Do I need to increase my KiwiSaver contribution rate?

Table of Contents

Do I need to increase my KiwiSaver contribution rate?

25 Aug 2022

Do I need to increase my KiwiSaver contribution rate?

How much will your current contribution rate give you for your first home or retirement? Not quite sure? Check today to get your financial future on track.

In this guide, we’ll delve into and look at these questions:

1. How much do you need from your KiwiSaver?

2. Will your KiwiSaver contribution rate get you there?

3. Another reason to contribute more? Compounding returns

How much do you need from your KiwiSaver plan?

For the TL;DR (too long; didn’t read) power users and everyone else, below you will find some useful steps that will help you along the way:

-

Figure out how much you’ll need for the goal you have in mind: This is where you need to begin. After all, you cannot know how far off a goal is, if you don’t know what the goal is. But how? Read on...

-

Focus on the weekly retirement income, not just the lump sum: Most people tend to live off a weekly income and not a lump sum. So first, you need to understand how much weekly income you’ll need in retirement in order to find the lump sum figure you need to work toward AKA. your goal.

A general rule of thumb is to aim for at least 70% to 100% of your pre-retirement income. If you’re not sure where to start, it might be a good idea to create a budget.

-

Think about where that weekly income will come from: KiwiSaver is not the only source of income that you have, you might have other savings, rental properties, and of course, you will be relying on NZ Super. Also think harder about future expenses, taking into account possibilities like having to support older or younger dependents in some way, higher healthcare costs, and the possibility of redundancy.

-

Once you have your expenses and known income sources all laid out, let KiwiSaver fill the hole. Now you can convert it to a lump sum and remember the general rule of thumb is - depending on your circumstances, and whether you own your home or not, it’s probably safe to aim for 70 to 100 per cent of your current weekly income, including NZ Super. If you rent, you may need 100 per cent, whereas if you own a home mortgage-free, a 70 or 80 per cent income may be enough.

What if your goal is your first home? Don’t worry the process is exactly the same, just use the steps above to figure out the amount you will need for your first home (We wrote an article on tips for first home buyers using their KiwiSaver which you can read here)!

Now you know how much you need, the next big question is...

Will your KiwiSaver contribution rate get you there?

Many people only contribute 3% of their wage, the minimum rate, hoping that will give them enough for a comfortable retirement. But the reality is, it may not even be enough for one without bells and whistles.

So, here are a couple of graphs to illustrate the impact of different contribution rates over time.

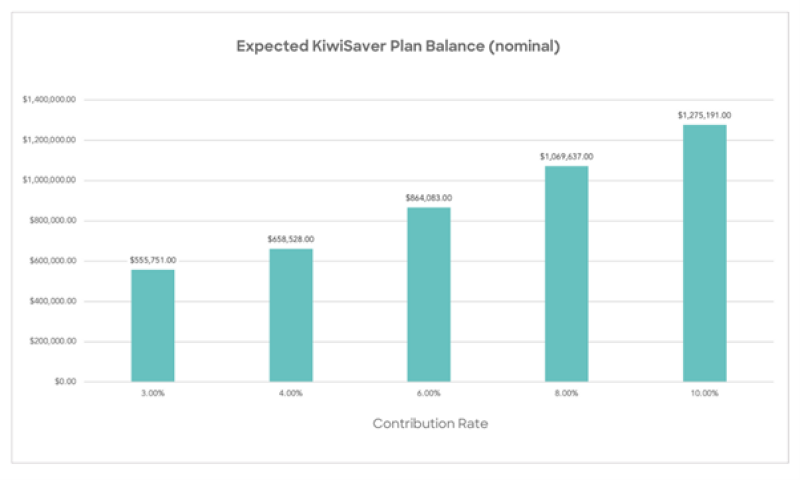

Meet Jared, 30 years old. Assuming he has a starting salary of $80,000 growing at 3.5% per annum between the ages of 30 and 65, here’s how much Jared would have in his KiwiSaver balance at age 65, depending on the contribution rate.

