What to do with your first home deposit or lump sum of money while you’re still saving

What to do with your first home deposit or lump sum of money while you’re still saving

7 Oct 2021

What to do with your first home deposit or lump sum of money while you’re still saving

Putting your savings to work without putting your final balance at risk

Pulling together a lump sum of money for a house deposit, big-ticket item, or business venture is no easy feat. Depending on the amount you need and the rate at which you’re able to save, it could take years (and years) to reach the balance you need.

To keep that precious sum of money safe while saving a lot of people end up leaving it in a bank account. While a bank account is definitely one of the safest places for your money to be, it means it’s probably not generating much (if any) return and is subject to inflation. That means while your savings sit idle not generating returns, the cost of living continues to rise and your buying power is going backwards instead of forwards! (i.e. $1 today is worth less than $1 in the future)

So, what can you do with your lump sum of money so that it’s not just sitting idle, slowly depreciating in value? Here’s what you need to know!

Step 1: Understand your investment horizon and risk appetite

Your risk appetite is how comfortable you are with the ups and downs of the market. Along with your investment horizon, it’s a key factor in determining what types of investments you should have. If seeing your investment drop in value when the market dips makes you anxious, you probably have a low-risk appetite. Alternatively, if you’re comfortable with your investment value temporarily fluctuating, you may have a higher risk appetite.

Your investment horizon is a fancy way of say ‘the length of time until you want to use your money. For example, if you’re saving to buy a house in 6 years' time, you have a longer investment horizon, or if you are saving for a house in 6 months' time you have a shorter investment horizon.

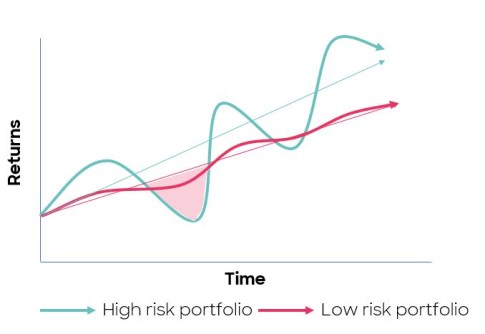

Your investment horizon is really important because when you are investing you have a choice of where to put your money. Investing in the share market can deliver great returns over the longer term, but could be a wild ride with some ups and downs. If you are invested for a long time, you can withstand the wild swings of the market because if there is a market fall, you will have time for the market to recover.

The shorter your investment horizon, the fewer risks you should take with your money (i.e. not investing in things like equities/shares, or other things that could quickly drop in value). That way you’re not putting your hard-earned savings at risk right before you need to use them.

The longer your investment horizon, the more risk you could take with where you invest your money because you have time to ride up the ups and downs of the market.

Here are some general investment horizon guidelines:

- 0-2 years - your portfolio should be mostly cash and fixed income assets

- 2-5 years - your portfolio could be an even balance of growth and fixed income assets

- 5-10 years - your portfolio could be largely growth assets offset by some fixed-income assets.

- 10+ years - your portfolio could be mainly high-growth with a very small amount of fixed-income.

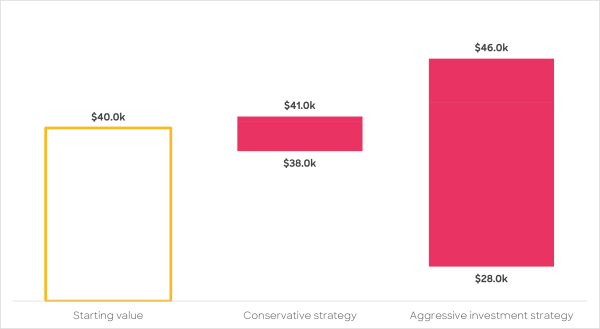

Putting this into context

The above table shows the possible returns of a $40,000 investment following a conservative strategy, vs $40,000 in invested following an aggressive strategy over a 1 year time period. The conservative strategy assumes 100% fixed income assets. Aggressive assumes 100% growth assets.

You can see here the impact of being in an aggressive investment portfolio vs a conservative/defensive portfolio. The conservative portfolio is unlikely to have a huge amount of upside but at the same time not much downside. Whereas an aggressive portfolio might have a much higher upside but a much lower/bigger downside. The question to ask yourself is - what do you prefer? Do the potential losses of an aggressive portfolio outweigh the lack of potential gains of a conservative portfolio? When investing, short-term investing in the markets is not materially different from gambling, you are just hoping a market crash doesn’t happen before you need to get your money out.

Step 2: Put your money to work

It’s time to do something with your lump sum of savings! Here are some of the options you have and their varying risk levels. Remember to consider both your investment horizon and risk appetite when choosing where to invest your savings. You might choose to diversify your investments and spread your money (and your risk) across a few options.

KiwiSaver

If you’re saving for your first home and are planning on using your KiwiSaver balance to help with your deposit, then you’ll want to make sure you’re in the right KiwiSaver fund. If your investment horizon is short, then a Conservative fund would be a safer option to protect your balance from market fluctuations. If you have a longer investment horizon, a Balanced or Growth portfolio could be an option, but you should understand the risk you’re taking before switching to a higher growth fund.

The traditional KiwiSaver fund options are limited to 3 different types, Conservative, Balanced and Growth, and it can be hard to know what ‘fund’ best suits your current situation (if one of them even suits you at all).

That’s where we come in! kōura’s digital advice tool builds each client a custom KiwiSaver portfolio (i.e. instead of a ‘fund’ you get a bespoke set of investments), that suits your investment horizon and risk appetite. Each year you get closer to withdrawing your money, Kōura automatically recommends slight changes to your KiwiSaver portfolio to ensure you’re not taking on too much risk. Check out the free tool for yourself.

Bank/long-term deposits

Term deposits are bank accounts that pay you a little more interest than normal savings or current accounts in exchange for you agreeing to lock up the money for a period of time. You can get term deposits for anything from 30 days out to three years. A term deposit is a lower-risk investment option which means you’re still generating a small return on your savings (and are therefore likely to be off-setting inflation).

Interest.co.nz has a good summary of term deposit rates for you. It’s a good idea to stick with the banks rather than the credit unions or finance companies as the banks will be a safer investment for you.

Managed Funds and Shares

This is the highest growth and risk option of all the ones we’ve mentioned. It would be suitable if you have a long investment horizon.

If you choose to invest in managed funds or shares, you’re investing in the stock market. Managed funds usually have slightly less risk than individual shares because you’re investing in a group of companies rather than just one. If one company within a managed fund of 100 companies performs badly, you’re also invested in 99 others that can offset the bad performance.

If you’re invested in an individual company and they do badly, there is no safety net to fall back on and your investment will drop in value. So while it might be tempting to put your money in a few of your favourite companies (like Tesla, or Apple), this would mean you’d be taking on a lot of risk. Instead, why not look for a fund that includes some of your favourite companies?

Step 3: Review your investments and make adjustments

Make sure you check back in on your investments and re-adjust your strategy as your investment horizon shortens and you get closer to your goal! That means should start to de-risk your portfolio by rebalancing it to have more conservative assets (like cash, bonds, and bank deposits).

And if you’re nearing the end of your investment horizon but are tempted to stay invested in riskier assets in hopes of generating higher returns just think: would you rather play it safe and have an extra +10% for your savings, or risk losing -30% or more in the lead up to your purchase?

It's okay to be a little overwhelmed at first, but as long as you set yourself up with the right strategy based on your specific goals, you’ll find that your first home is closer and more achievable than ever before!