Your nest or your nest egg: what comes first?

Table of Contents

Your nest or your nest egg: what comes first?

21 Jun 2023

Your nest or your nest egg: what comes first?

Deciding between paying the mortgage or building your retirement nest egg is tough. So, what do you prioritise and how?

A large proportion of New Zealanders are dependent on their property values to fund their retirement. However, according to the latest data from the Commission for Financial Capability(1), one in five Kiwis aged over 65 are still paying their mortgage, and 80% are spending the equivalent of more than 40% of NZ Super on housing costs. What’s more, as the report reads, "Future generations of retirees will look very different from our current retirees. They are much less likely to own their home, and if they do, they are less likely to have paid off their mortgage by the age of 65.”

While paying your mortgage faster can be difficult at this stage, due to the rising cost of living and higher interest rates, entering retirement mortgage-free is still crucial. Not only you will not have to fund mortgage repayments with your retirement savings, but you will also save thousands of dollars in interest costs: all money that could be diverted to your KiwiSaver account or other investments.

Why it’s important to have a plan

Here in New Zealand, we’re lucky to have universal pension. But unfortunately, NZ Super was not designed to cover rent or mortgage payments. And according to the latest research from Massey Fin-Ed Centre(2) NZ Super rates are not enough to cover most households’ retirement expenses.

In 2022, depending on where they lived and the quality of their lifestyle, a New Zealand two-person households could spend between $800 and $1580 per week, but only receive $712.22 from NZ Super every week. And although NZ Super rates were increased on 1 April 2023, these adjustments struggle to keep up with an annual inflation rate of over 7%.

That’s why it’s important to have a plan and prioritise debt repayment while you save for the future. Of course, in between paying down the mortgage and saving for retirement are a bunch of other expenses that may come up or life goals you may wish to achieve, like long-term travel as a family or saving up for your kids’ education. So, how can you juggle everything without dropping the ball?

Our suggested priorities

1. Maximise your KiwiSaver benefits.

You may already know that if you contribute to your KiwiSaver balance, your employer is liable to match your contributions up to 3%. On top of this, every year, the Government also matches 50 cents to every dollar you contribute in the 12 months to 30 June, up to a maximum of $521.43 per year. This is the annual Government contribution – click here to find out more. While $521.43 may not seem much, it’s like getting a 50% return on the first $1,042.86 you put in your KiwiSaver, every year. Plus, thanks to the power of compounding returns, that extra money you get from the Government and your employer can grow significantly over time.

Here are some practical examples to illustrate this:

Scenario #1: Making the most of KiwiSaver -

Assuming you are 30 years old, with an average salary of $70,000, an annual 3% of KiwiSaver contribution before tax equals approximately $2,100* invested in your KiwiSaver account in a year. However, when you account your employer contributions at 3% (another $1,470**) and the maximum annual Government contribution ($521.43), you are actually saving up $4,091.34 in a year into your nest egg – which is almost double the amount! If your current KiwiSaver balance is $25,000, invested in a Kōura personalised portfolio (e.g., 90% Core Growth Fund and 10% Income Funds), your projected KiwiSaver value at age 65 will be $666,993

Scenario #2: Putting $2,100 per year in a savings account -

Now, let’s say you didn’t invest that $2,100 (3% of your annual pre-tax salary) in KiwiSaver, but instead put it in a savings account giving you an average 3% return p.a. $2,100 per year equals to approximately $40 saved per week. By the time you turn 65, your savings will amount to about $127,000.

Scenario #3: Increasing your mortgage repayments by $2,100 per year -

In this scenario, you don’t contribute an annual $2,100 to your KiwiSaver account or savings account, but rather increase your annual mortgage repayments by $2,100 Assuming a $500,000 mortgage and lifetime mortgage interest rate of 7% over 30 years, your minimum mortgage repayments are $3,327 per month, or $39,924 per year. This means you will pay $697,544 in overall interest costs. If you increased the annual repayments by $2,100, or $175 per month, you will shorten the life of your mortgage by four years and pay $577,087 in overall interest costs. It’s a saving of $120,000 in interest costs, plus you will have four years of mortgage-free living to focus your efforts on saving for retirement.

As these scenarios highlight, increasing your mortgage repayments make sense, and it’s definitely something important to consider. But at least for that first 3%, nothing is as effective as maximising your employer and Government contributions.

2. Get rid of all consumer debt.

Consumer debt is any debt aside from a mortgage and student loan that you’ve taken on to fund travel or new purchases or unexpected expenses, either through an overdraft, your credit card or the various hire purchase providers that are available.

Unlike your domestic student loan, which is cheap, the average credit card charges 20% on any credit you roll over past your bill cycle. And, while hire purchase on companies like AfterPay, Q Card etc. may seem like great deals, they often make their money through various hidden fees and by continuously enticing you to buy things you don’t really ‘need’.

