Your nest or your nest egg, what comes first?

Your nest or your nest egg, what comes first?

25 Nov 2019

Deciding between paying the mortgage or building your retirement nest egg is tough - what do you prioritise & how?

A large proportion of New Zealanders are dependent on their property values to fund their retirement. However, a report by the Commission for Financial Capability in 2019 revealed that of those aged 50 – 65, only 38% are mortgage-free and the number of people entering retirement with freehold homes has been declining for decades. Couple this with recently released research from Westpac Massey Fin-Ed Centre that shows that if a couple wants a ‘choices’ retirement in a major city, they’re going to need a lump sum of around $787,000 to survive.

So do you focus on becoming mortgage-free or do you focus on retirement planning? Is it better to first become debt free – a hard task given the average Kiwi now has a mortgage of at least $400,000 – and then worry about retirement? On the other hand, there’s the cost of waiting to invest. Thanks to the joys of compound interest, a dollar you invest today has more value than a dollar you invest five or 10 years from now. That's because it will be earning interest—and the interest will be earning interest—for a longer period of time.

The answer to this dilemma lies in the basic math of in versus out. You want to focus on paying off debt if it’s likely to cost you more in interest than you might otherwise earn through investing. And you want to focus on investing if you think it’s likely to earn you more than you’d otherwise pay in interest.

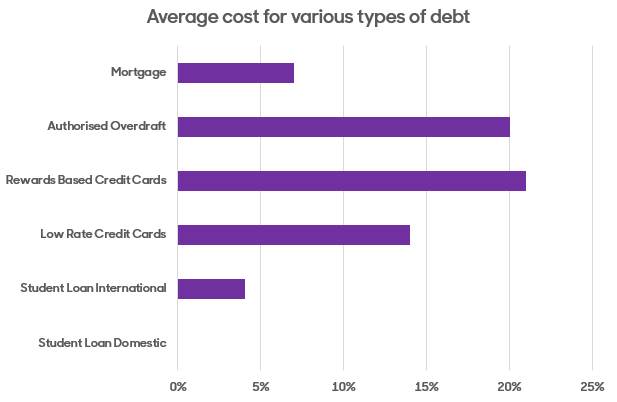

As we can see, the average cost over the past 10 years for a mortgage has been about 7% which is lower than overdrafts and credit cards. Also, since a domestic student loan accrues no interest, you can continue paying this at the minimum level for as long as it takes.

Now let’s compare this to the average KiwiSaver fund returns. The latest report released by Morningstar on KiwiSaver schemes suggests that over a period of the last ten years, the average Growth fund has given investors an annualised return of 9.9%, followed by an 8.2% return for Balanced funds and 6.2% returns for Conservative funds.

Effectively this means if you’ve invested your KiwiSaver in a growth fund, you have earned more in returns than you would have paid in interest on your mortgage.

But, a growth fund is not appropriate for everyone, and not all funds perform the same in the long term. The above returns while the great need to be viewed with a grain of salt as we have been in an unprecedented 10-year long bull run where the capital markets have been growing each year significantly. Going ahead, it’s unlikely we will see such strong performance repeat in the next ten years at least.

Life too is not all black and white. In between paying down the mortgage and saving for retirement are a bunch of other expenses that may come up or life goals you may wish to achieve like long-term travel as a family or saving up for your kids’ education.

Our Suggested Priorities

First, maximise the free money.

You may already know that if you contribute to your KiwiSaver balance, your employer is liable to match your contributions up to 3%. On top of this, the government also matches 50c to every dollar you contribute up to a maximum of $521/year. Assuming an average salary of $70,000 for a 30-year-old, an annual 3% contribution before tax equals to approximately $2100*. However, when you account your employer and government contributions into the picture, you are actually saving up $4621 into your nest egg, which is essentially double the amount!

Now compare this to stopping contributions and putting the same money into your mortgage. Not only will you first be taxed on this $2100 which means you have less toward your mortgage, but you also miss out on the free money from your employer and the government which could have made a significant difference to your final retirement pot.

So, even if current mortgage rates rise to 7% (the rate at which the bank calculates your mortgage affordability), you’re still better off putting in at least a 3% KiwiSaver contribution because the pool of money that you can throw at your retirement will be higher than the one you can throw at your debt, making the former more effective.

Next, get rid of all consumer debt.

Consumer debt is any debt aside from a mortgage and student loan that you’ve taken on to fund travel or new purchases or unexpected expenses either through an overdraft, your credit card or the various hire purchase providers that are available.

