Understanding the types of KiwiSaver funds

Understanding the types of KiwiSaver funds

4 Feb 2020

Choosing the type of fund your KiwiSaver money is invested in will be a critical decision you take for your retirement.

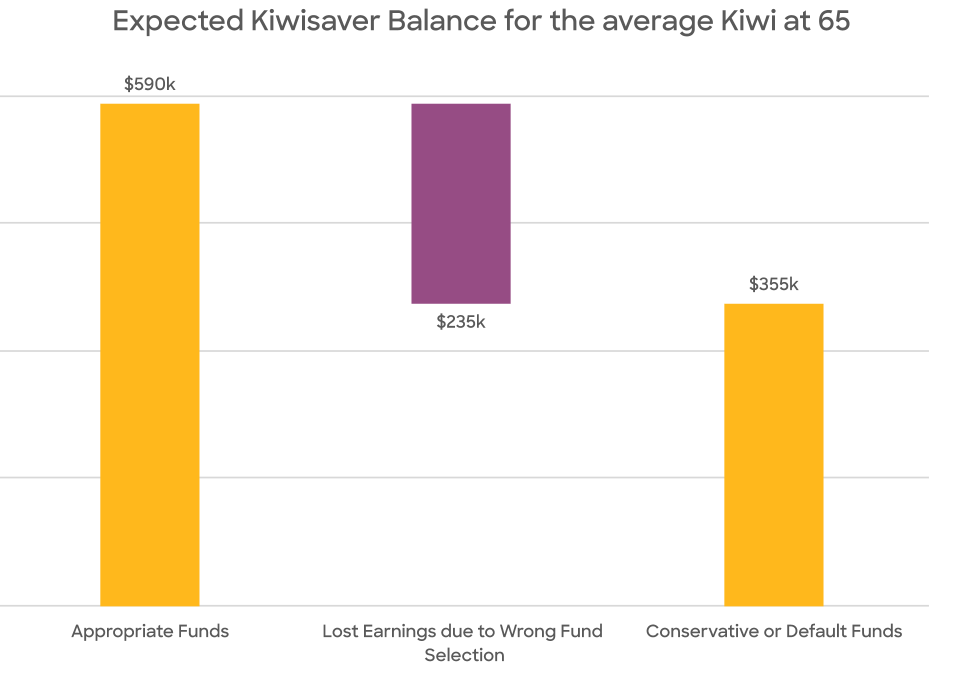

You could contribute 6% of your salary and be in a default fund or you could contribute 3% and be in the right fund. Both decisions will get you about the same KiwiSaver balance at retirement. Which one would you choose?

Unfortunately, the reality is that 53% of Kiwi’s have invested their KiwiSaver savings in the wrong type of KiwiSaver fund for their age and the goals they have for their investment. Even worse, there’s another 400,000 Kiwi’s languishing in default funds where they are earning less than they would with a term deposit.

That means 53% of kiwis are potentially missing out on a free trip to Europe for every year of their retirement.

Types of Assets

Before we get talking about the different KiwiSaver funds we need to understand what makes up a KiwiSaver fund. Broadly, there are two types of assets in a KiwiSaver fund:

