The value of advice

The value of advice

11 Mar 2022

There are plenty of good financial behaviours people can make in order to maximise their KiwiSaver opportunity, but how much of a difference does getting advice make?

With advice being at the heart of Kōura we’re big believers that it plays an essential part in helping kiwis make the right decisions for achieving their KiwiSaver goals, whether it’s for their first home or retirement.

Advice allows for better financial decision making

In the 2021 ‘Value of an adviser report’ produced by Russell Investments (a large global asset manager with over $300 billion of assets under management), it was found that an advised client portfolio on average was 5.2 % per annum better-off than someone who didn’t receive advice in the same period.

Making up 2.0% of the 5.2% average was ‘Behavioural coaching’, which basically refers to a part of advice that teaches people about behavioural mistakes such as trying to time the market and pick the highs and lows. A very common KiwiSaver mistake is kiwis changing to a conservative fund because they are scared of a market crash, more often than not, this decision will end up costing the investor a significant amount.

Building up positive financial behaviours such as allowing yourself to be less swayed by emotions is critical in being able to achieve your end goal and an adviser is a great person to talk to each and every time you think about making a critical KiwiSaver decision.

People build better awareness and think harder about their outcomes

A recent report by Financial Advice NZ - ‘Better Behaviours’, looked at what some of the key differences between KiwiSaver members who have or haven’t received advice when making certain KiwiSaver decisions, with a focus on contributions and reviews - predictably, those who had received advice came out on top.

Understanding how much money you’re contributing and whether it will be enough to achieve your goal is a critical ingredient in building up your KiwiSaver savings. Not contributing enough makes it a lot harder to reach the first home or retirement goal you desire.

A lifetime of low KiwiSaver contributions will leave you high and dry when it’s time to hang up the boots at retirement. There is an unfortunate amount of kiwis who only contribute the default rate of 3% and the sad truth is that it’s nowhere near enough for a comfortable retirement or the first home you expect and it’s why getting this part right is so important.

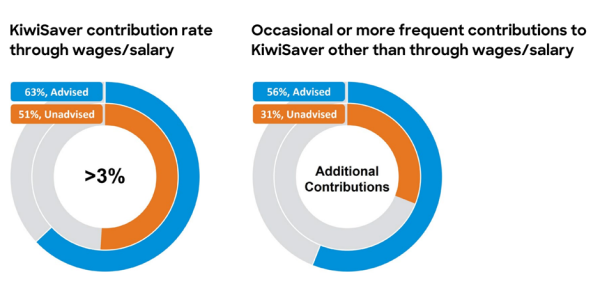

The difference advice can make with KiwiSaver contributions

Fig.1 KiwiSaver Advised vs Unadvised contribution stats | Financial Advice NZ

In the Better Behaviours report, it was found that both groups had high rates of KiwiSaver contribution rates (82% vs 72%) which is great. However, when it comes to making regular contributions, advised Kiwis are more likely to do so with contributions higher than the 3% minimum, with 63% paying 4% or higher compared to only 51% of those who are unadvised. They are also twice as likely to be making occasional or more frequent contributions to their KiwiSaver other than their wage/salary contributions at 56% vs 31%.

We attribute this to the fact financial advisors will ensure that clients are aware of what their KiwiSaver will give them (like the Government contributions match of 50c to every dollar up to a maximum of $521 per year. So, if you contribute up to $1,041 in a year, you will get an additional $521 of free money), allowing them to make more considered and informed decisions about how much they need to contribute to their KiwiSaver.

And before you say this is only because those with financial advice can afford it, we’d like to highlight that the report found the “marked difference in behaviour is seen across all ranges of personal/household income indicating that advice, and not income, is driving KiwiSaver contribution rates.” Showing that KiwiSaver advice is increasingly available to everyone!

The sad reality is there are hundreds of thousands of kiwis still shooting themselves in the foot by not having high enough contribution rates so it’s encouraging to see what difference some extra advice can make! (Whilst we won’t go into any further depth here, if you want to understand more about why KiwiSaver contributions are so important, you can check out this blog to learn more.)

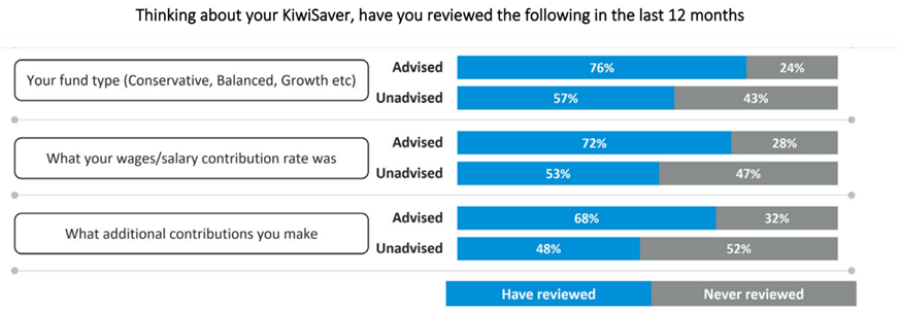

Advice compels you to spend more time and review your KiwiSaver

KiwiSaver is a 'set and forget' for most KiwiSaver members. The portfolio of funds selected at sign up is more than likely the same portfolio that a customer still has today. There is no appreciation that the portfolio needs to change and be reviewed on an ongoing basis to match your objectives.

So, the biggest value that advice brings to the table is that it doesn’t let you ‘set and forget’. A big part of staying on top of your KiwiSaver is making sure that you do regular reviews or check-ups in order to make sure everything is still functioning as it should be (think of it in the same way as your annual visit to the doctor or dentist).

Keeping that in mind it should come as no surprise that the better behaviours report found that advised Kiwis are more likely to be more proactive about reviewing their KiwiSaver compared to those who aren’t advised, whilst also being likely to make changes as a result of those reviews.

Fig.2 KiwiSaver Advised vs Unadvised review stats | Financial Advice NZ

Whilst some people are starting to take KiwiSaver more seriously there are still a whole lot (as this report shows) not getting it right, and that’s where securing quality KiwiSaver advice could make the difference between an okay retirement and a great one.

The take away

Kōura at its core is a digital adviser and whilst not quite the formal in-person adviser that the ‘Positive behaviours’ report refers to, we are firm believers that every Kiwi has the right to a good retirement, and a part of that for us is making sure we do our best to make advice accessible to everyone. We also recognise that some people prefer a combination of both human & digital advice and it’s why we offer an additional facilitator option (facilitators being the many awesome KiwiSaver advisors we partner with) for our customers.

There are still lots of kiwis out there who think advice is still only for the rich & wealthy, but this is no longer the case. Advice for KiwiSaver is available for everyone, if you want help with your KiwiSaver come and talk to us at Kōura or reach out to your life insurance or mortgage adviser.