5 common KiwiSaver mistakes and how to avoid them

5 common KiwiSaver mistakes and how to avoid them

27 Oct 2021

5 common KiwiSaver mistakes and how to avoid them

Getting your KiwiSaver sorted and setting yourself up for the first home or retirement you're dreaming of doesn't have to be difficult. To make it even easier we're running through 5 common KiwiSaver mistakes that a lot of Kiwi's unknowingly make, and how to avoid them!

1. Not contributing enough to your KiwiSaver account

The contribution default rate for KiwiSaver is set at 3% but you can choose to contribute 4%, 6%, 8%, or even 10% of your pay, and while contributions to KiwiSaver are typically done through your pay, you can also make extra voluntary payments to your provider.

A lot of Kiwi's contribute the default 3% (plus their employers 3%) and assume it will be enough for a comfy retirement. However, the reality is that most Kiwi's need to be contributing around 10-12% for a comfortable retirement. That's because research suggests most people need somewhere between 70-100% of their current income when they retire, because contrary to popular belief, most people end up spending the same if not more when they first retire due to the extra time on their hands.

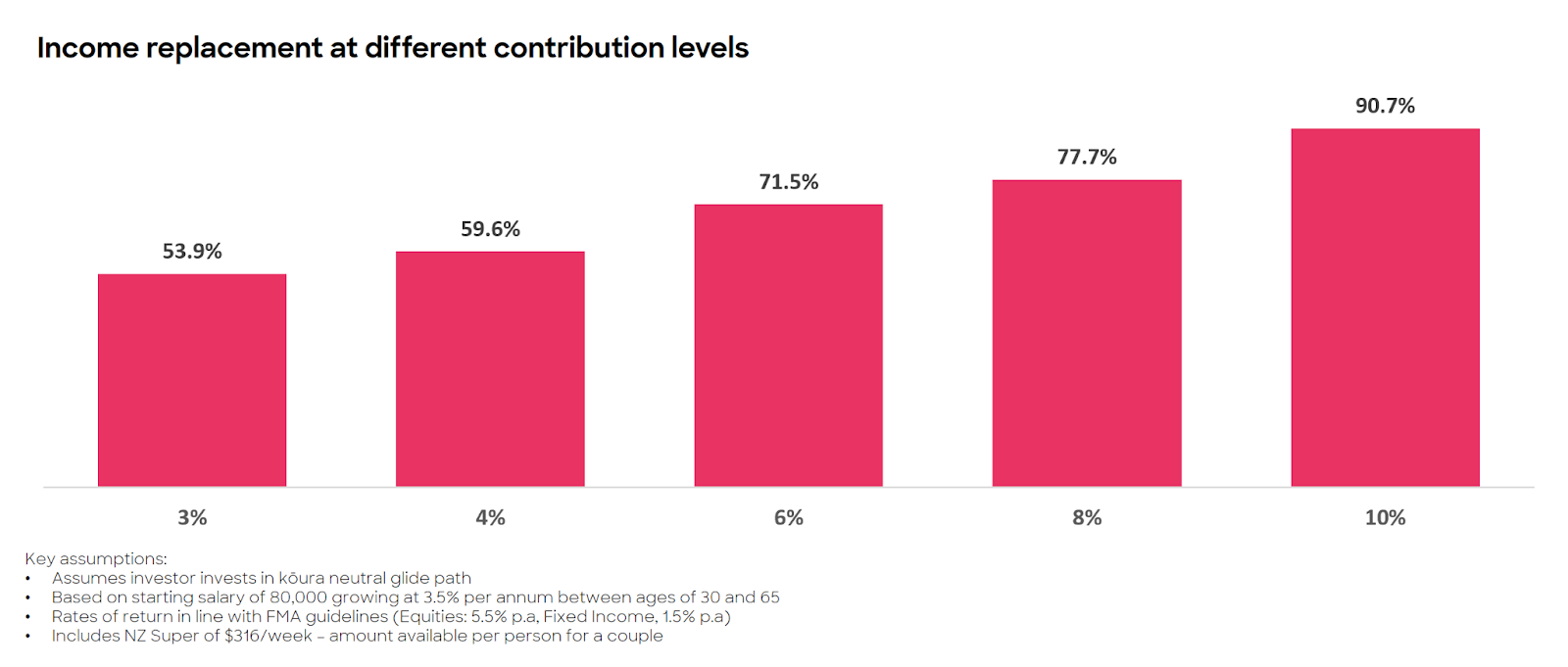

Let's see what different contribution rates would give someone aged 30 on an $80,000 salary by the time they reach retirement.