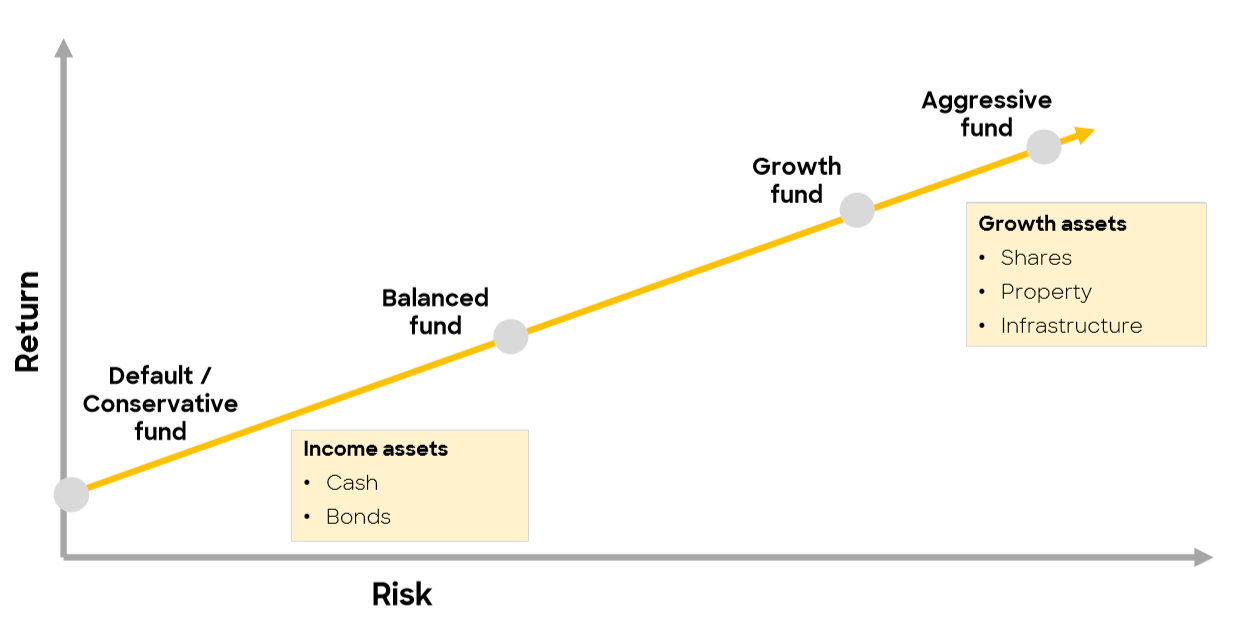

Growth Assets target capital growth and include shares, property and infrastructure. Growth assets are generally more volatile, they have lots of ups and downs over time, though as a general rule, they will grow more than income assets over time.

Income Assets target ongoing income distribution and include fixed income, cash and term deposits. These assets typically have fewer ups and downs, though typically will have lower returns.

Long term impact:

Over the past 90 years, a portfolio of US growth assets would have delivered you a return of 9.7% per annum, whereas a portfolio of US income assets would have delivered you a return of 6.0%. At first look, this means that you want to have a portfolio entirely of growth assets because that will make you the most money. It is true that growth assets will deliver you greater returns over time, but they have much more ups and downs over time (in finance speak “Risk”).

The US equity markets suffered a loss in 25 of these 91 years. One such loss saw markets falling by 43% during the Depression in 1931. In contrast, the best year had a 53% gain in 1954. The US bond market, on the other hand, has only had 16 years in that period where it has delivered a negative return with the greatest loss being 9% (again in 1931 in the Depression).

Types of Funds

Broadly speaking, most providers will offer to invest your KiwiSaver savings in a defensive, conservative, balanced, growth or aggressive fund. Each one invests in different things that have varying levels of risk.

Typically, an aggressive fund will invest 90 – 100% of its funds in growth assets and therefore has the highest risk. It will however likely deliver the highest returns in the long terms. A defensive fund is on the other side of the spectrum with 90% of its funds invested in cash or bonds and has the lowest risk but will also likely deliver very low returns in the long term.

However, it’s important to note here that risk doesn’t truly mean risk in KiwiSaver speak. Think of it like a rollercoaster – the more risk your fund is exposed to, the sharper the peaks and dips. Growth and Aggressive funds are more volatile which mean there are going to be more ups and downs while Conservative funds won’t go up and down as much, but they also have less potential for growth.

How much risk you take depends on your own personal risk tolerance - how you are likely to behave in a downturn - and your investment horizon (how long you will remain invested for). We can tackle these two things in two separate arguments:

1. Risk tolerance

How you might behave in a market downturn is really important to understand. Typically, markets will take anywhere from 5-7 years to recover from a significant downturn. If you change your investment strategy during, or immediately after a down-turn you will be locking in the losses. Whereas if you keep your money invested, you will be riding the gains of an investment strategy. You need to be confident that you will be able to stay the course through a downturn.

| Market Downturns | Peak to trough change | Time to recovery |

| Oil Crisis Recession | 26% Downturn | 3 years |

| Dot Com Bubble | 41% Downturn | 7 years |

| Global Financial Crisis | 51% Downturn | 3 years |

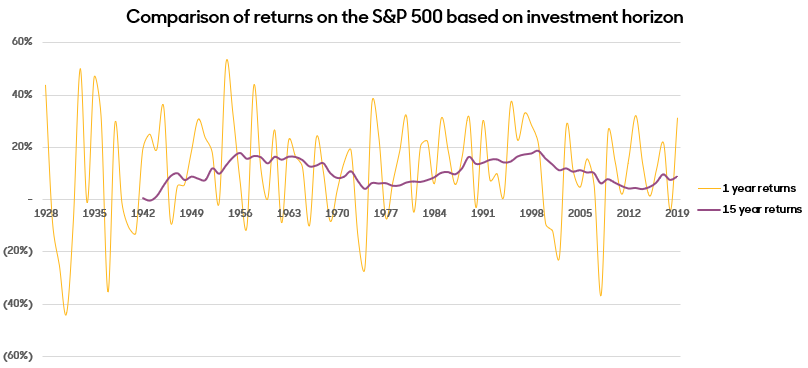

2. Investment Horizon

Investment horizon refers to how long you will remain invested. As you can see in the chart below. On a 1 year basis (the yellow line) there are lots of ups and downs so you need to make sure you can remain invested through both the ups and downs. Looking at returns over a 15-year basis, you can see that the returns are much smoother, and are generally always positive.