Unlike your domestic student loan, which is cheap, the average credit card charges 20% on any credit you roll over past your bill cycle. And, while hire purchase on companies like AfterPay, Q Card etc. may seem like great deals, they often make their money through various hidden fees and by continuously enticing you to buy things you don’t really ‘need’.

Overall, the interest on consumer debt is at least 3 – 5 times of what you pay on your mortgage or what you’re likely to get in investment returns from KiwiSaver or elsewhere. Which is why it makes sense to either pay this off completely and ensure you’re able to pay off your credit card bills in full before you turn your focus back to the nest v/s nest egg question.

Now get on comfortable terms with your mortgage.

While mortgages may be cheap right now at 3.5%, this may not always be the case. And, if you calculate the interest, you pay over the lifetime of a 30-year mortgage you will be shocked to learn that it equals to almost the original price of your home, if not more! Making extra repayments not only helps you reduce the term of your loan but helps you get comfortable with your mortgage.

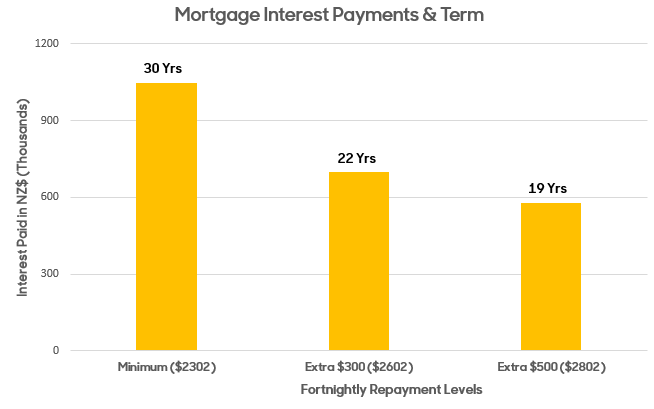

Assume you had a mortgage for $750,000 over a 30-year term which you got into at age 35. Paying the minimum amount would mean that you are paying a mortgage until you retire and you would have paid almost $1,000,000 in interest, which is almost 125% of your original purchase price*.

Now compare this to making an extra repayment of $300/fortnight. Not only does doing this bring your term down to 22 years – giving you a time of 8 years (likely when you're earning your highest salary) to save up but also means that you pay about $690,000 in interest repayments – a figure that should be offset by the equity you have been able to build up in the property.

The best time to make these repayments is in the first 10 years when most of your ‘minimum payment’ is going toward interest. Whatever extra you put in during these years directly reduces your principal and paying down your principal early means your savings get compounded over time.

However, remember that you don’t want to focus on your mortgage to the exclusion of everything else primarily because when invested properly your KiwiSaver has the potential to give you higher returns than what you’re paying in your mortgage.

And now you save, save, save

Majority of Kiwis are currently only contributing 3% to their KiwiSaver account. However, research shows that this will only yield them an income of 53% of their current take-home salary as compared to the international standards which say you need to ensure your savings replace at least 70-100 % of your existing income.

Building up your nest egg beyond the minimum may not be possible immediately. However, it is certainly possible to focus on this when you get an increment or promotion and the trick is to increase your contribution before your new salary hits the account. This way, you will never notice the ‘missing money’ and the future you will be very, very happy. If a regular increase in your KiwiSaver contribution is not possible, you can also review your insurance premiums each year, renegotiate with your power and broadband suppliers annually and make other small tweaks to build up a small pool that you put in as a voluntary contribution annually.

Conclusion

At the end of the day, any money you’re putting toward debt or investing is a step in the right direction. Your priorities may change as your life changes, so let the math tell you which one to focus on first. It’s also important to keep nurturing your KiwiSaver balance and ensuring you’re in the right type of fund as that has the biggest impact on your final retirement pot. At Kōura, we believe that everyone should be able to access free advice for their KiwiSaver investment so they can make smarter retirement decisions and fully understand their impact, which is why we design a KiwiSaver portfolio that's completely customised to you. Check it out now!

[hubspot type=cta portal=5033855 id=fa1b6a4c-f6e7-4d5f-8361-86a4b53afd00]

*Assumptions: Mortgage repayments have been calculated basis a lifetime mortgage interest rate of 7% for a fixed term NZ$750,000 mortgage. Calculations for 'free money' are done on the assumption of employees holding a full-time role where they are not on a total remuneration package. These amounts will vary for self-employed people, temps and contractors.