The chart below shows that with a 3% contribution rate, they'd have a weekly retirement income of about 54% of their usual weekly salary - an almost 50% cut in weekly income would be quite a lifestyle adjustment. Whereas you can see that an 10% contribution rate would make their weekly retirement income 90.7% of their pre-retirement salary and which would make for a far more comfortable retirement!

Contributing 10% of your salary to KiwiSaver might seem high, but compared to international levels it's still considered low. Over the ditch, Aussies contribute a minimum of 10%, while other members of the OECD (Organisation for Economic Co-operation and Development) like Iceland contribute a minimum of 15%.

The above chart assumes an investor invests in kōura neutral glide path. It's based on a starting salary of $80,000 growing at 3.5% per annum between ages of 30 and 65. Rates of return in line with FMA guidelines (Equities: 5.5% p.a. Fixed income, 1.5% pa). Includes NZ Super of $316/week - amount available per person for a couple.

The main takeaway here is to think about how much you’re contributing and whether it's currently enough to give you the retirement you want. If it's not and you can afford to up your contribution rate, your future self will thank you for it! So make sure you:

- Check how much you're currently contributing

- Calculate how much that contribution rate will give you by the time you want to withdraw your KiwiSaver balance (Kōura's digital advice tool can help with all of the calculations!)

- Adjust your contribution rate by informing your employer

2. Choosing the wrong KiwiSaver fund type

68% of Kiwis consider KiwiSaver to be a very important tool for their retirement. Yet, we don't realise the importance of getting it right. A 2019 survey done by Kōura found that less than half of people are sitting in the type of fund that's right for their risk appetite and objectives. That's a lot of people not making a decision (or making the right one) and it could end up costing them a lot.

