Why does a personalised KiwiSaver portfolio matter?

Why does a personalised KiwiSaver portfolio matter?

1 Jun 2021

What does a personalised portfolio really mean for you and why is it important?

The most common misconception is that KiwiSaver is a set-and-forget product that you never need to look at again after making your first fund choice. This means most people are sitting in funds that aren't right for their financial goals.

But what’s wrong with the way most KiwiSaver providers set up their funds?

Most KiwiSaver providers offer 3 different funds; Growth (higher risk), Balanced (mid-level risk) and Conservative (lower risk). And usually, you choose for 100% of your money to be in one fund (e.g. 100% Conservative) or split your money to be 50% in one, 50% in another (e.g. 50% Growth, 50% Conservative).

The problem with the traditional KiwiSaver model is that it’s inflexible and doesn’t take your own personal financial timeline and risk appetite into account. Let’s look at some examples of how this model can impact your long-term financial goals:

Using your KiwiSaver for your first home

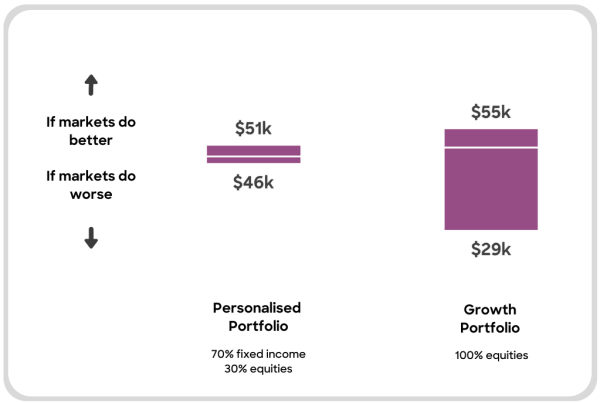

Rachel is planning on buying her first home within the next 2 years. She currently has $35,000 in her KiwiSaver which is a critical part of her first home deposit.

Rachel is planning on buying her first home within the next 2 years. She currently has $35,000 in her KiwiSaver which is a critical part of her first home deposit.

If she lost 30% of her precious first home deposit due to a market downturn (which is expected to happen to a growth fund every 5-10 years), it would seriously delay her house purchase or move her from a 2 bedroom townhouse back to a 1 bedroom apartment. So Rachel needs to maximise returns, whilst making sure the balance never falls too far.

So while a growth portfolio could return a slightly higher overall balance of $55k for her, if markets were to do badly, Rachel could risk only having $29k when she comes to withdraw her KiwiSaver and purchase her first home.

We would build her a KiwiSaver portfolio with a 30:70 ratio of fixed income (lower risk) and equities (higher risk), meaning Rachel wouldn't be risking too much of her balance if markets were to do worse, though still gives her the opportunity to grow her balance before she withdraws it.

Rachel needs to consider what level of risk she's willing to accept, and how important her KiwiSaver balance is to her first home deposit. If she's not comfortable potentially ending up with only $29,000, then she'd be better off choosing the personalised portfolio. Her personalised portfolio is risk-adjusted to suit her short timeline, while still aiming to grow her overall balance.

Saving for retirement

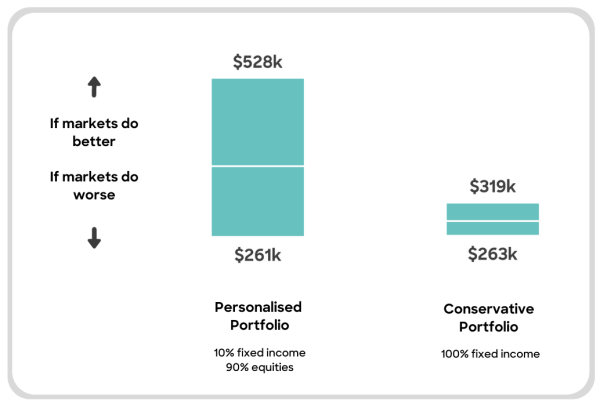

Marcel is 45 and is currently saving for retirement with a $50,000 KiwiSaver balance. He is relying on his KiwiSaver to help fund the retirement he's dreaming of.

Marcel is 45 and is currently saving for retirement with a $50,000 KiwiSaver balance. He is relying on his KiwiSaver to help fund the retirement he's dreaming of.

Marcel is a very long term investor and should expect to see through a few market cycles (the ups and downs). So if he is invested predominantly in equities (growth assets) his KiwiSaver balance will fall when the market turns, though in time it will recover. Despite the large ups and downs, this will give him a much larger investment balance for his retirement.

A conservative portfolio means Marcel has a very low risk of losing any of his KiwiSaver balance if the markets do badly. However, it also means he would miss out on a lot of potential returns, with the most he'll have at retirement being $319k.

Plus, with a personalised Kōura portfolio, as he gets closer to retirement, Kōura will recommend slight changes to his portfolio that slowly lower his risk, to ensure he retires with a healthy KiwiSaver balance.

To summarise

While it's tempting to chase high returns, or (if you're risk-averse) take the safest route, your KiwiSaver fund choice doesn't have to be all or nothing. By building a personalised portfolio with Kōura, your KiwiSaver will be right where it should be for you to reach your goals. And, if you want to, you can still build your own portfolio to suit the level of risk you're willing to shoulder - with the added benefit of Kōura conducting an annual review and making recommended updates to your portfolio mix.