This scenario is based on a $0 KiwiSaver balance with a starting salary of $80,000 growing at 3.5% per annum between the ages of 30 and 65 using a neutral Kōura glide path. We have used the FMA prescribed returns for our growth assumptions:

-

All equity funds are expected to generate a return after tax and fees of 5.5%;

-

Our fixed income fund is expected to generate a return after tax and fees of 2.5%;

-

Our cash fund is expected to generate a return of 1.5%.

We assume 2.0% annual inflation, the mid-point of the Reserve Bank of New Zealand’s inflation targets.

Of course, $555,000 may seem like a lot, but if you turn that amount into weekly payments and compare it with Jared’s current weekly income – not so much.

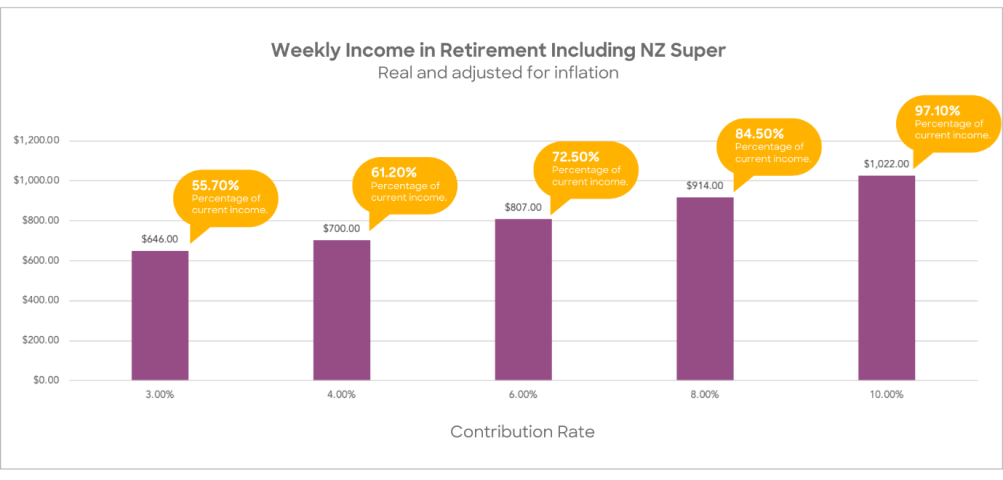

This scenario is based on a $0 KiwiSaver balance with a starting salary of $80,000 growing at 3.5% per annum between the ages of 30 and 65 using a neutral Kōura glide path. We have used the FMA prescribed returns for our growth assumptions:

-

All equity funds are expected to generate a return after tax and fees of 5.5%;

-

Our fixed income fund is expected to generate a return after tax and fees of 2.5%;

-

Our cash fund is expected to generate a return of 1.5%.

We assume 2.0% annual inflation, the mid-point of the Reserve Bank of New Zealand’s inflation targets.

As you can see, contributing 3% would only give him 55.7% of his pre-retirement income. To get to the 70-100% ‘sweet spot’, he would need to increase his contribution rate to 6% and over – more like 8% or 10% if he continued to rent in retirement.

Now, let’s leave Jared to his devices and focus on you. What KiwiSaver rate would you need to achieve your goals? Give our digital advice tool a spin: by selecting different contribution rates, you can see how that would affect your savings.

[hubspot type=cta portal=5033855 id=3d588ebf-2ae0-445a-9da1-83f24583a794]

Another reason to contribute more? Compounding returns

Compounding returns – it’s maths, but it feels like magic! Albert Einstein called compounding returns the 8th wonder of the world. Warren Buffet believes that compounding returns is the greatest contributor to his wealth. Rupert at Kōura calls it his retirement.

Put simply, compounding returns means you can earn investment gains on the gains that you have already made. The more you invest (and the longer your money stays invested), the more your savings grow. That’s why procrastination is an investor’s worst enemy – including for your KiwiSaver plan.

The Kōura difference

Planning for retirement – it’s a balancing act between your short-term needs and future goals. At Kōura, we understand how complicated figuring it all out can be.

This is why, before you invest in our portfolios, we give you an indication of what your KiwiSaver plan might contribute toward your objective. Hopefully, this gives a realistic picture of much you can rely on your KiwiSaver plan for your retirement. Give Kōura a try now and see how your retirement looks.