What do low interest rates mean for you?

What do low interest rates mean for you?

16 Apr 2021

So you hear talk of interest rates in the news, especially right now as they sit at record lows. But what do they really mean for you? Here’s your guide to making the most of your money while interest rates are low:

Firstly, for those of us who don’t speak economics and finance (hello to most of us), here’s a super quick run-down or re-cap on how interest rates work. If you know your stuff, skip ahead!

You probably know that an interest rate is the amount of the loan that is charged to the borrower for being able to use the money being lent to them. Or the flip side, how much money you are paid for lending money to someone else (ie. a bank deposit). But how do they fluctuate?

Central banks or in NZ, the Reserve Bank of New Zealand (RBNZ), set something called the official cash rate (OCR). This basically means the interest rate that commercial banks and financial institutions will be charged for borrowing money from the RBNZ. When it’s cheaper for them to borrow money from the RBNZ, it’s cheaper for them to lend money to us! So these lower rates are generally passed on to us as consumers.

So essentially the OCR is a tool that the RBNZ has that enables them to increase or decrease interest rates in the economy. When interest rates are low, spending goes up, when they’re high, consumer spending decreases.

Okay cool, we get the OCR, but how do interest rates influence spending?

Interest rates have a direct impact on consumer activity and spending because when interest rates go down, the cost of borrowing becomes cheaper. For many people, this makes purchases on credit more affordable, such as home mortgages, car loans, and credit card expenses. Low interest rates may be a catalyst for someone to make a large purchase that they otherwise wouldn’t have, hence why low interest rates boost spending activity.

And it’s vice versa for when interest rates go up, the cost of borrowing becomes more expensive, so people generally tend to borrow and spend less. There you go, congrats on making it through interest rates 101!

So why are interest rates so low right now?

COVID-19 has ravaged economies, with the subsequent lockdowns and a change in the way we live equating to extra costs and lost revenue for businesses. To navigate the fallout, central banks all over the world, including our very own RBNZ, lowered interest rates to spur spending and facilitate the economic recovery.

On 16th March 2020 the Reserve Bank dropped the official cash rate (OCR) from 1% to a record low of 0.25%. They also indicated that they would look to keep interest rates at this low rate for at least 12 months.

When it comes to spurring spending, the recent Covid inspired drop in interest rates has worked; variable mortgage rates have fallen by 0.76% (from 5.26 % to 4.50 %) and fixed rate mortgage have fallen significantly further, which has led to a debt fueled consumption boom. For some people interest bills have halved, so they’re now topping up their mortgages to do a renovation, buy a bach, a boat or a car. It’s truly amazing the spending that is going on in New Zealand at the moment.

What low interest rates mean for your savings

While low interest rates encourage spending and benefits those looking to buy some big-ticket items, unfortunately for the keen saver depositing money into a bank account it means that they miss out on the benefits. Low interest rates mean you don’t get much return on investing cash in the bank, raising the question, should you put it elsewhere? (more on this later!)

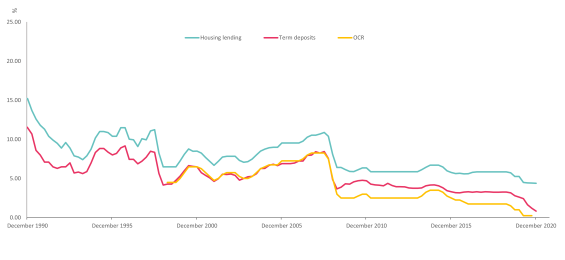

In the chart below, you can see that over the past 35 years, interest rates have tumbled. We’ve seen mortgage rates go from over 15% in 1990 to 4.39% and term deposits go from 10% in 1990 to below 1%. For someone with $100,000 of savings in the bank, in 1990 they took home over $10,000 from interest, today that same $100,000 would only return $830!

This lower interest rate means that investors and savers need to do two simple things, they need to save more, and they need to take on more risk. However, one other thing to keep in mind is that a major side effect of low interest rates is asset inflation. In this case, that means house prices and stock markets have ballooned, all driven by the low interest rates making debt really cheap.

What other investment options do you have?

There are typically three primary types of assets, term deposits (money in a long-term savings account), fixed interest (money invested in things like government bonds) and equities (shares in companies). Each type of assets has different benefits and potential drawbacks, let’s understand their differences a bit better.

Different types of investment and their risk and return profiles

As you can see from the table above, the three primary types of assets all have different risk and return profiles. Volatility is a proxy for risk, and it represents the most an asset is likely to move in a single year. For example, equities have the most risk, with an annualised volatility of 30%, meaning there’s a chance that they could go up or down in value by 30% in a single year.

Higher risk generally means higher returns. If that $100,000 was invested entirely in equities, the return is likely to be $5,500 per year, however you’d be exposing yourself to a significant amount of volatility. You should only be doing this if you can withstand a 30% loss in any given year.

So how do you choose what and how much to invest in? We’ve broken it down based on your life-stage:

I’m saving for retirement

Unfortunately, lower interest rates mean that we will need to save more for our retirements. Our money won’t work as hard as we’d previously hoped for. Markets are expected to deliver a return of 5-6 % over the next 10 – 20 years, significantly lower than the 11% that they have delivered over the past 10 years. So ultimately, you’ll need to save and invest more to deliver the same outcome, which makes investing in things other than a term deposit an attractive option.