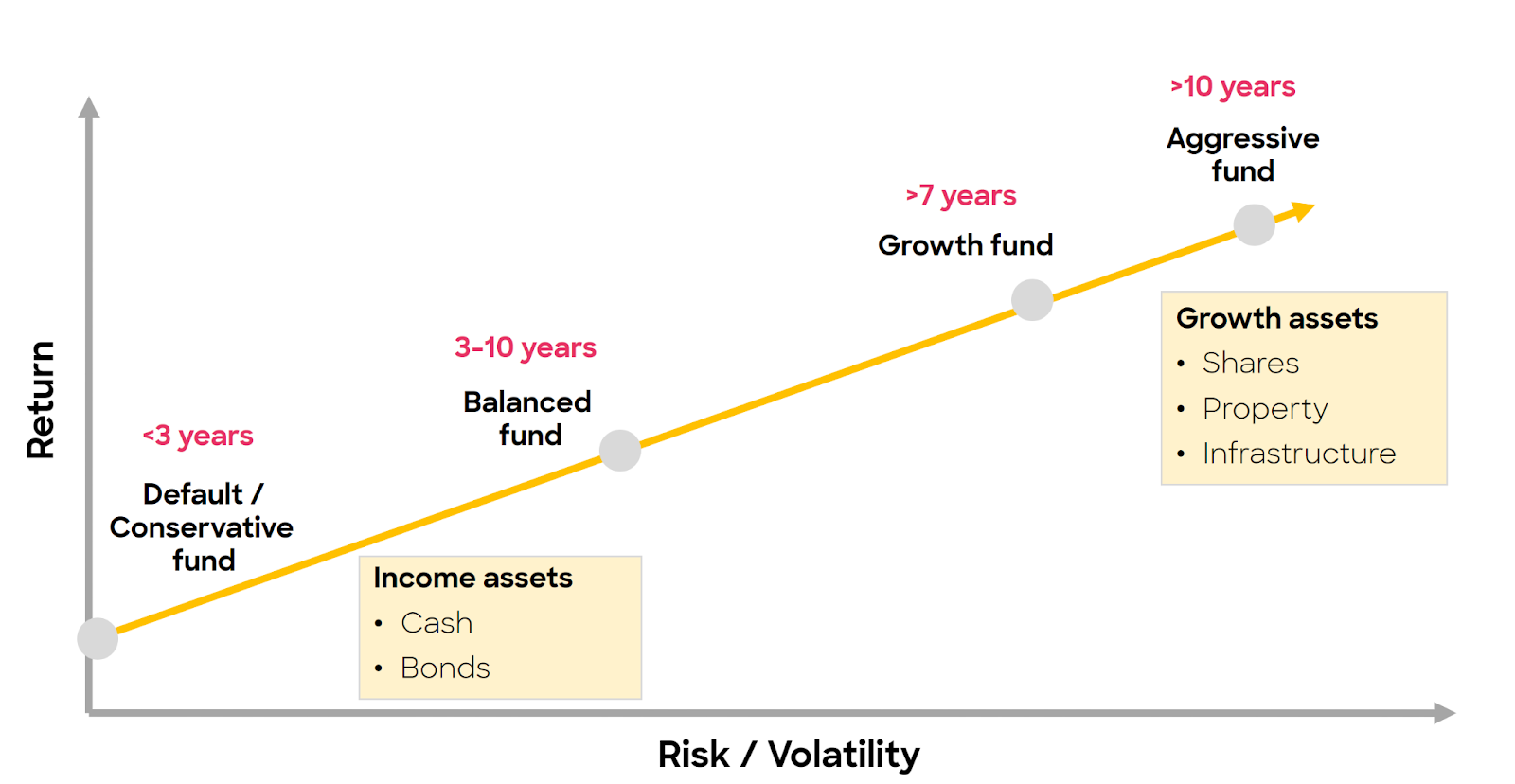

When you put your money into your KiwiSaver you're investing it, and where it is invested depends on the KiwiSaver fund type that you're in. The most common KiwiSaver funds are Conservative, Balanced, and Growth - with each fund type being made up of different kinds of investments (assets) that have different levels of risk and potential returns.

For example, Growth funds invest more money into assets like shares, real estate and infrastructure, while Conservative funds invest more in fixed income products like bonds and bank deposits. Growth assets will typically be more volatile (have more ups and downs), but they’ll usually deliver higher returns over the long term, and fixed income assets have lower risk (less ups and downs) but will generally have lower returns.

When deciding what fund type is right for you, you should consider your goal, your risk appetite (whether ups and downs in the market make you uncomfortable or worried), and your investment horizon (the amount of time your money will be invested for until you reach your goal).

As a general guide, the longer your investment horizon, the more risk you can take as you have time to ride out the ups and downs in the market. Whereas the shorter your investment horizon, the less risk you should take so that you can protect your investment from dropping in value if the markets underperform right before you need to withdraw and use it. You can see an example of this in the graph below.

To understand even more about risk and return and how you should think about it for your KiwiSaver portfolio, you can check out our blog on understanding risk with your KiwiSaver.

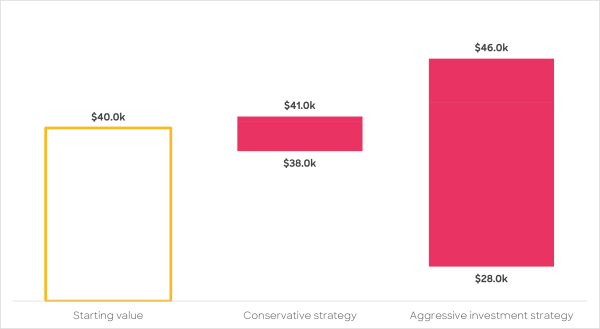

Let's take a look at someone who plans on withdrawing their $40,000 KiwiSaver balance as part of their first home deposit in 1 year's time, and what happens to their balance if they choose a conservative approach or a higher growth, aggressive approach:

The above table shows the possible returns of a $40,000 investment following a conservative strategy, vs $40,000 in invested following an aggressive strategy over a 1 year time period. The conservative strategy assumes 100% fixed income assets. Aggressive assumes 100% growth assets.

