying economic prospects of New Zealand versus some of our trading partners.

The New Zealand dollar is often seen as a “risk currency” this means that when investors around the world are confident and willing to take risks then the NZD typically strengthens, though when things are bad in the world then the NZD is often sold off. That is great for NZ investors as it can prove to be a “natural hedge” against foreign domiciled investments that are priced in foreign currencies and also a boon for our export orientated economy as it makes our exports worth more. The bottom of the NZDUSD cross rate was at the same time as financial markets bottomed in October.

Secondly, we need to think about the NZ fundamentals versus the US fundamentals. The US economy continues to do well at the moment and there is increased nervousness around what will be happening in New Zealand.

In May we saw the sudden fall from 63.5c all the way down to 60c post OCR announcement largely because of interest rate expectations falling in New Zealand and increasing in the US.

We do not think this volatility will abate any time soon. Markets are still not yet sure on when inflation returns to zero, how high interest rates go or whether we are heading for a hard or soft recession. Once we have all of that sorted and the world returns to normal, we will have less volatility across all products.

China and Europe vs America, why so different?

May saw a sharp selloff across Asia and many of the European markets. The Shanghai Composite in China fell 5% and large European markets such as Germany, the UK and France were all in significant negative territory.

In China there is increasing worry around what escalating US tensions will do to their economy long term, not having access to critical US technology will be an impediment to their long-term growth.

This is all happening at a time when the economy has not delivered the stellar recovery that was expected post reopening. The Chinese economy will struggle to deliver the 6% growth that the CCP wants and expects, and to a certain extent needs.

In Europe the news appears to be turning even more sour. France and Germany are now expected to head for recession later this year and the UK is most likely currently in recession and is one of the few developed countries still battling double digit inflation.

This is all happening while US growth estimates continue to increase. A few months ago, most US economists expected a “hard landing” (read deep recession). But that has now softened, and most people expect a soft landing or no landing at all.

The key difference is the structure of the economies and the structure of the mortgage market. Amazingly, in the US when you take out a mortgage you typically take out a 30-year mortgage with your interest rate locked for 30 years. This means that the only people impacted by the higher interest rates are those that have purchased a house in recent times (last 12 months).

Europe and other markets have mortgage markets like New Zealand with fixed periods ranging from 3 years to a maximum of 10 years.

So where are we at?

It does appear that the fight against inflation is coming closer to winning than we initially thought. We have now seen the Australian, Canadian and New Zealand Central banks all claim that interest rates are unlikely to go higher as they are confident in the deflationary process. Though we are yet to see anyone fall back into the 2-4% inflation range which is necessary to call it a job done.

The US is the main outlier here, given the strength of their economy and job market it is unclear how much further the Fed will need to go with interest rates. Britain is the one massive outlier where inflation remains extremely high, though this appears to be a combination of economic structural issues (very inflexible labour market, difficult energy market) and also Brexit issues (food shortages due to border issues).

Markets are very positive right now because they see that the fight against inflation is almost over and the expected carnage that was meant to eventuate from the higher interest rates has not appeared. It is too early to say that we are in the next golden age, but there is a strong possibility that we might be.