Source: Aswath Damodaran - Historical Equity Risk Premium

If you are a long-term investor, these market cycles should not bother you because the market will invariably recover by the time you need to access your money. In finance speak, anyone that is investing for 10+ years and has already purchased their home is essentially a long-term investor. However, one of the biggest mistake KiwiSaver’s make is to set and forget.

The fund type you choose when you sign up to KiwiSaver won’t be the one that’s appropriate for you at 30 or at 55. Your fund should change as you grow older and wiser.

| Type of fund | Horizon | Growth Assets | Forecasted Returns | Investment Personality |

| Defensive | 1 - 3 years | 0 - 9.9% | 1.5% | Don't want your account to ever go down and accept that your balance won't grow ( in some cases not keep up with inflation) |

| Conservative | 2 - 6 years | 10 - 34.9% | 2.5% | Are willing to take on some ups and downs and are seeking average returns |

| Balanced | 5 - 12 years | 35 - 62.9% | 3.5% | Are comfortable with seeing your account value fall a little and are seeking mid-range returns |

| Growth | At least 10 years | 63 - 89.9% | 4.5% | Looking for high growth in the long term and won't want to switch when your balance falls a lot |

| Aggressive | 10 years or more | 90 - 100% | 5.5% | Looking for strong long-term growth, knowing you will stick with your choice of the fund even when your balance fluctuates fast |

Let’s put this into context

To really understand the impact of being in the wrong fund you need to put it into context and for that, you need to meet two people, Jake and Rachel.

Jake is a 26-year old customer service manager at one of NZ’s leading banks. His partner and he have started doing the homework on the Auckland property market and expect to purchase his first home in the next 3 years. Jake has been investing in KiwiSaver since he was working part-time at Uni and his investment in a growth fund has meant that he has almost $25,000 saved up in there for his first home deposit.

A popular misconception is that a growth fund is the best place for Jake’s KiwiSaver money so he can accumulate as much money as possible before he withdraws it all for this home. However, doing this is risky because if markets fall, Jake could lose a significant portion of his deposit and he may either not be able to put enough towards the house or may even have to postpone his first home purchase altogether.

Going back to the table above, the ideal place for Jake to invest would be a Conservative fund. As he gets closer towards purchasing, he should then move to a Defensive fund so that his capital is protected.

Now let’s meet Rachel. Rachel is a 37-year old Marketing Manager in Auckland earning about $80,000 a year. She has used up her entire KiwiSaver balance towards purchasing a home and is now starting the long journey of building up her KiwiSaver balance once again. Rachel describes herself as being quite a safe and considered person and is, therefore, looking to invest in a Balanced fund.

While a balanced fund is certainly an okay place for Rachel to invest if she is risk-averse, it is important that Rachel understands that she will be invested in KiwiSaver fund for at least another 25 years, ideally for another 40 (because even if you can withdraw your money at 65, you should continue to stay invested to access the best returns). This means that Rachel has enough time to see through multiple market cycles and their recovery. Staying in a balanced fund or conservative fund could mean that she loses out on thousands of dollars of returns at retirement.

The Kōura difference

We understand that choosing the right type of KiwiSaver fund can be hard. It’s important you spend a bit of time comparing what’s out there because not all funds are made equal. Within the same type of fund, different providers will offer varying fees, services and returns, regardless of what your existing provider might insist. Think of it as a smartphone. All of them will let you call, text and take photos but an iPhone will offer a radically different experience to a Galaxy Note to a Huawei.

Kōura is unique in the market, we have a digital advice tool that will create a personalised portfolio to match your personal objectives and profile. Whether you’re looking to buy a house or save for retirement, our tool will give you honest and impartial advice to help you make the most out of your KiwiSaver fund.

We also believe that there are few things in life that fit neatly into 3 – 5 different boxes labelled ‘Conservative’, Balanced or Growth and your KiwiSaver fund is not one of them. This is why we offer our investors a range of six different funds and we will tailor your portfolio by combining our four equity funds and two fixed-income funds.

Importantly, we believe your KiwiSaver portfolio should change as you change and we check in with you every year to ensure you are still invested in absolutely the right KiwiSaver plan for you.

.png)