Should you invest in something based on past performance?

Should you invest in something based on past performance?

15 Nov 2021

How making financial decisions based on past performance could lead to future disappointment

Investing in something that’s historically performed well might seem like a pretty good idea. But in reality, evidence shows that funds that have done well in the past, don't necessarily do so in the future. In fact, more often than not they go on to under-perform. That's why the number one rule in finance is 'past performance isn't indicative of future performance'.

However, that rule doesn't stop investors from repeatedly basing investment decisions on past performance. You might argue investors can't be blamed when they're bombarded with news or social media content that hero's or advertises a fund's favorable performance. But if you shouldn't base investment decisions on past performance, what should you consider? Our article dives into 'past vs future performance', so you can learn what to look out for when sorting your KiwiSaver or investing!

Are great returns just dumb luck or is there some skill involved?

It’s been an interesting couple of years in the financial markets, with plenty of volatility and surprises that provided a great test for fund management skills and adaptability. From the initial chaos from COVID-19 which led to a massive market rebound led by the tech sector, that later widened to other areas as the world got back on its feet.

Looking at the SPIVA mid-year report we can see that from the top quartile funds in June 2019, only a small portion (a mere 4.8%) remained by June 2021.

What this chart shows us is that the best performing funds of June 2019 continued to do well over the next year - whether that was due to benefiting from the Covid post-lockdown rebound or some other factors in 2020. However, things begin to change as 2021 drew closer, the rest of the market began to catch up, leading to those top quartile funds falling back in line with the rest of the pack (back to normal).

“While the persistence report does not prove that fund performance is completely random, from a practical or decision-making perspective, it reinforces the notion that choosing between active funds on the basis of previous outperformance is a misguided strategy.” - U.S. Persistence Scorecard mid-year 2021

So, the main takeaway from this is that as expected the large majority of funds that were performing well just a short time ago are no longer the breadwinners!

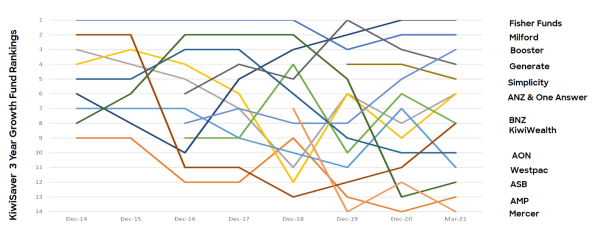

How does this compare to KiwiSaver fund performance?

Well, in short, you can expect largely the same outcome. We have done a little research looking at the historical returns of the KiwiSaver growth funds - ranking them based on their 3-year returns after each year. What we see is mostly consistent with that of the international funds; being that the best performing funds historically don’t tend to perform nearly as well in the future. So now we know that predicting when a fund will outperform is near impossible!

The above chart looks super confusing right? Well, this that's kind of the point. It shows that there are lots of funds that have periods at the top before then having periods at the bottom - providing a good example of how past performance isn’t a great indicator of how things are going to go in future. This predominantly comes down to the fact that fund managers will select a strategy that might work well in one set of market conditions for about 3 years or so - but then, when the market conditions change, their strategy falls apart.

What does all of this mean for passive KiwiSaver providers?

Another thing to think about is whether you should choose an ‘active’ or ‘passive’ fund. While passive funds are unlikely to ever be the short-term superstars - over time they should be consistently top quartile, something that is extremely difficult for active funds to do. Passive investing is meant for the long term, where you follow a set of rules rather than picking individual investments.

In general, a passive investment strategy should perform broadly in line with the markets they invest in less the applicable fees. This means that using past performance to judge the performance of a passive fund is kind of irrelevant.

So, what should you do when it comes to making an investment decision?

The key thing to recognize is that past performance is not something that should be used on its own when making a decision. This can especially be applied to your KiwiSaver.

So, if you shouldn’t pick a KiwiSaver scheme based on it's past performance alone, what should you do?

Think about your risk appetite and investment horizon

Firstly, you need to think about the type of fund you want to invest in, what will give you the best returns relative to your risk appetite and investment horizon (have a read of our blog that covers these two things if you don't know!). This will be the biggest factor when it comes to your overall returns.

Once you have decided on the above, you’ll need to choose a fund manager - some of the things you should look for when doing this should be:

- The fundamentals of the scheme, who’s involved?

- Are they experienced and do you trust their decision-making ability?

- What are the fees like? Are they reasonable and in line with others in the market?

- What's their asset allocation like (i.e., growth vs income assets), remember some funds are not built the same.

- What are they like ethically - do they align with you personally, (i.e., Environmental, or socially) and are they investing in investments that you actually want to own?

- What's the historical performance of the scheme? - it's still something to keep in mind, just shouldn’t be the deciding factor.