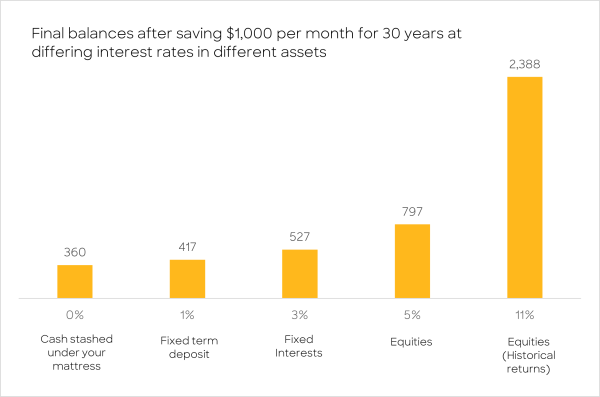

In the chart below you can see the impact of lower interest rates on investing. If someone invests $1,000 per month for 30 years, that person will have invested a total of $360,000 over that 30 year period. Let’s compare what that person could invest in and the kind of returns they could get. Here are so simplified examples:

- If they invested the full amount in a term deposit earning 1%, they’d have $417,000 invested by retirement.

- That same $360,000 invested in Fixed Interest with a 3% return would be $527,000 by retirement.

- Or if they invested it in equities for a 5% return, it would be $797,000 by retirement.

- And, just to compare with what returns on equities used to be, that same $360,000 when invested historically (before interest rates and the markets changed) would have returned around 11%, meaning their retirement nest egg could’ve been up to $2.4 million.

$797,000 sounds like a great sum towards your retirement, but it doesn’t mean you should go and throw everything into equities. You should ask yourself what level of risk you’re comfortable with, and let that help you to decide your asset allocation (the mix of investments you have). To take the guess work out of it, Kōura can help you navigate through this uncertainty by helping you build a personalised KiwiSaver portfolio based on your goals and risk appetite.

I’m already in retirement

If you’re retired, you may tend to have a large portion of your money in fixed income assets such as savings and bonds, because you require the certainty that you’ll get a set amount of cash flow for living expenses. Hence, term deposits and rental properties have traditionally been the favoured savings vehicles for retirees.

As a retiree you’re particularly affected by low interest rates, because your savings in the bank aren’t earning as much as they used to. Retirees who planned to retire on a nest egg or KiwiSaver might find themselves in a bit of a pickle as they quickly realise that their monthly income has dropped to a level lower than they originally budgeted for. Unfortunately, the answers to this is to spend less and/or to take on more risk. But how do you go about taking on more risk?

We believe that the traditional mantra of save your capital and spend your income needs to change. The traditional way of looking at things was if you retire with a $2million retirement pot, you should live off the income and not touch the capital. If properly executed, you would likely still have the $2million when you die. To do this though you need to invest exclusively in income generating assets of which term deposits used to be the easiest to invest in and understand.

However, with interest rates at all time lows, retirees now need to think about creating more diversified portfolios and spending a combination of the income and the capital growth. Most retirees are long term investors, therefore can withstand the volatility of the markets, if you expect to spend 4-5% of your retirement savings each and every year you shouldn’t mind whether it comes from capital or income, and this approach allows you to invest in higher risk assets such as equities.

I’m a first home buyer

As we mentioned earlier, low interest rates cause asset prices, like housing prices to go up. The reason for this is simple; low interest rates allow people to borrow more for less, increasing the demand for housing. According to REINZ, the one-year change in house prices over the year to Feb 2021 is 21.5%. While this is great for people who are already homeowners, it is at the expense of the first home buyer.

Unfortunately for first home buyers, they have fewer investment options to help them save up for a deposit. The most proven and time-tested way to build wealth over time is to invest in a well-diversified portfolio of stocks. However, this might not be the case for first home buyers as investing in stocks can be risky in the short term.

The generic KiwiSaver advice to people investing in a growth fund (largely made up of equities) is to have recommended 10-year holding period. For first home buyers saving up for a purchase in the next 5 years or even sooner, investing a high proportion of your portfolio in stocks is risky. The worst thing you want to do is sell when the stock market is down. If the market goes into a downturn, this could turn bad very quickly for your savings goals in the short term.

To diversify against market risk, one should instead invest in fixed income assets like bonds or putting money into a savings account. However, it will not do you much good as the current interest rate on savings is close to nothing.

So sadly, in terms of investment options for first home buyers, there aren’t a lot of options. In this situation, striking the right balance between growth and income assets is the right answer. Balancing risk versus rewards in the short term is crucial so that first home buyers will get the best returns with the least amount of volatility, to make sure that their financial goals are secured. Kōura will be able to help you navigate through this uncertainty by helping you build a personalised portfolio based on your goals and risk appetite.

Summing it all up

Essentially low interest rates mean that the difference between saving in a bank and investing in markets has widened significantly. This exaggerated difference makes it extremely important that you understand what you’re saving and investing for, and that you have an asset allocation that makes perfect sense for you. That way, how much risk you’re taking on is suited to your situation, and you’re taking enough risk to ensure that you don’t miss out on reaching your goals.

[hubspot type=cta portal=5033855 id=dfd6e00f-28a3-40bc-a3d9-fe025bfa70f8]