You can see here the impact of being in an aggressive investment portfolio vs a conservative portfolio. The conservative portfolio is unlikely to have a huge amount of upside (they might only gain an extra $1K) but at the same time not much downside (they could lose $6k).

Whereas an aggressive portfolio might have a much higher upside ($6K) but a much lower/bigger downside ($12K!). In this situation, seeing as their investment horizon is very short (only 1 year) we'd recommend a more conservative strategy to protect their final balance. However it's up to the individual to decide what they prefer. Do the potential losses of an aggressive portfolio outweigh the lack of potential gains of a conservative portfolio? When investing, short-term investing in the markets is not materially different from gambling, you are just hoping a market crash doesn’t happen before you need to get your money out.

Here's your checklist of things to consider when choosing your KiwiSaver fund:

- Decide what your investment horizon timeline is (how long until you reach your goal)

- Learn and understand what your risk appetite is (have a read of the blog mentioned above)

- Talk to your KiwiSaver provider and go through your portfolio to find if you’re still in the right fund

- OR use Kōura's digital advice tool and we'll suggest a fund type based on all of your above information

3. Not considering KiwiSaver fees

KiwiSaver fees can be confusing and are notoriously hard to compare because not all providers follow the same fee structure. Some charge a set % based on your KiwiSaver balance plus an annual management fee. Some include extra fees based on how well your investments perform. And some charge monthly instead of yearly. So what should you consider?

