Protecting yourself from the woes of inflation

Protecting yourself from the woes of inflation

5 Jul 2023

Protecting yourself from the woes of inflation

Have you been feeling the ‘pinch’ on your wallet these past couple of years? You’re not the only one, as inflation has been stickier and more persistent than anyone expected…

The good news is that there may be light at the end of the tunnel. In their May OCR announcement, the Reserve Bank of New Zealand confirmed that inflation is finally starting to slow and further interest rate hikes may no longer be necessary.

The not-so-good news, though, is that interest rates (including mortgage rates) are expected to stay at this level for at least another year. Hopefully, this will be enough to bring inflation down to its target range of 2-3%. That’s what the RBNZ expects, but as always, only time will tell.

So, now that you know that there’s still some inflation to come, how can you prepare for it? Here are some steps you can take. But first…

A quick recap on what inflation is

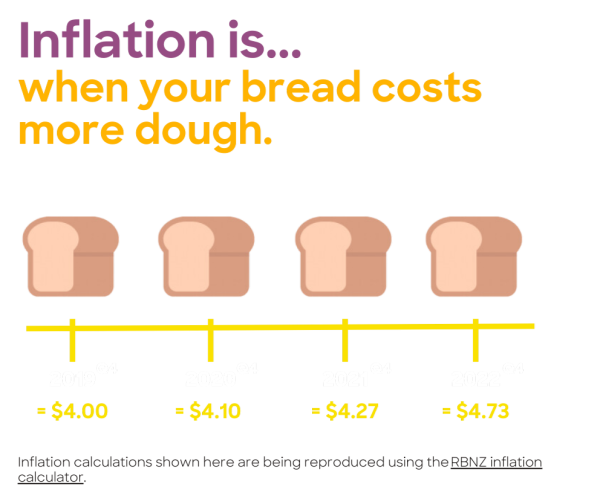

Inflation is the rate at which the cost of everyday living expenses rises each year (it’s called deflation, or negative inflation, when prices fall). We will use the cost of a loaf of bread as an example:

How inflation has changed the price of a loaf of bread over time

Inflation calculations shown here are based on Consumers Price Index (CPI) inflation and Wages official data produced by Statistics New Zealand ("Stats NZ") and are only being reproduced using the RBNZ inflation calculator. Calculations are taken from Q4 of each given year.

A loaf of bread worth $4.00 at the end of 2019 had increased by 73 cents by the end of 2022. You may be thinking it’s only a small increase, but it’s a total percentage change of 18.1% in just three years. And that’s just one of the items in your shopping list.

How much money is left over each month?

One of the best ways to prepare for inflation is to cut costs, and it all starts with understanding where your money is going. Print off your bank statements for the past three years and take a closer look at your day-to-day spending. Now take note of your in-flows (money coming in) and out-flows (money going out), looking up the costs of any monthly contracts you might have on things like your insurance or phone.

Once you’ve figured out your income and expenses, there is an all-important equation you need to run: Sum of income – Sum of expenses = Money left over.

Not the number you were after?

Find money-saving opportunities

Not the number you were after? Don’t be too hard on yourself; it can be an opportunity to save some extra money.

-

Any small costs you can trim off your budget? Go through your budget with a fine-tooth comb and see if there are areas you can reduce spending. Cutting seemingly minor things can save you a lot over a year.

-

Not all debt is created equal – It might also be a good idea to look at any debt you have and what needs to be paid first, starting with the highest interest rates. Prioritising paying off credit cards with higher interest rates first is beneficial in saving you some money. On the other hand, a student loan is interest-free (as long as you’re working in New Zealand) and can usually afford a more relaxed approach. Put them all on a list and pay the ones with the most priority first.

-

Utilise the money management apps out there. They can help you stay on top of your expenses and sort out what money is going where.

-

Remember to take advantage of the free money! If you are on a tight budget, there may also be some Government entitlements worth checking into such as childcare benefits and tax credits that could help bring you some relief.

Time for a proper plan (yes, a budget!)

Now that you have a clearer view of where your money is going, you can develop your own budget.

Setting yourself a budget can be somewhat daunting and feel a little restrictive, so it’s important to remember to keep your budget realistic and make sure there’s still room for some of the things you enjoy. In creating some guidelines around your spending, you have a map to follow. Don’t fret too much if you overspend a little on one day, the bottom line is it’s the weekly and monthly amounts that are key to staying on track. Keep yourself accountable and stay positive so that you feel encouraged!

What inflation means for your KiwiSaver

High inflation can eat away at the future spending power of your KiwiSaver account. To maximise your long-term returns, firstly look at your attitude to risk and - most importantly - your investment timeline (how long you wish to remain invested before needing your savings). Based on your answers to these questions, choose the highest risk fund you can afford to maximise your long term returns.

Remember, you need to be in the right type of KiwiSaver fund for you. By maximising your long-term returns, you’re more likely to outpace inflation in the long run. And, it also can’t hurt to take into account how much you’re paying in fees and doing regular check ups!

The bottom line

An easy way to look at inflation is simply as another cost that can eat away at your savings, but by reviewing your budgeting and investment strategy regularly, you are giving yourself the best possible chance to stay ahead of the curve and achieve the retirement you deserve - if you start to go off course, you can make small changes to ensure you stay on target.

Hopefully, this gives you a better idea of ways you could potentially better protect yourself from inflation, and when it comes to your KiwiSaver if you’re still feeling unsure you can try using kōura’s digital advice tool to help you see how things could look. Advice for KiwiSaver is available for everyone (check out our article on the value of advice), if you want help with your KiwiSaver come and talk to us at Kōura or reach out to your scheme or adviser.