Banks in crisis, but markets up? What is going on?

Serious market wobbles brought on by a mini-banking crisis have not deterred global share markets this month. But can the good news continue, or will things get worse before they get better?

Despite the doom and gloom brought on by the threat of a new banking crisis, global stock markets ended the month with a 2% gain and a quarterly gain of 9%. Markets are now up 14% since their October lows though remain 11% left below their January 2022 highs.

All of this occurred in a high stakes month which saw the collapse of several mid-tier US banks, an implosion from Swiss banking giant Credit Suisse and wholesale interest rate announcements from most central banks.

With so much to cover in a high octane month, let’s get straight into the biggest moments of March, in this month’s Market Wrap.

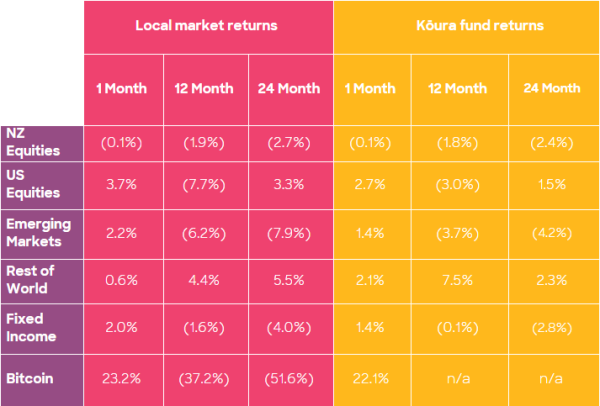

The kōura funds are impacted by currency (translation of local currency indices to NZD) and also differences in constituents between the underlying indices and the actual investments that the kōura funds invest in. kōura returns are net of tax. The kōura Carbon Neutral Crypto Currency Fund inception date was 23 May 2022. Returns over 12 months are annualised. Past performance is not necessarily an indicator of future performance and return periods may differ.

1. The banking crisis – What happened, and what does it mean?

Early in the month we saw the rapid collapse of several mid-tier US banks (Signature Bank, Silicon Valley Bank and Silvergate Bank). By the end of things the Silicon Valley Bank collapse ended up being the second largest US bank failure of all time.

The failures were largely caused by poor investment management. The banks invested in long-dated Government bonds (purchased in a low interest rate environment) funded using short dated deposits.

In plain English this meant the banks used money that customers could ask to be returned tomorrow to purchase bonds that needed to be held for 10, sometimes 20 years.

This strategy works fine in a falling interest rate environment where the value of the bonds increases, but over the past 18 months rapidly rising interest rates resulted in the value of the bonds falling.

At the same time depositors started to pull their money out to invest in other higher interest earning accounts, which reduced the volume of deposits in the bank. This forced the banks to sell the assets and realise those losses. This was what eventually made them insolvent.

But Credit Suisse was a different story. This was the second largest bank in Switzerland and a globally important bank. Over the past 5 years it has been involved in a number of high profile and expensive scandals such as the Archepego disaster in 2021.

Credit Suisse was on the path to restructure of its business, though were widely expected to need more capital to support that turnaround. Unfortunately their largest shareholder Saudi National Bank though stated in an interview that they would not invest further into Credit Suisse and this pushed the bank into free fall as investors fretted that Credit Suisse would not have enough capital to execute on the ambitious turnaround plans.

Over the course of a weekend, they were very quickly sold at a massive discount to their Swiss peer UBS. Regulators around the world were unwilling to let another global systemic bank fail after witnessing the chaos that ensued after the collapse of Lehmans back in 2008.

The big surprise for all involved has been the massive speed that a bank run can happen. In the past a bank run would happen over a course of weeks, but now can happen over the course of hours largely due to the power of social media and internet banking. Luckily for the remaining US regional banks, regulators were quickly step up to the plate, effectively guaranteeing deposits and providing liquidity backstops in place for any other banks that were suffering from liquidity issues.

Whilst the immediate fallout from this banking crisis seems to be over, banks remain nervous and will be doing everything they can to protect their funding and liquidity positions. The easiest way to do this is to stop lending which will stifle growth.