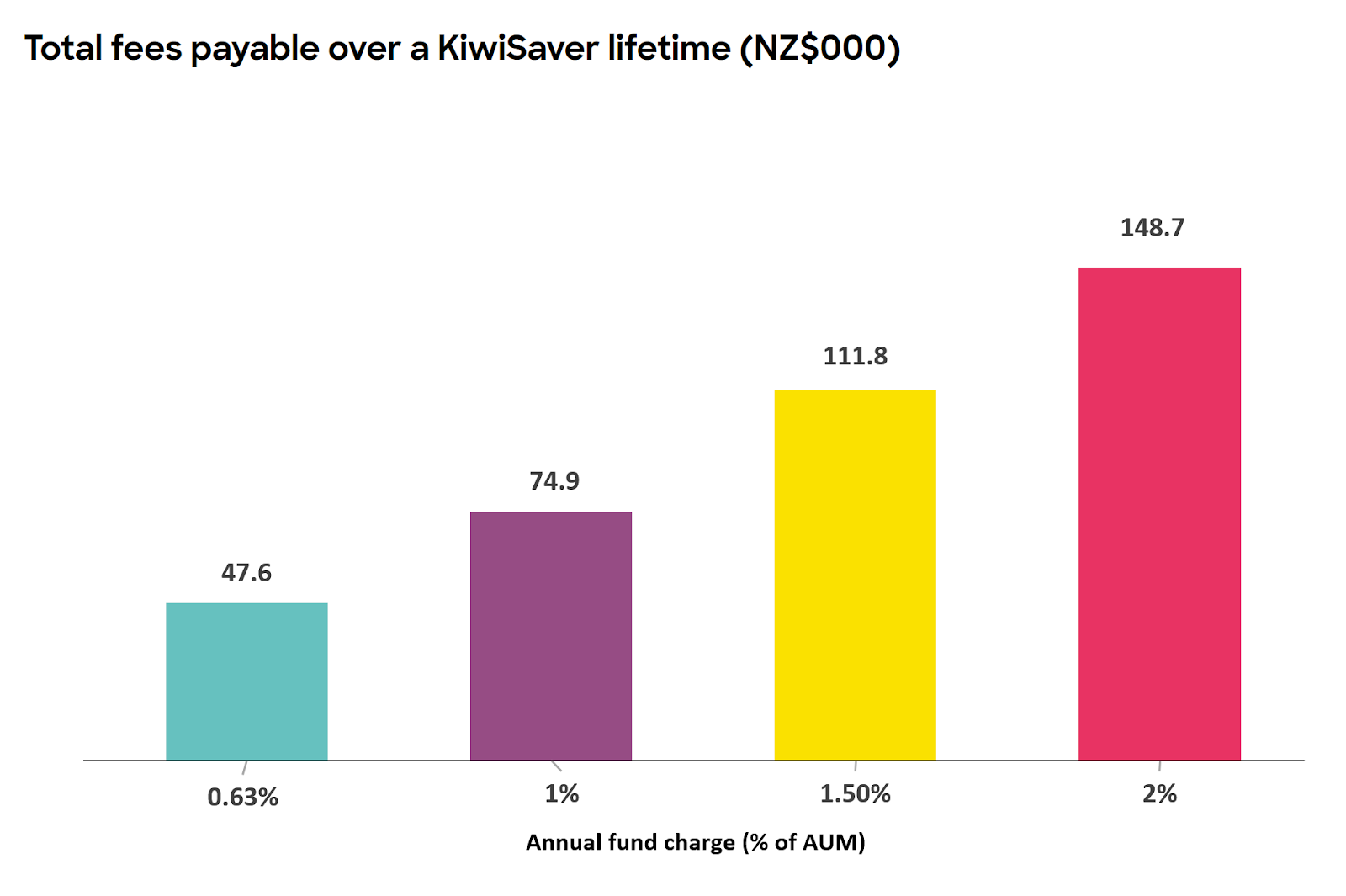

The biggest thing that we think really matters when it comes to KiwiSaver fees is the ‘after fee performance’. Let us explain. If you’re in a fund that has high fees and it's doing really well, should you really care that you're paying a lot since you're also making a lot? Well, the thing is, it's widely known that funds very rarely outperform the market in the long run, and therefore your high fees don't matter so much right now while your returns are also high, but over time when that great performance inevitably comes to an end, you'll still be paying high fees. Over a 10 year period of time, fees are likely to make the greatest difference in returns than anything else.

Looking at the above table, you can see that the level of fees someone will pay over their lifetime is no insignificant sum, and so a KiwiSaver provider who charges over 1% in fees will need to need to deliver much higher returns than a provider charging lower fees to not put their client at a disadvantage. To make matters worse, there's currently very little correlation between high KiwiSaver fees, and high returns, which means most people are simply paying too much for the level of service and returns they're getting.

A good thing to do is to take a look at your current provider fees and see how they stack up against the others in the market. And while fees aren't the only thing to consider when choosing a provider, they are important.