Overall, the interest on consumer debt is higher than what you pay on your mortgage or what you’re likely to get in investment returns from KiwiSaver or elsewhere. Which is why it makes sense to either pay this off completely and ensure you’re able to pay off your credit card bills in full before you turn your focus back to the nest v/s nest egg question.

3. Get on comfortable terms with your mortgage.

Gone are the days of 2.5% mortgage rates, and it’s not clear when they will return (if ever). But higher interest rates aren’t just bad news for your monthly repayments. If you calculate the interest, you’ll likely find that the total interest you’ll pay over the lifetime of your mortgages is higher than the original price of your home. In other words, unless you pay your mortgage faster, your house will cost you more than double the original price.

The solution is making extra repayments, which go directly to reduce the principal portion of your mortgage (the total amount you still owe). This, in turn, helps reduce the term of your loan, so you can get more comfortable with it.

Of course, in times of rising cost of living and high mortgage rates, it’s possible that your budget can only cover the already high minimum mortgage repayments. If so, don’t forget to take advantage of any pay rises and future interest rate drops. Keeping mortgage payments at the same level when interest rates drop can be an easy way to pay extra without feeling the pinch, because you’ve already made room for those payments in your budget.

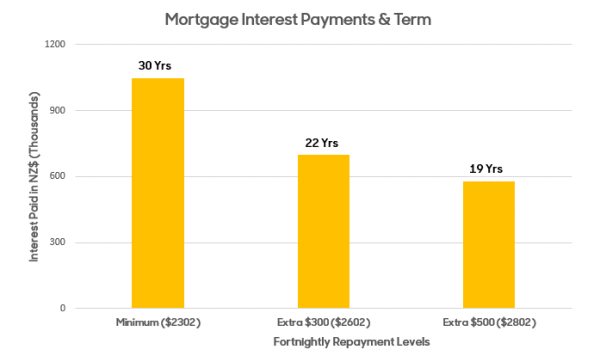

To illustrate how this works, meet Jane, a 35-year-old who just took out a $750,000 mortgage.

As the graph shows, if Jane paid the minimum amount over a 30-year period, based on a lifetime mortgage interest rate of 7%, her minimum fortnightly repayment amount would be $2,302, and she would pay $1,045,491 in interest by retirement age. This is about 139% of her original mortgage amount, just in interest costs.

But if Jane made an extra repayment of $300 every fortnight, she would bring her mortgage term down to 22 years – giving herself eight full years to save up for retirement, likely when she’s earning her highest salary. Instead of $1,045,491, she would pay $698,003 in interest payments – a figure that hopefully will be offset by the equity she will build in the property.

Keep in mind that the best time to make extra repayments is in the first 10 years, when most of your ‘minimum payment’ is actually going toward interest. Whatever extra you put in during these years directly reduces your principal, and paying down your principal early means your savings get compounded over time.

4. And now you save, save, save.

The majority of Kiwis are currently only contributing 3% to their KiwiSaver account. However, as we explained here, this is unlikely to give you a comfortable retirement.

In fact, research shows that a 3% contribution rate will only yield a retirement income of around 53% of your current take-home salary, whereas international standards suggest that you should aim to replace at least 70-100% of your existing income to maintain a similar lifestyle.

To bridge this gap, consider increasing your KiwiSaver contributions or making extra voluntary contributions. And remember: every little bit counts. Building up your nest egg beyond the minimum may not be possible immediately, but even small, incremental increases can have a significant impact down the line, due to the power of compounding returns.

The bottom line

At the end of the day, any money you’re putting toward debt or investing is a step in the right direction. Your priorities may change as your life changes, so let the math tell you which one to focus on first. It’s also important to keep nurturing your KiwiSaver balance and ensuring you’re in the right type of fund as that has the biggest impact on your final retirement pot.

At Kōura, we believe that everyone should be able to access free advice for their KiwiSaver investment, so they can make well-informed decisions about their future. Like to get started? Use our digital advice tool to develop a personalised portfolio that is right for you.

Assumptions

* Calculations for the employee’s KiwiSaver saving made using PAYE calculator (PAYE.net.nz/calculator). Calculations for the annual Government contribution are done on the assumption of employees holding a full-time role where they are not on a total remuneration package. These amounts will vary for self-employed people, temps and contractors.

** In this example, a 3% employer contribution equals $1,470 ($2,100 adjusted for ESCT at 30%).

Sources

1. Te Ara Ahunga Ora Retirement Commission – Review of Retirement Income Policies 2022.

2. Massey University NZ Fin-Ed Centre – New Zealand Retirement Expenditure Guidelines 2022

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.