Investors are now cautiously watching to see what may happen next.

2. Have central banks changed their tone?

Both the European Central Bank (the ECB) and Federal Reserve (the Fed) announced their interest rates decisions over the course of this past month. The ECB raised rates by 0.5% taking rates up to 3.0% and the Fed raised rates by the widely expected margin of 0.25% taking them to 4.75 – 5.0% (in line with New Zealand’s Reserve Bank).

The interesting thing about both announcements was the change in tone. Both central bankers made it clear that while inflation is higher than they would like they will be watching the data very closely to see what further action is necessary, implying that we might be at the end of the tightening cycle.

Both banks have stated credit conditions are likely to tighten as a result of the banking issues and this might do some of the work of higher interest rates.

This is a very different message from previous months where Central Bankers consistently talked about “how much work” there is to do and how much higher interest rates are likely to go.

At the time of writing (4 April) the market is expecting one more rate rise for both the US Fed and the ECB of 0.25% at their next meeting a pull back from previous expectations.

3. Why have wholesale interest rates fallen over the past month?

Wholesale interest rates have materially fallen over the past month following the change in tone from global central bankers and in response to the banking issues.

In New Zealand, two year rates fell from a high of 5.5% all the way down to 4.9% during the month. In the US, interest rates fell even faster with a drop from 5.4% down to 4.4% at the end of the month.

These changes are a result of the revised view on where we are in the inflation fight, markets are now anticipated a lower peak and a cut in interest rates to happen sooner than expected. If interest rates remain where they are this will be seen as a material easing of financial conditions which will force central banks to be more aggressive than where they currently are.

Over the past 18 months, the market has continually underestimated how hard it will be to get inflation under control and how quickly interest rates will reverse again. Central banks are saying that they expect interest rates to stay higher for longer, while the market is saying interest rates will start to fall again in Q4 2023 or Q1 2024, it will be interesting to see who is right here.

4. Why does Bitcoin continue to rise?

Bitcoin continues to rise and is now up over 75% from its October lows. After a tough start to the year, Bitcoin has emerged as one of the year’s best performing asset classes, and as of 31 March, was trading US$28,000.

Part of the reason for this has been the banking collapse, which has made people consider whether banks are as safe as they seem.

At the same time as global banks such as Silicon Valley Bank, and Credit Suisse have faced major crisis we have seen massive inflows into crypto currencies as people look for a safe haven.

While the banks and depositors have been saved this time, people may question whether they will be saved next time again.

March 10, the day that Silicon Valley Bank filed for bankruptcy was the largest ever day of contract volumes on the Ethereum network. In my view this proves the trend that customers were moving funds into stable coins.

There is no question that question marks still hang over crypto currencies, and their use and longevity is yet to be proven, but this month we saw some good signs of crypto holding its own amid choppy waters.

Thank you to NBR for giving us the opportunity to share a different side to the crypto story this month. Has cryptocurrency finally come of age? (nbr.co.nz)

5. Where to from here?

It is difficult to make predictions in what remains a very uncertain market, but here is what we expect to see unfold over the next few months.

Markets will remain choppy and there are likely to be scary times ahead. While markets may slip from where they currently stand we expect to see them recover before year’s end back to where they ended the month. The market will continue to debate whether we are moving to a hard or a soft landing, and the prevailing narrative at the time will drive the markets up or down.

In our view interest rates will continue to rise and are likely to stay higher for longer than the markets are predicting. Unfortunately we are not out of the inflation woods yet - the labour market remains way too tight and recent oil price rises will increase inflationary pressure. There is definitely more to come in this space.

But one thing we do know, is when we hit the bottom things will turn very quickly. All of a sudden we will see markets on the up, inflation falling sharply, and rate rises will slow. And this will happen far faster than people predict, it is only with hind sight that we will know we have been through the bottom of the markets.

All we can do is grit our teeth and hold on until then.

Disclaimer: The views and opinions expressed are those of the author Rupert Carlyon, the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.