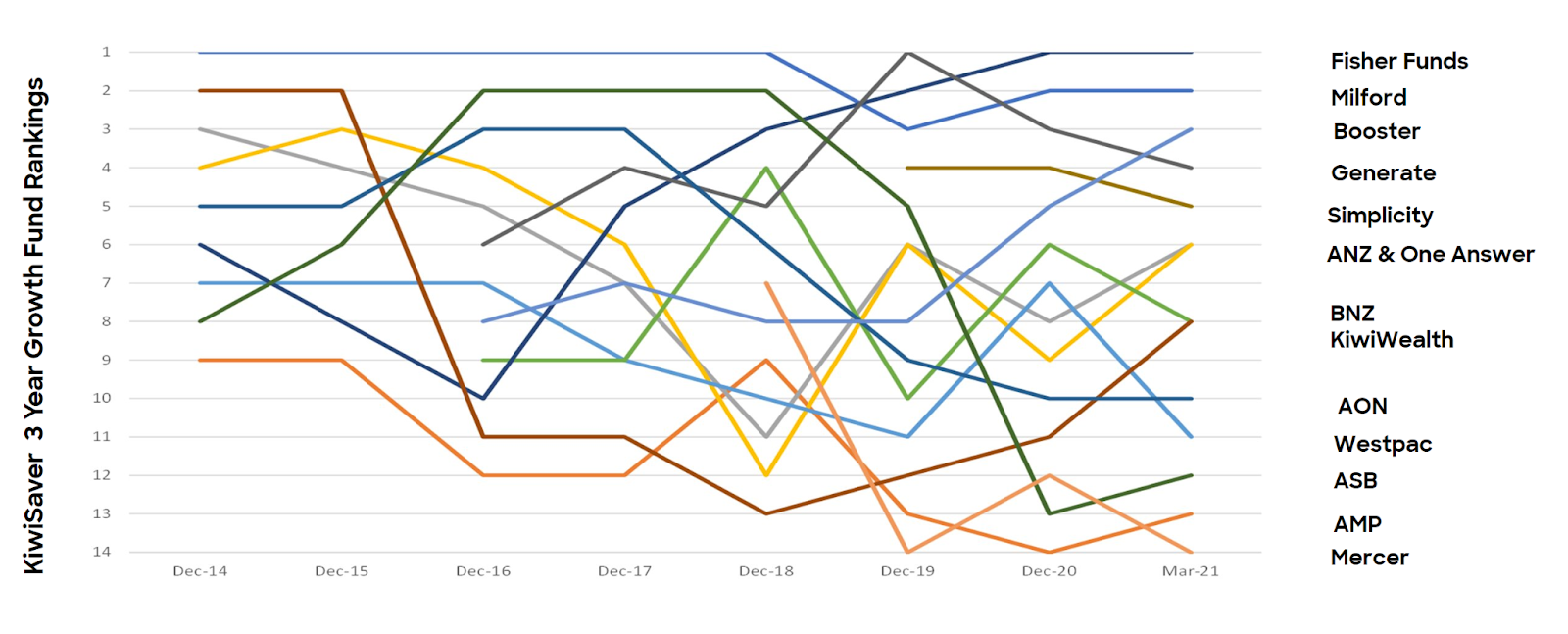

4. Choosing a fund based on historical returns

The number one rule in finance is that past performance does not equal future performance. Which is another way of saying that funds that perform well historically, rarely perform well in the future. What are we trying to say? That choosing a KiwiSaver provider or fund type based on historical returns isn't the best way to choose a KiwiSaver provider, because predicting when a fund will outperform is almost impossible.

The chart above may be confusing and look strange but that's the point. What is being shown here is that there are lots of lines that have periods that are up before then dropping down and vice versa. The chart is showing the performance of various KiwiSaver schemes, and what it tells us is that past performance probably isn’t the best indicator for how something is going to perform in future.

Research out of the US shows that less than 15% of funds that are top quartile in a 5 year period are then top quartile in the next 5 year period (i.e. the ones that were the best in one 5 year period, were no longer the best in the next 5 year period). This is because investment houses & fund managers will choose a strategy that will work in one set of market conditions for a few years - but when the market conditions change that strategy unwinds.

However, there are some KiwiSaver schemes that perform consistently poorly, and if that's the case it's not a bad idea to weigh up your other options, while keeping in mind that the top-performing schemes now will most likely not stay that way forever.

So what should you do?

It's really important to recognize that past performance on its own should never be used as something to make a decision, especially when it comes to picking your fund type. So instead, some things to ask yourself would be: How did I pick the fund I'm currently in? Has it consistently been performing poorly? What other things are important to me in a KiwiSaver provider and does my current provider offer or do those things?

5. Not reviewing and staying on top of your KiwiSaver

No matter how fit you are or aren’t, we all know that it’s valuable to drop by your doctor’s office and get an annual health check-up to make sure everything is working as it should be. These check-ups are important for early detection of problems that might have cropped up, or at the very least just gives peace of mind that you’re on the right track.

This idea applies to your KiwiSaver as well, a critical thing to remember is that all these decisions are really simple to think about, and stay on top of. It’s important to note that KiwiSaver is not a ‘set and forget’ product. So treat it like an annual ‘KiwiSaver’ health check - ask questions like:

- Are you still in the right fund type?

- Does it match your objectives and your risk tolerance?

- Do you need to change your contribution rates?

- Are your fees reasonable and in line with what's happening in the market

- What will your KiwiSaver give you for your retirement or first home?

It’s really important to make sure that you’ve made those simple decisions, and returning for an annual check-up makes sure those decisions remain valid. But it's okay to be a little overwhelmed at first, just as long as you set yourself up with the right strategy based on your specific goals, you’ll find that your goal is closer and more achievable than ever before!

Kōura also has a great set of tools to help you understand your KiwiSaver account and make sure it suits your needs, plus we conduct an annual KiwiSaver health check for you and send you our recommendations! Review your KiwiSaver plan here.